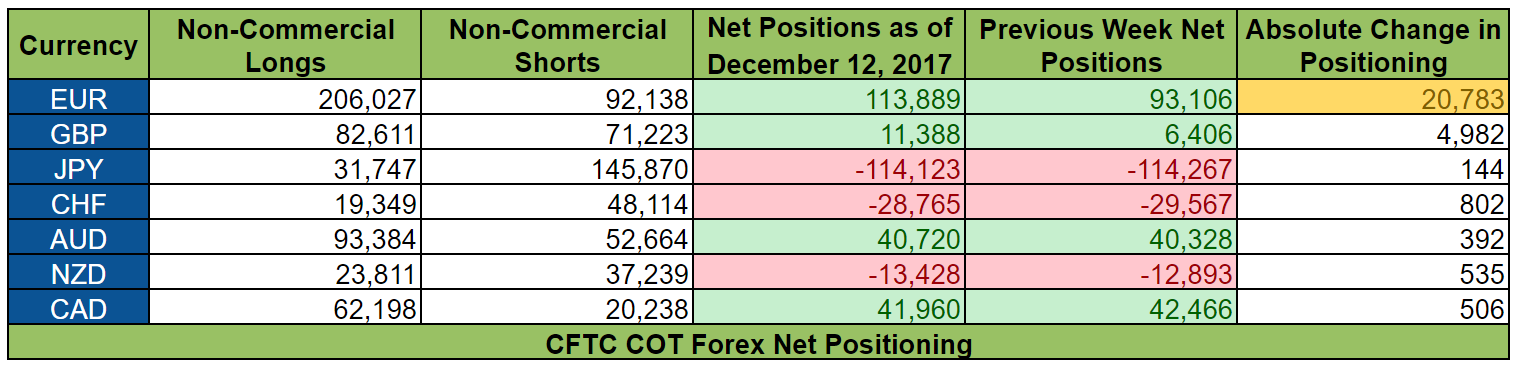

Large players apparently ramped up their net bearish bias on the Greenback since the value of net short positions on the Greenback jumped from $4.28 billion to $7.81 billion during the week ending on December 12, according to calculations done by Reuters.

However, the latest Commitments of Traders (COT) forex positioning report from the CFTC reveals that unfavorable positioning on the Greenback was driven mostly by a squeeze on euro shorts and, to a lesser extent, unwinding by pound bears.

Oh, please keep in mind that the numbers below show the net positioning of non-commercial forex traders against the U.S. dollar.

And if you’re feeling overwhelmed by all these figures, you might need to review our School of Pipsology lesson on How to Gauge Market Sentiment Using the COT Report in order to learn how to pinpoint potential forex market reversals.

And here is how positioning activity played out during the week ending on December 12, 2017.

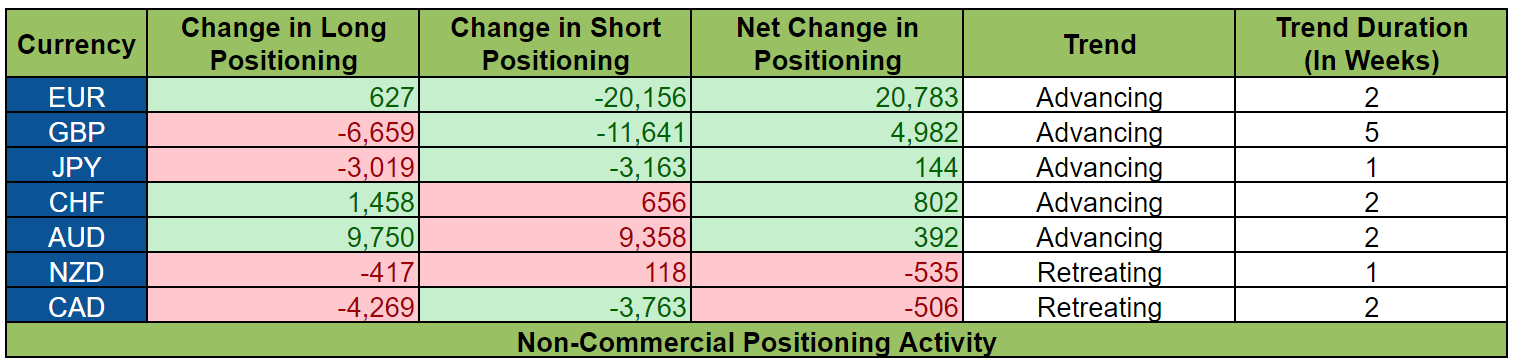

Positioning activity was a bit mixed and net change in positioning on most currencies was only very minimal. Moreover, sentiment on the Greenback deteriorated mainly because of favorable positioning activity on the euro and, to a lesser extent, the pound.

We can therefore conclude that positioning activity was likely driven by sentiment on the other currencies, rather than by sentiment on the Greenback itself.

With that said, the Greenback did lose some ground to its peers, with the exception of the Kiwi and the Loonie. The Greenback therefore showed a degree of vulnerability. And this was probably due to uncertainty with regard to the Fed’s forward guidance and the Alabama Senatorial elections.

We now know, however, that the Fed hiked as expected while keeping its forecasts for the future path for the Fed Funds Rate essentially unchanged.

Also, we now know that Democrat Doug Jones won in Alabama, which dented the Greenback’s price action since it stoked fears that the Republicans would have a harder time in pushing for their agenda. Jones vote won’t have an impact on the tax reform bill, however, assuming Congress can vote on the bill before Jones takes office this January.

Okay, here are the major events, reports, and other catalysts for the other currencies:

EUR

The euro took even more ground from the Greenback, so much so that net bullish positioning on the euro was the highest since early 2007.

However, a closer look at positioning activity shows that favorable positioning on the euro was actually driven almost entirely by the squeeze on euro shorts, rather than by a build-up in euro longs.

Interestingly enough, the only positive catalyst during the week ending on December 12 was the news that SPD members voted to allow coalition talks with Angela Merkel.

It’s possible, however, that positioning activity reflects unwinding by euro bears ahead of the ECB statement since recent economic data showed that the Euro Zone economy is still evolving within the ECB’s expectations or better, which likely raised expectations that the ECB may sound a bit more optimistic, perhaps even hawkish.

Of course, we now know that the ECB upgraded its growth and headline inflation forecasts but maintained its forward guidance, including its easing bias on its QE program.

GBP

Positioning activity on the pound was mixed. Even so, more pound bears abandoned ship compared to pound bulls, which is why net positioning on the pound became even more bullish, which marks the fifth consecutive week of favorable net positioning on the pound.

Positioning activity likely shows unwinding ahead of the BOE statement, as well as profit-taking by pound bulls and pound bears getting spooked because of news that there was a breakthrough in Brexit talks.

We now know that the BOE tried to sound cautious and just shrugged off the U.K.’s net positive economic data. Also, we now know that Brexit talks were cleared for Phase 2 during the Euro Summit. However, the most recent COT report does not reflect those developments.

JPY

Net positioning on the yen was practically unchanged since the reduction in yen longs and yen shorts almost cancelled each other out.

There’s really no clear reason for the trimming in both yen shorts and yen longs, but it’s possible that the paring of yen longs was due to the prevalence of risk appetite at the time. The reduction in yen shorts, meanwhile, may have been due to jitters related to the botched December 11 terrorist attack in New York City, as well as the Senatorial elections in Alabama.

CHF

Net change in positioning on the Swissy was only minimal since the 1,458 increase in long Swissy contracts was partially offset by the 656 increase in short Swissy contracts.

The build-up in Swissy longs likely outpaced the increase in Swissy shorts because of safe-haven demand for the Swissy, given the Alabama Senatorial elections.

As for the increase in Swissy shorts, that was probably because of the prevalence of risk appetite in other markets at the time.

AUD

Net bullish positioning on the Aussie was only nudged very slightly higher. However, positioning activity reveals that both Aussie bulls and Aussie bears were reinforcing their respective positions.

The increase in Aussie longs was likely due to the the prevalence of risk appetite at the time as well as preemptive positioning ahead of Australia’s jobs report.

As for the build-up in Aussie shorts, that likely reflects falling gold prices at the time.

However, it’s also possible that the increase in Aussie shorts reflects preemptive bearish positioning ahead of Australia’s jobs report. If that is indeed the case, then those bears likely got burned since Australia’s jobs report was better-than-expected.

NZD

Net change in positioning on the Kiwi was very modest. Likewise, positioning activity on the Kiwi was also very modest.

The very minimal positioning activity on the Kiwi is actually kinda strange since it implies that large players weren’t all that affected by Adrian Orr’s appointment as the new RBNZ Governor, even though spot Kiwi and Kiwi futures broadly caught a bid.

CAD

The Loonie took a very small step back against the Greenback since more Loonie longs got culled compared to Loonie shorts.

Positioning activity likely shows profit-taking by Loonie bears and disappointed Loonie bulls calling it quits because of the BOC statement since the BOC presented a cautious and neutral tone while focusing on uncertainties rather than the recent positive economic developments.

Got any other conclusions you can draw from this latest COT Report? Feel free to share your thoughts in the comments section or if you’re looking for further discussion, community member ForExchange has a lively thread called Trading based on Market Sentiment in the forums awaiting your participation.