Large players were apparently not too fond of the Greenback in Q1 2018 since net bearish positioning on the Greenback ramped up from $4.62 billion as of the week ending on January 2 to $21.73 billion in the week ending on March 27, according to calculations done by Reuters.

This is slightly off the $21.99 billion that was reported during the week ending on March 20, which is the highest net bearish positioning level on the Greenback since 2011.

To add to that, the Commitments of Traders (COT) forex positioning report from the CFTC also reveals that large players favored the other currencies at the expense of the Greenback, with the euro, the pound, and the yen being particularly favored. The only notable exception was the Loonie since net positioning favored the Greenback over the Loonie.

Sentiment on the Greenback deteriorated during Q1 2018 for a variety of reasons, which include higher growth prospects in other countries, Europe in particular some market analysts say.

Other than that, fears of a potential trade war between the U.S. and China were also cited by market analysts as the reason for the anemic demand for the Greenback.

Sure, trade war fears really flared up only recently. However, some of you may still remember that there were already reports out as early as January about Trump’s plan to punish China’s trade practices which Trump perceives as unfair.

China, for its part, recently announced tariffs on U.S. goods to counter Trump’s own China tariffs, but there were also reports back in January that China was supposedly thinking about slowing/stopping its purchases of U.S. treasuries, which had a detrimental effect on the Greenback’s price action.

And while it’s a relatively late event, the Fed’s decision in the latest FOMC Statement to maintain its forecasts for the future path of the Fed Funds Rate to only show two more hikes in 2018 also likely helped to sour sentiment on the Greenback.

Okay, here is how positioning activity played out on the different currencies during the past six months, but we’ll only be focusing on the last three months (Q1 2018).

Oh, please keep in mind that the numbers below show the net positioning of non-commercial forex traders against the U.S. dollar.

And if you’re feeling overwhelmed by all these figures, you might need to review our School of Pipsology lesson on How to Gauge Market Sentiment Using the COT Report in order to learn how to pinpoint potential forex market reversals.

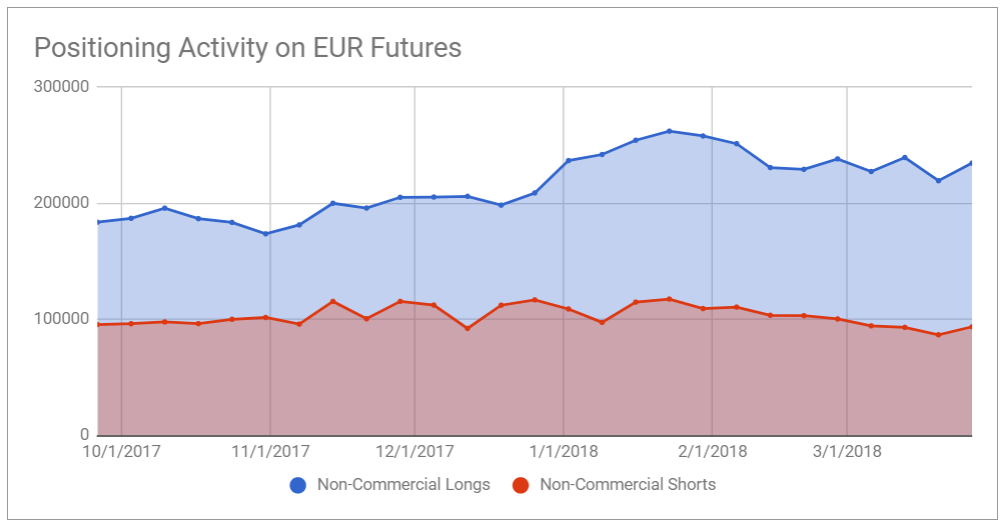

EUR

Euro bulls added to their long positions in January, then began winding them down starting in February. Euro bears, meanwhile, have also been steadily unwinding their positions since February. However, bears were culling their bets at a slightly faster pace than bulls. And as a result, net positioning on the euro remained bullish as of the week ending on March 27, 2018.

The buildup in euro longs in January was likely driven by the December ECB minutes, which were released on January 11, since the minutes revealed that ECB members thought that “The language pertaining to various dimensions of the monetary policy stance and forward guidance could be revisited early in the coming year.” And that was seen as a possible hint at a future tightening of monetary policy.

Another likely driver for the buildup was the progress in German coalition talks and speculation that a coalition government will be formed since there were reports at the time that German Chancellor Merkel and SPD Leader Martin Schulz have struck a deal to move forward to formal coalition negotiations.

As to why both euro bears and euro bulls began to unwind their positions starting in February, profit-taking by bulls and bears getting spooked seems likely since Merkel was able to finally hammer out a coalition deal with the SPD, thereby easing political uncertainty in Germany and the Euro Zone as a whole.

Also, the ECB’s January ECB minutes, which were released on February 22, heavily implied that the ECB was cautiously hawkish. And that likely prompted more bears to unwind their positions while bulls, especially those who were expecting a much more hawkish stance, likely decided to cull some of their positions as well.

And this culminated in the ECB removing its easing bias on its QE program during the March 8 ECB statement, which likely prompted even more bears to run away. However, bulls weren’t enticed to add their longs, likely because the ECB also tried its best to sound cautious, even neutral.

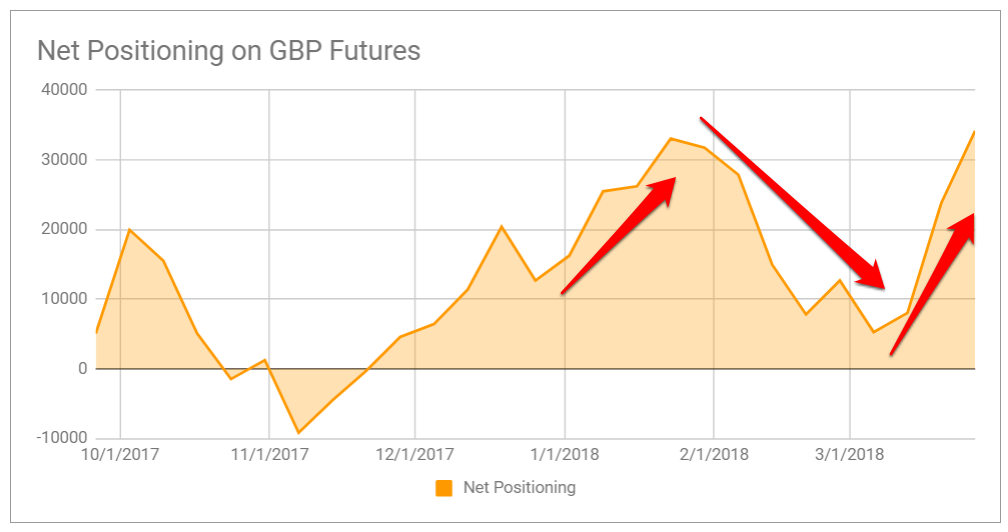

GBP

Large non-commercial forex traders have been net bullish on the pound throughout the entirety of Q1 2018. And while it’s not at a steady pace, pound bears do seem to be trimming their positions over time.

And if we look at net positioning activity, large speculators became more bullish on the pound at the start of the year, dialed back their bullishness in late January, then became more bullish again by March.

The increase in net long positioning in January was actually a continuation of the trend that started in late November. And the increase in net bullish positioning was likely driven by optimism that Brexit talks were cleared for Phase 2.

As to why bullish sentiment on the pound began to deteriorate later, that was likely due to renewed Brexit-related jitters since doubts over a possible transition deal began to grow.

And those doubts were reinforced when the E.U. released its Draft Withdrawal Agreement since some of the provisions were so bad that British PM Theresa May remarked that “no UK prime minister could ever agree” to the E.U.’s proposals.

However, Brexit talks continued to move in a mostly positive direction, resulting in a transition deal being announced on March 19. And so sentimen to pound also improved.

Aside from Brexit-related events, sentiment on the pound also likely improved because the British economy has been evolving mostly within the BOE’s expectations, so much so that two BOE members even voted for a rate hike during the March 22 BOE statement.

JPY

Positioning activity on the yen was steady on January. However, yen bulls began quietly adding to their positions in January while bears began to pare some of theirs. There was then a massive culling of yen shorts during the weeks ending in March 20 and 27.

The steady rise in yen longs and decline in shorts was likely due to the prevalence of risk aversion during the quarter.

As for the sudden slashing of yen shorts late in March, that was likely due to speculation that the yen will be in demand because of the intense risk-off vibes at the time because of fears of the potential trade war between the U.S. and China.

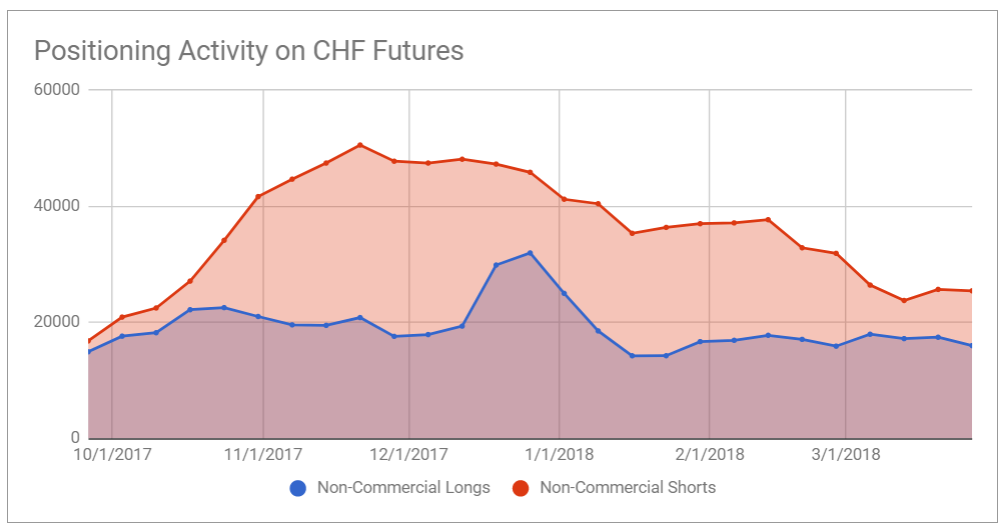

CHF

Net bearish positioning on the Swissy has been easing throughout Q1 2018. However, that was driven largely by the steady unwinding of Swissy shorts since Swissy longs have been steady for most of the quarter, except for the reduction at the start of January.

And the steady decline in Swissy shorts was likely due to the prevalence of risk aversion during the quarter.

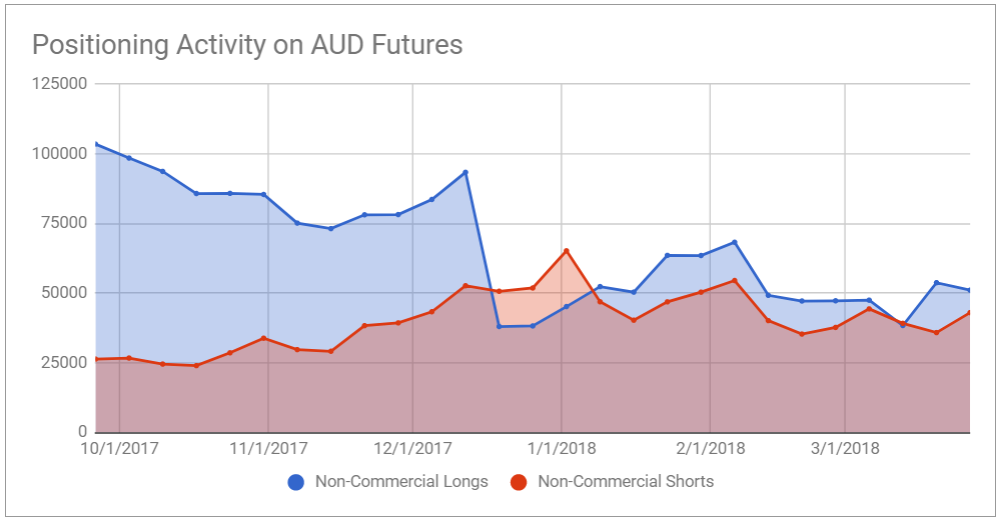

AUD

Large players have been mostly net bullish on the Aussie during Q1 2018. There was a brief period when traders were net bearish on the Aussie after longs fled en masse in the wake of the dovish minutes of the December RBA meeting, but bulls have been mostly on top since then.

Bears, meanwhile, appear to have been trimming their positions since there were only 42,998 short contracts on the Aussie as of the week ending on March 27, down from the recent peak of 65,201 contracts during the week ending on January 2.

As to why bulls aren’t giving up while bears seem to be rethinking their position, that’s probably because the RBA continues to have a hawkish tilt, although the RBA also keeps stressing that a rate hike isn’t coming anytime soon.

RBA Governor Lowe said in a February 8 speech, for example, that “given recent developments in Australia and overseas, it is likely that the next move in interest rates in Australia will be up, not down.” However, Lowe also repeated the RBA’s message that “the Reserve Bank Board does not see a strong case for a near-term adjustment in monetary policy.”

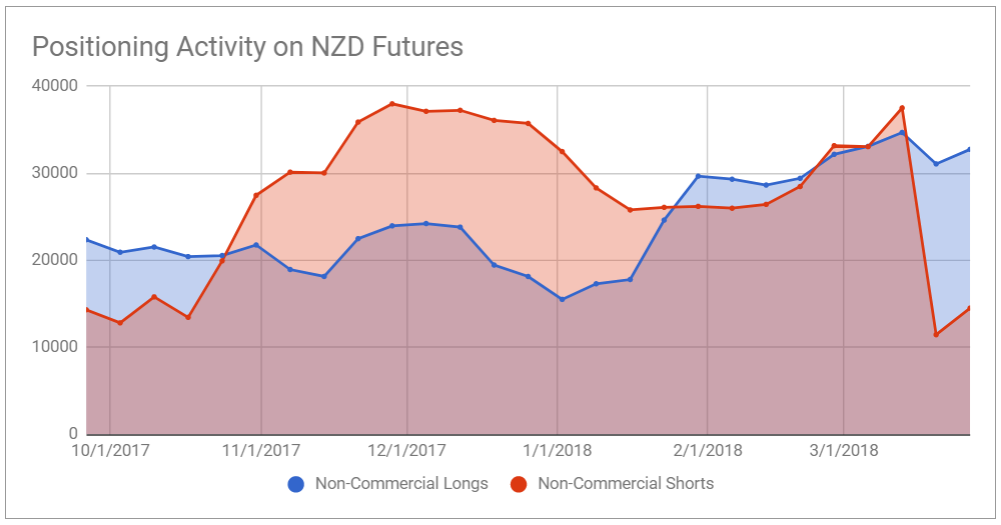

NZD

Large speculative traders have been net bearish on the Kiwi for most of Q1 2018. However, sentiment on the Kiwi appears to be changing since bulls have been steadily building up their positions throughout the quarter while bears slashed a large chunk of their positions late in March, particularly during the week ending on March 20.

The steady buildup in Kiwi longs might be positioning on the expectation that the RBNZ is still on course for a 2019 rate hike. In fact, the RBNZ’s projected path for the OCR still projects a rate hike by Q2 2019, as of the February RBNZ statement.

And in the March 20 RBNZ statement, the RBNZ even hinted that it wasn’t too worried with the Kiwi’s exchange rate since the RBNZ refrained from talking about the Kiwi’s trade weighted index (TWI).

As for the large drop in Kiwi shorts during the week ending on March 20, that was likely due to the RBNZ statement, which didn’t derail expectations for a 2019 RBNZ rate hike as well as refrained from talking down the Kiwi.

However, it’s also very likely that shorts were abandoning ship after adding to their bets in the runup to the FOMC statement since the Fed was expected to hike and then upgrade its projected path for the Fed Funds Rate to show three more hikes in 2018, thereby putting interest differentials into play in favor of the Greenback and at the expense of the Kiwi.

But as it turned out, the Fed did hike as expected but maintained its forecast of two more hikes this year, which likely convinced Kiwi bears to take some profits off the table.

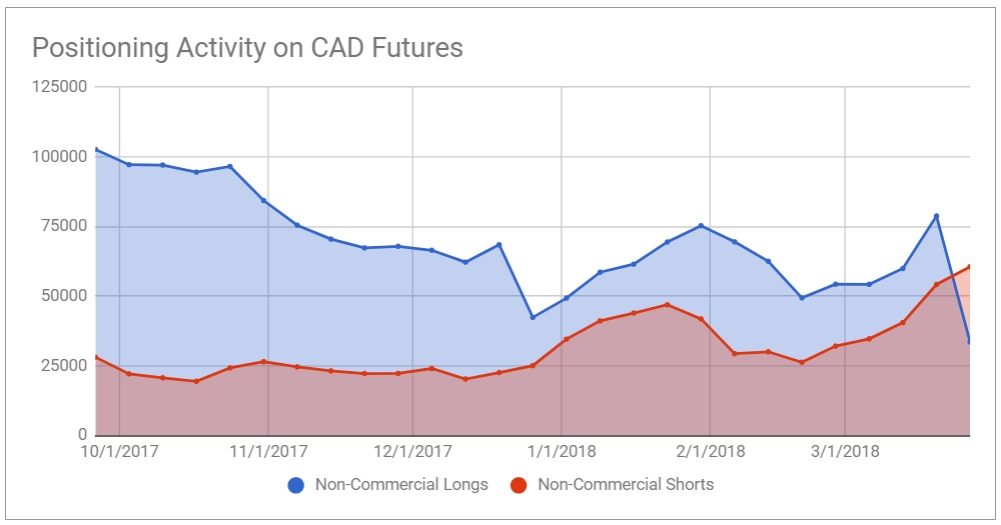

CAD

Net positioning on the Loonie has been bullish for a long time now. However, that came to an end when Loonie bulls slashed their positions during the week ending on March 27, pushing net positioning on the Loonie into bearish territory for the first time since since the week ending on July 11, 2017.

Aside from falling oil prices at the time, there was no clear catalyst that could have convinced Loonie bulls to exit their positions. However, it’s possible that we’re just seeing some profit-taking by bulls in order to avoid NAFTA-related uncertainty since talks are still ongoing.