Non-commercial forex traders slashed the value of their net long bets on the Greenback from $7.82 billion to $4.50 billion during the week ending on June 27, 2017, according to calculations done by Reuters

And the latest Commitments of Traders forex positioning report from the CFTC shows that the Greenback lost ground mainly to the Loonie and, to a lesser extent, the euro.

Also, positioning activity was actually mixed and the Greenback was able to take a large chunk of ground from the yen.

Oh, please keep in mind that the numbers below show the net positioning of non-commercial forex traders against the U.S. dollar.

And if you’re feeling overwhelmed by all these figures, you might need to review our School of Pipsology lesson on How to Gauge Market Sentiment Using the COT Report in order to learn how to pinpoint potential forex market reversals.

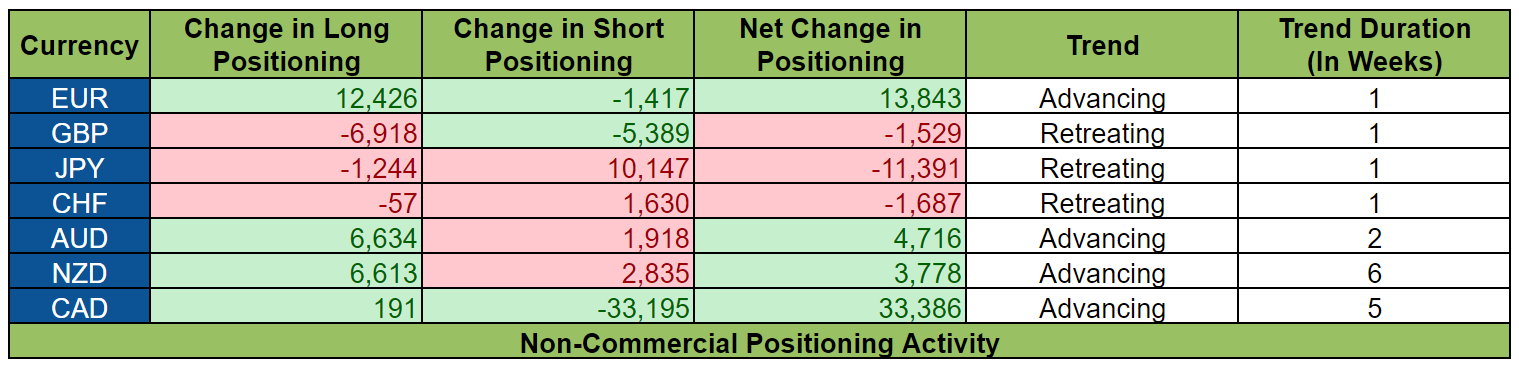

And here is how positioning activity played out during the week ending on June 27, 2017.

Positioning activity was actually mixed so catalysts for the other currencies were likely in play, rather than demand (or lack thereof) for the Greenback.

Having said that, the lack of broad-based demand for the Greenback two weeks after the Fed raised the target range for the Fed Funds Rate highlights the market’s lack of faith that the Fed can deliver on one more rate hike this year.

And sentiment on the Greenback probably didn’t get any help from the 1.1% drop in U.S. durable goods orders (-0.5% expected, -0.8% previous) and Markit’s flash reading for U.S. manufacturing and services PMI both deteriorating in June.

Okay, here are the major events, reports, and other catalysts for the other currencies:

EUR

The euro resumed its advance against the Greenback, thanks to the increase in euro longs and slight reduction in euro shorts.

This rather bullish positioning activity was very likely due to ECB President Draghi’s June 27 speech wherein he gave a very optimistic assessment and outlook on the Euro Zone economy. Draghi even highlighted that the factors that are weighing down on inflation are expected to temporary.

Finally, Draghi hinted at a potential shift in monetary policy bias when he said that the ECB “can accompany the recovery by adjusting the parameters of its policy instruments.”

Do note, however, that net positioning does not yet reflect how large players reacted to ECB Vice President Constancio’s CNBC interview wherein Constancio presented a more cautious tone.

Moreover, positioning activity does not yet reflect how speculators reacted when unnamed ECB officials were cited in a Bloomberg report as saying that the market may be “hypersensitive” and could have misjudged Draghi’s hawkish tone.

GBP

The pound was finally able to take back some ground during the previous week. However, that was quickly ended during the week ending on June 27, although a closer look at positioning activity shows that both pound bulls and pound bears were actually bailing their positions, with slightly more bulls than bears heading for the exit.

Positioning activity likely shows pound shorts getting spooked and profit-taking by pound bulls in the wake of BOE Chief Economist Haldane’s June 21 comments, which were surprisingly hawkish and a big contrast to BOE Governor Carney more dovish June 20 comments.

Even more surprising is the fact that Haldane is a well-known dove and he’s the chief economist, so his hawkish shift was a big event.

Other than that, shorts may have also been spooked by the June 26 news that the Conservatives and the DUP were able to finally hammer out a deal. After all, the deal is meant to provide more stability in government, reducing Brexit-related uncertainty in the process.

It should be noted, though, that Carney would later give a speech on June 28. And the market interpreted this speech as being much more hawkish compared to Carney’s June 21 speech. However, that hawkish speech is not reflected in the most recent COT report.

JPY

Yen shorts charged in and some yen bulls decided to pare their positions during the week ending on June 27.

And the very likely reason for this was that Draghi’s speech caused global bond yields to surge as speculation rose that the ECB may be tightening soon.

CHF

Sentiment on the Swissy sourced as large players slightly increased their short positions on the Swissy, which is weird because risk aversion dominated at the time. Also, there were no direct catalysts for the Swissy itself, which leaves us with monetary policy divergence, as mentioned earlier.

AUD

Sentiment on the Aussie continued to improve. And a quick look at positioning activity shows that was due to the increase in fresh Aussie longs, which was partially offset by a smaller increase in Aussie shorts.

The increase in Aussie longs was likely prompted by the surge in iron ore prices. And the surge in iron ore prices, in turn, was attributed by market analysts to speculation that demand of steel mills will pick up, as well as upbeat rhetoric from Chinese Premier Li Keqiang.

As for the increase in Aussie shorts, that may have been due to the Draghi-induced surge in bond yields at the time, which reduced the higher-yielding Aussie’s yield advantage. Also, risk aversion was the dominant sentiment at the time.

NZD

Large players also boosted their long bets on the Kiwi while slightly bumping up their bearish bets.

The increase in Kiwi longs was likely a positive reaction to the June 22 RBNZ statement since the RBNZ didn’t seem to worried about the slow growth in Q1 and didn’t try to talk down the Kiwi’s recent strength.

The slight increase in Kiwi shorts, meanwhile, may have also been due to the Kiwi’s reduced yield advantage because of the surge in bond yields, as well as the risk aversion at the time.

CAD

The Loonie took ground from the Greenback for the fifth consecutive week, thanks to the massive culling of Loonie shorts.

The large reduction in Loonie shorts was likely linked to climbing oil prices at the time. And oil was on the rise because of short-covering and heavy speculation that U.S. oil inventories would continue to fall, market analysts say.

Of course, we now know that U.S. oil inventories did not fall, but that U.S. oil production did, sending oil even higher.

Also, positioning on the Loonie does not yet show increased rate hike odds from the BOC after BOC Governor Poloz gave an upbeat view during a June 28 CNBC interview.

Got any other conclusions you can draw from this latest COT Report? Feel free to share your thoughts in the comments section or if you’re looking for further discussion, community member ForExchange has a lively thread called Trading based on Market Sentiment in the forums awaiting your participation.