Returning Greenback demand was short-lived since the value of net long positions on the U.S. dollar resumed its slide, decreasing from $7.45 billion to $6.88 billion during the week ending on March 8, 2016, according to calculations done by Reuters. And the latest Commitments of Traders forex positioning report from the CFTC shows that the Greenback lost ground to most of its forex rivals, particularly the Aussie.

Keep in mind that the numbers below show the net positioning of non-commercial forex traders against the U.S. dollar. If you’re feeling overwhelmed by all these figures, you might need to review our School of Pipsology lesson on How to Gauge Market Sentiment Using the COT Report in order to learn how to pinpoint potential forex market reversals.

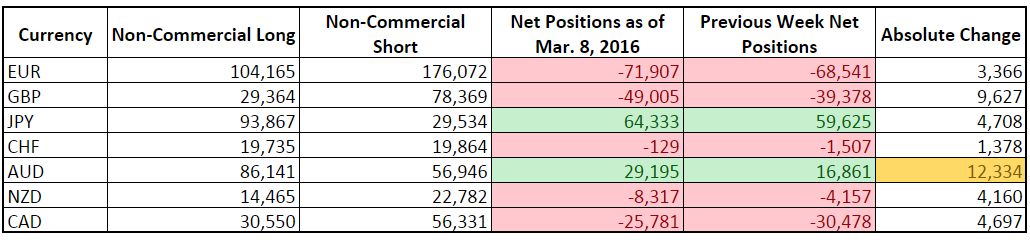

Lemme break down the latest numbers for y’all:

- The Greenback continued the previous week’s theme of losing ground to most of its other forex rivals while advancing against the pound and the euro. The Greenback can now list the Kiwi as one of its victims, however.

- The Kiwi lost ground to the Greenback because Kiwi bulls trimmed their long bets from 16,593 to 14,465 while Kiwi bears simultaneously increased their bets from 20,750 contracts to 22,782.

- Large peculators increased their bearish bias on the euro mainly by increasing their short positions on the euro from 172,506 contracts to 176,072.

- As for the pound, speculators increased their bearish bias primarily by drastically unwinding their long positions, reducing their bets from 38,965 contracts to 29,364.

- Non-commercial forex traders now seem very bullish on the Aussie dollar since they pumped up their bullish bets from 76,480 contracts to 86,141 while paring their short bets from 59,619 contracts to 56,946.

- They’re also still very bullish on the yen, but the increase in net bullish bets was mainly due to yen shorts slashing their positions from 34,445 contracts to 29,534.

- The Swissy is very close to winning out against the Greenback, thanks to Swissy short cutting down their positions from 21,230 contracts to 19,864.

- The Loonie is still slowly but surely taking more and more ground from the Greenback, as large speculative traders continue to unwind their shorts. Short bets on the Loonie have been unwinding for six consecutive weeks now while bullish bets on the Loonie show little change.

Looks like my assessment from last week that Greenback demand was being fueled at the euro’s expense rather than actual demand for the Greenback itself was right since the value of net long positions on the Greenback resumed its slide.

Demand for the Greenback probably became soft because of the most recent NFP report. Sure, employment saw a net increase of 242K which is much bigger than the expected 190K increase, but wages also declined by 0.1% instead of advancing by 0.2%. And the latter probably gripped the hearts and minds of forex traders since the U.S. Fed could use that to justify holding off on further rate hikes.

Moving onto the other currencies, demand for the Aussie was very likely jacked up by the RBA decisions to maintain the cash rate at 2.00% while sounding upbeat, as well as the better-than-expected reading for Australia’s Q4 2015 GDP and the commodities rally during the period.

The commodities rally also helps to explain how the Loonie was able to take a chunk of ground from the Greenback, although speculation that the BOC will maintain its monetary policy during the March 9 decision probably helped too. And we now know that the BOC did keep rates on hold while presenting a rather optimistic outlook.

The commodities rally should have pumped up demand for the Kiwi as well, but forex traders were probably betting that the RBNZ will cut rates or be dovish during the March 9 monetary policy decision. And it looks like they were right because we now know that the RBNZ did slash its official cash rate from 2.50% to 2.25%.

Moving on, the March 10 ECB policy decision was likely weighing down on the euro since traders were probably expecting more easing moves, given that ECB President Mario Draghi said in a February 15 statement that the ECB “will not hesitate to act” to act if needed, as I mentioned in last week’s write-up. Forex traders were probably not expecting that Draghi will say that further rate cuts may be no longer be necessary, however.

As for the Swissy and the yen, they were able to advance further at the Greenback’s expense and despite the prevalence of risk-appetite during this period. This probably had more to do with Greenback weakness rather than strength on the part of the Swissy and the yen, given that long positions on the two aforementioned currencies saw little change while short positions got slashed.

The only currency left is the pound. And the pound’s weakness was likely due to a slew of disappointing economic reports and renewed Brexit fears after BOE Governor Mark Carney testified before the Parliamentary Committee that a Brexit could result in “lower levels of activity because of the degree of uncertainty that could affect investment and household spending.” In short, a Brexit could negatively impact the British economy in the short-term.

Got any other conclusions you can draw from this latest COT Report? Feel free to share your thoughts in the comments section or if you’re looking for further discussion, community member ForExchange has a lively thread called Trading based on Market Sentiment in the forums awaiting your participation.