How y’all doing, forex friends! Canada will be simultaneously releasing its retail sales and CPI reports this Friday at 12:30 pm GMT. And that means that the Loonie will likely get a volatility injection.

And if you’re looking to pillage some quick pips from the Loonie before the week ends, then you better read up on today’s Event Preview.

Canada’s Retail Sales Report (March)

What happened last time?

- February retail sales m/m: +0.4% as expected

- January retail sales m/m: downgraded from +0.5% to +0.1%

- February core retail sales m/m: 0.0% vs. +0.4% expected

- January core retail sales m/m: upgraded from +0.9% to +1.0%

The previous retail sales report showed that headline retail sales in Canada increased by 0.4% month-on-month in February, which is in-line with consensus.

However, the reading for January was downgraded significantly from a solid +0.5% to a not-so-solid +0.1%.

The core reading, meanwhile, came in flat, which is rather disappointing since the consensus was for a 0.4% increase.

But on a more upbeat note, the core reading for January was upgraded slightly from +0.9% to +1.0%.

Looking at the details of the report, only 4 of the 11 subsectors reported increases in retail sales. And one of them happens to be the motor vehicle and parts dealers.

However, sales from motor vehicles and parts dealers are not included in the core reading, which is why the core reading came in flat.

In summary, the February retail sales report was mixed on the surface but was rather poor overall.

What’s expected this time?

- Headline retail sales m/m: +0.3% expected vs. +0.4% previous

- Core retail sales m/m: +0.5% expected vs. 0.0% previous

For the upcoming retail sales report, the consensus among economists is that headline retail sales moderated further in March (+0.3% expected vs. +0.4% previous) while the core reading is expected to rebound (+0.5% expected vs. 0.0% previous).

There’s therefore also an implied consensus that vehicle sales eased while non-vehicle sales ramped up.

So, do the leading and related economic indicators offer any clues?

- Canada’s March jobs report showed that the wholesale and retail trade industries axed 5.9K jobs.

- Canada’s April jobs report revealed that the wholesale and retail trade industries lost an additional 22.1K jobs.

- The jobs reports also show a steady increase in wage growth, which could lead to stronger consumer spending.

- Canada’s March trade report reveals that imports of motor vehicles and parts surged by 8.3% (+2.8% previous).

- The trade report also shows that imports of consumer goods surged by 7.7% (+1.9% previous).

Aside from the reduction of employees working at the wholesale and retail trade industries, the leading and related economic reports are pointing to a potential pickup in retail sales.

However, the trade report shows that imports of vehicles and parts also increased in March.

And that implies that vehicle sales ramped up, which goes against the implied consensus that non-vehicle sales drove retail sales while vehicle sales slowed, given that the headline retail sales reading is expected to ease further while the core reading is expected to rebound.

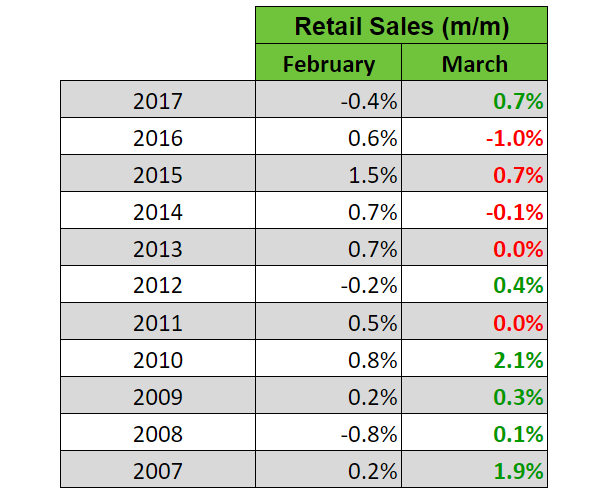

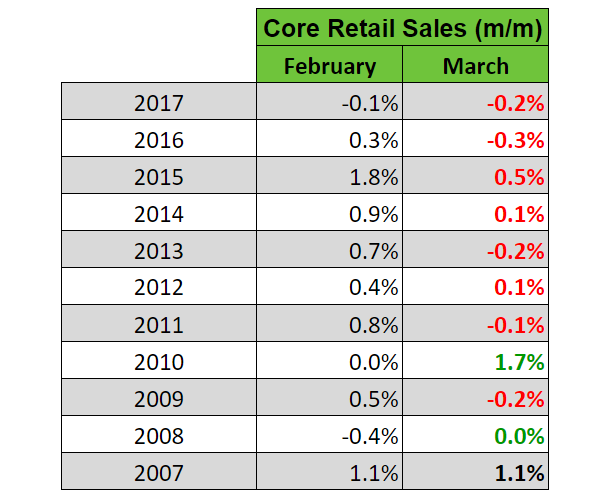

Okay, what about historical tendencies? Do they offer additional clues?

Well, historical data are contrary to the consensus since headline retail sales tend to be stronger in March compared to February while the core reading has been historically weaker. It should be pointed out, however, that the March headline reading was weaker from 2013-2016 but followed historical norms again last year.

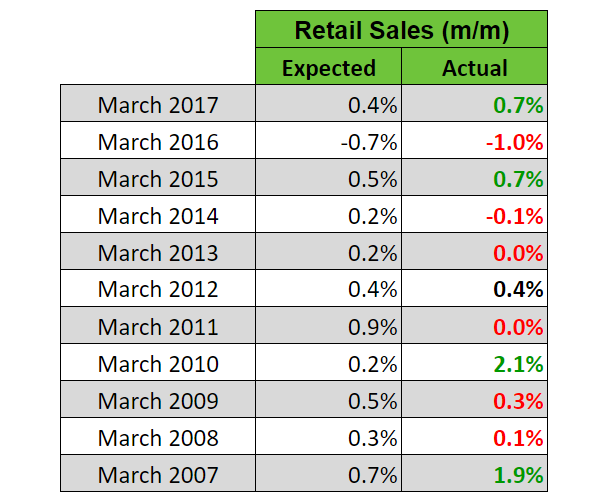

As to how economists fared with their guesstimates, they have a mixed performance when it comes to headline reading. Although there are more downside surprises.

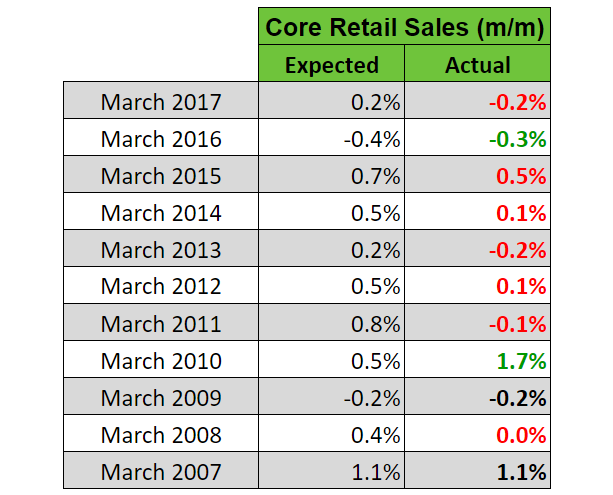

As for the core reading, economists have a clear tendency to be too optimistic with their guesstimates, resulting in more downside surprises.

In summary, the leading and related indicators and reports are pointing to the possibility of a pickup in both headline and core retail sales readings.

The potential pickup for the core reading is in-line with consensus but a stronger headline reading is not.

Historical trend, meanwhile, go against the consensus since the headline reading usually strengthens while the core reading deteriorates.

Historical trends also show that economists tend to be too optimistic with their guesstimates, resulting in more downside surprises for the core reading, and to a lesser degree, the headline reading as well.

Probability therefore appears skewed slightly more towards a downside surprise, based on the historical trends. Although I wouldn’t be too surprised if the headline reading comes in better-than-expected, given the surge in imports of vehicles and parts.

Anyhow, just remember that we’re playing with probabilities here, so there’s also still a chance that both headline and core readings may surprise to the upside. After all, Canada’s March trade report also showed a surge in import of consumer goods.

Canada’s CPI Report (April)

What happened last time?

- Headline CPI m/m: +0.3% vs. +0.4% expected, +0.6% previous

- Headline CPI y/y: +2.3% vs. +2.4% expected, +2.2% previous

- Trimmed Mean CPI y/y: +2.0% vs. +2.1% previous

- Weighted Median CPI y/y: steady at +2.1%

- Common Component CPI y/y: steady at +1.9%

Canada’s March CPI report revealed that headline CPI only increased by 0.3% month-on-month, which is a tick slower than the expected 0.4% rise and marks the second month of ever weaker monthly readings to boot.

Year-on-year, headline CPI only increased by 2.3%, missing expectations for a 2.4% increase.

But on a more upbeat note, the +2.3% reading is the strongest since October 2014 and marks the second month of stronger annual readings.

But on a more downbeat note, the stronger reading in March was driven mainly by gasoline prices. If gasoline prices are excluded, then headline CPI only increased by 1.8% in March, matching the rate of annual increase reported in February.

As for the BOC’s three preferred measures for the “core” reading, the Weighted Median CPI and Commom Component CPI were both steady at +2.1% and +1.9% respectively.

However, the Trimmed Mean CPI was a disappointment since it eased from +2.1% to +2.0%.

Overall, the March CPI report was disappointing on the surface and the details didn’t really take away the disappointment.

What’s expected this time?

- Headline CPI m/m: +0.4% expected vs. +0.3% previous

- Headline CPI y/y: steady at +2.3% expected

Most economists forecast that headline CPI rose by 0.4% month-on-month in April, which is a stronger rise compared to the 0.3% increase recorded in March.

The year-on-year reading, meanwhile, is expected to maintain last month’s pace by coming in at +2.3%.

So, what do the available leading indicators have to say?

- The prices index of the Ivey PMI report jumped from 60.0 to 67.8 in April. The prices index refers to input prices, but higher input prices usually translate to higher CPI, provided that companies pass on their higher input costs to consumers.

- Markit’s manufacturing PMI report corroborates Ivey’s finding since Markit found that “The latest increase in overall cost burdens was the steepest since March 2014.” More importantly, Canadian manufacturers are passing on their higher costs since “Sharply rising operating expenses and resilient demand conditions led to the fastest increase in average prices charged by manufacturers for exactly seven years.”

Both Ivey and Markit suggest that input costs ramped up. And according to Markit, Canadian manufacturer are passing on their higher costs, so much so that factory gate price inflation hit a seven-year high in April.

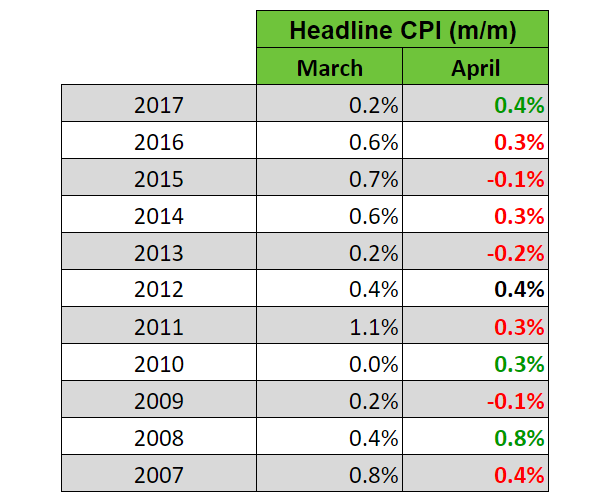

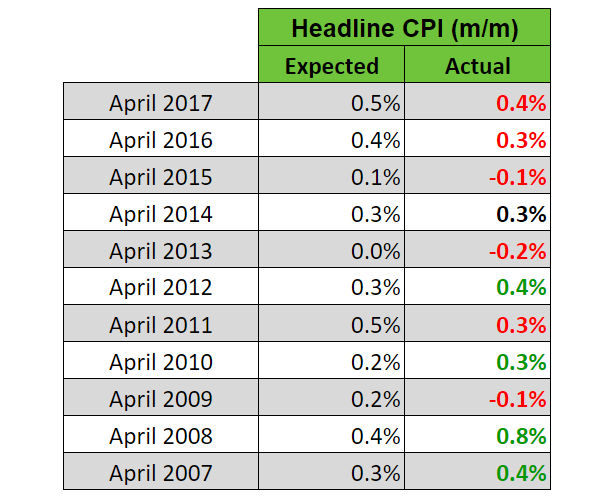

What about historical tendencies?

Well, CPI usually decelerates month-on-month between March and April. This obviously goes against the consensus as well as the hints from the PMI reports.

Also, economists tend to overshoot their guesstimates since there are more downside surprises. In fact, we have been getting downside surprises for the past three years.

To summarize, the leading indicators point to higher input costs in April. And Markit even found that manufacturers are passing on their costs, which is an argument in favor of a stronger monthly reading for headline CPI. And that’s in-line with consensus.

However, historical trends don’t support the consensus since monthly CPI usually slows down between March and April.

Furthermore, historical data show that economists tend to overshoot their guesstimates, resulting in more downside surprises.

Probability therefore appears to lean more towards a downside surprise, at least for the monthly CPI reading.

But again, just keep in mind that we’re playing with probabilities here, so there’s no guarantee that the monthly reading will surprise to the downside.

Final Thoughts

Canada’s retail sales and CPI reports will be released simultaneously this Friday, just like last time.

As usual, just remember that if both top-tier reports disappoint, then the Loonie usually gets sold off.

Conversely, if both top-tier reports were to beat expectations, then that would likely propel the Loonie higher.

However, if the reports come in mixed, then it’s the CPI report that usually takes precedence because of its more direct link to monetary policy.

And Loonie’s reaction to the previous reports is an example of this since the retail sales report was mixed on the surface (but negative overall) while the CPI report was a disappointment.

Overlay of CAD Pairs: 15-Minute Forex Chart

As for follow-through buying or selling, that usually depends on oil prices, so you may also want to keep an eye on oil prices as well.

And if you didn’t know, you can check out oil prices at our Live Market Rates page.