Large players trimmed their net bearish positions on the Greenback even further, with the value of net short positions on the U.S. dollar falling from $12.65 billion to $8.02 billion during the week ending on October 24, according to calculations done by Reuters. This marks the fourth consecutive week of easing bearish bias on the Greenback.

And the latest Commitments of Traders (COT) forex positioning report from the CFTC reveals that the Greenback took ground from ALL its peers, but the yen was particularly vulnerable and lost a large chunk of ground to the Greenback, thanks to the large increase in short bets on the yen.

Oh, please keep in mind that the numbers below show the net positioning of non-commercial forex traders against the U.S. dollar.

And if you’re feeling overwhelmed by all these figures, you might need to review our School of Pipsology lesson on How to Gauge Market Sentiment Using the COT Report in order to learn how to pinpoint potential forex market reversals.

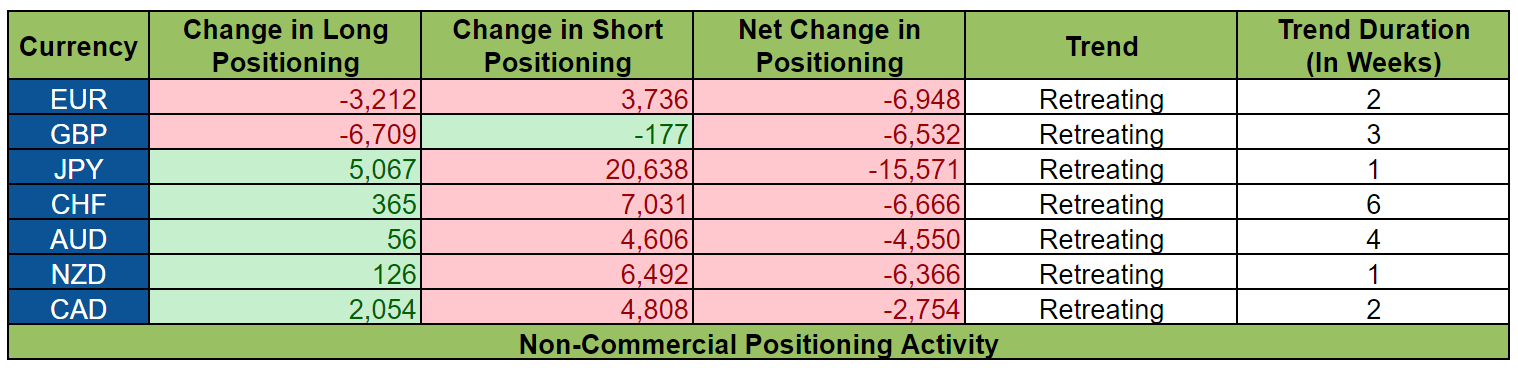

And here is how positioning activity played out during the week ending on October 24, 2017.

Large speculators became even less bearish on the Greenback. And positioning activity shows that there was a build-up of short positions on the Greenback’s forex rivals, with the exception of the pound.

And large players opened fresh bearish bets against the forex rivals likely as a reaction to the U.S. Senate’s decision to pass the 2018 budget blueprint since that’s the first step to making it easier to push through with Trump’s tax plans.

After all, the budget blueprint includes “budget reconciliation” which will allow the U.S. Senate to pass certain legislation (which include Trump’s tax reform plans) with only a majority vote (50+1) in the Senate instead 60 votes, which greatly increases the chance that Trump’s tax plans may be passed, given that the Republicans currently control 52 seats in the Senate.

Aside from reflecting how large players reacted to the U.S. Senate’s decision, it’s also likely that large players were opening preemptive bets on the expectation that the House of Representatives would also pass the 2018 budget plan.

Of course, we now know that the House did pass the 2018 budget blueprint, but the COT report does not yet reflect that development.

Other than that, it’s also likely that demand for the Greenback was spurred by speculation on who the next Fed Chair would be.

And back on October 24, there was a widely-circulated a Bloomberg report that claimed that Trump asked the Republican senators on they prefer to be the next Fed Chair. And according to South Carolina Senator Tim Scott,“Taylor won.”

And to put that into its proper context, do note that Taylor is perceived as one of the more hawkish Fed Head candidates.

Okay, here are the major events, reports, and other catalysts for the other currencies:

EUR

Positioning activity on the euro was rather bearish since euro bears buttressed their positions while euro bulls eroded theirs. This marks the second week of easing bullish bias on the euro.

And aside from demand for the Greenback at the expense of the euro, the increase in euro shorts likely reflects preemptive positioning ahead of the ECB statement.

We now know that the ECB delivered a dovish taper when it announced that it plans to extend its QE program by nine months starting next year but at half the current monthly pace while maintaining an easing bias on its QE program. The most recent COT report does not yet reflect how large players reacted to that, though.

As for the increase in euro longs, that was likely due to profit-taking ahead of the ECB statement. Although jitters over Catalonia amid Spain’s declaration that it plans to trigger Article 155 of the 1978 Spanish Constitution in order to remove Catalonia’s autonomy also likely helped to dampen demand for the euro and may have even convinced fresh euro shorts to jump in.

GBP

The pound continues to retreat against the Greenback. And as has been the case in the past couple of weeks, sentiment on the pound soured because pound bulls were abandoning ship.

And the culling of pound longs likely reflects continued disappointment over the not-so-hawkish comments by BOE MPC Members BOE’s Carney, Tenreyro, and Ramsden when they testified before the U.K. Treasury Select Committee on October 20, as well as Jon Cunliffe’s not-so-confident message to the Western Mail

JPY

After a brief stop during the previous week, sentiment on the yen resumed its deterioration, thanks to a rather large influx of yen shorts.

But interestingly enough, there was also an increase in yen longs, likely because of safe-haven demand for the yen because of fears related to Catalonia at the time.

However, there were far more yen shorts, very likely because of Shinzo Abe’s victory in the elections, which likely means that the BOJ’s will continue with its loose monetary policy even longer, which highlights the growing monetary policy divergence between the BOJ and the Fed.

Also, global bond yields were surging at the time, which likely soured sentiment on the yen as well.

CHF

Swissy longs only slightly increased while Swissy shorts increased substantially, which likely reflect the growing monetary policy divergence between the SNB and the Fed.

AUD

Aussie longs were essentially unchanged while Aussie shorts saw a respectable increase.

The lack of demand for the Aussie while growing bearish bias may just show positioning in favor of the Greenback at the Aussie’s expense. However, it’s also possible that continued disappointment over the RBA’s latest meeting minutes may have continued to weigh on sentiment on the Aussie.

NZD

Kiwi shorts saw a noticeable increase while the increase in Kiwi longs was only very minimal.

And the likely reason why Kiwi shorts were eager to jump in while Kiwi longs didn’t seem to want to was the news that NZF chose to back Labour in order to form a government.

Also, new NZ Prime Minister Adern gave a speech on October 24 and she said that her newly-formed government has “been looking at changing the objectives set out in the Reserve Bank Act” to “possibly include employment,” which likely stoked fears that the RBNZ may be forced to push rate hikes even later.

CAD

Overall sentiment on the Loonie deteriorated since the increase in Loonie shorts was able to overwhelm the increase in Loonie longs. And this mixed positioning activity likely reflects preemptive positioning ahead of the BOC statement.

We now know that the BOC statement wasn’t too good for the Loonie, however, since the BOC hinted at a more cautious monetary policy bias. Do note that the COT report does not yet show how large players reacted to the BOC statement itself, though.

Got any other conclusions you can draw from this latest COT Report? Feel free to share your thoughts in the comments section or if you’re looking for further discussion, community member ForExchange has a lively thread called Trading based on Market Sentiment in the forums awaiting your participation.