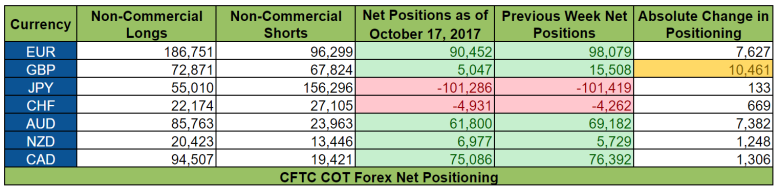

Large speculator became even less bearish on the Greenback since they further reduced the value of their net short positions on the U.S. dollar from $15.42 billion to $12.65 billion during the week ending on October 17, according to calculations done by Reuters.

And the latest Commitments of Traders (COT) forex positioning report from the CFTC reveals that the improved sentiment on the Greenback was broad-based, but the Greenback took ground mainly from pound, the euro, and the Aussie.

Oh, please keep in mind that the numbers below show the net positioning of non-commercial forex traders against the U.S. dollar.

And if you’re feeling overwhelmed by all these figures, you might need to review our School of Pipsology lesson on How to Gauge Market Sentiment Using the COT Report in order to learn how to pinpoint potential forex market reversals.

And here is how positioning activity played out during the week ending on October 17, 2017.

Bearish bias on the Greenback eased even further during the week ending on October 17, very likely because of speculation that Trump may choose a more hawkish Fed Chair to replace Yellen, with either Powell or Taylor supposedly being the mostly likely candidates.

Other than that, the improved sentiment on the Greenback also likely reflects speculation that the U.S. Senate would vote in favor of the 2018 fiscal budget blueprint since the budget proposal includes provisions on budget reconciliation, which would make passing Trump’s tax plans somewhat easier since only a majority or 51 votes would be needed in the U.S. Senate instead of the usual 60 votes.

This means that if the Republicans are united then their 52 seats in the Senate are all that’s needed in order to push forward a tax package.

And we now know that the U.S. Senate decided to approve the budget blueprint and that the Greenback reacted very positively, but the most recent COT report does not yet reflect that.

Anyhow, here are the major events, reports, and other catalysts for the other currencies:

EUR

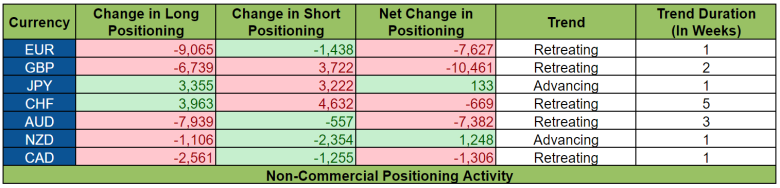

After three consecutive weeks of increases, bullish bias on the euro finally eased. However a closer look at positioning activity shows that both euro bulls and euro bears slashed their respective bets. Significantly more euro longs got culled, though, which is why bullish bias on the euro eased.

Aside from improving sentiment on the Greenback at the euro’s expense, the slashing of euro longs likely reflects renewed concern over Catalonia’s bid for independence, which ultimately culminated in Spain giving Catalonia an ultimatum to stop seeking independence, warning that failure to do so will result in the loss of Catalonia’s autonomy.

And since Catalonia refused, Spain moved to trigger Article 155 of the 1978 Spanish Constitution in order to gain direct control over Catalonia. Although the latest COT report does not yet reflect how large players reacted to that.

Aside from profit-taking by euro bulls because of Catalonia, it’s also likely that some euro bulls were unwinding their bets ahead of the October 26 ECB statement since ECB President Draghi did say in his October 13 speech that “Progress towards a durable and self-sustaining convergence of inflation towards our objective is not yet sufficiently convincing … Thus, a very substantial degree of monetary accommodation is still needed.”

GBP

The pound lost another chunk of ground to the Greenback as pound bulls called it quits while fresh pound bears jumped in.

This rather bearish positioning activity on the pound was very likely driven by the not-so-hawkish comments by BOE MPC Members BOE’s Carney, Tenreyro, and Ramsden when they testified before the U.K. Treasury Select Committee on October 20.

As for specifics, Dave Ramsden explicitly stated that he dissented from the majority opinion because he does not think a rate hike would be appropriate “in the coming months” because of weak wage growth.

Silvana Tenreyro, meanwhile, said that she’s hawkish but she also expressed concern about the weak wage growth, adding that she’s worried that hiking prematurely may force the BOE to slash rates in the future.

As for Mark Carney, he also said that he’s a hawk but he gave off a cautious vibe when he expressed concern about the negative impact of Brexit on the U.K. economy. Also, Carney said that “The sole reason that inflation has gone up as much as it has is the depreciation of sterling,” which implies that underlying demand did not drive up inflation at all.

JPY

Net change in positioning on the yen was only very minimal, but sentiment on the yen did slightly improve very slightly after deteriorating for three straight weeks.

A closer look at positioning activity shows that yen bulls and yen bears were reinforcing their respective positions, however, with the bulls having a slight advantage.

The increase in yen longs was probably due to safe-haven demand for the yen because of renewed jitters over Catalonia. As for the increase in yen shorts, that likely reflects continued positioning against the yen because of monetary policy divergence between the Fed and the BOJ.

CHF

Like the yen, net change in positioning on the Swissy was only minimal. Also like the yen, Swissy bulls and Swissy bears were ramping up their respective bets.

Unlike the yen, however, Swissy bears had a slight advantage so net positioning on the Swissy was pushed deeper into bearish territory.

Like the yen, the increase in Swissy longs was probably due to safe-haven demand for the Swissy while the increase in Swissy shorts was probably because of monetary policy divergence between the SNB and the Fed.

AUD

Net bullish positioning on the Aussie continued to degrade, thanks to the trimming of Aussie longs.

And large players slashed their Aussie longs likely because of falling gold prices at the time, as well as disappointment over the RBA’s latest meeting minutes since the minutes did not provide any forward guidance, which implies that the RBA is not ready to budge from its current monetary policy.

Moreover, the minutes even noted that “Members observed that moves towards higher interest rates in other economies were a welcome development, but did not have mechanical implications for the setting of policy in Australia,” which reinforces the idea that the RBA is not in a hurry to hike anytime soon.

NZD

The Kiwi was able to push back against the Greenback since the decrease in Kiwi shorts were more than the decrease in Kiwi longs.

And the reduction in both Kiwi longs and Kiwi shorts likely reflects unwinding ahead of New Zealand First’s (NZF) announcement on who to back in order to form a government in New Zealand, given that NZF’s Peters said on October 13 that NZF may finally be able to come to a decision on whether to back National or Labour before the end of the October 16-20 trading week.

Of course, we now know that NZF chose to support Labour, which caused the Kiwi to tank rather hard. However, the most recent COT report does not yet reflect that.

CAD

The Loonie finally took a step back after taking ground from the Greenback for four consecutive weeks. Although a closer look at positioning activity shows that this was due to the paring of Loonie longs, which exceeded the reduction in Loonie shorts.

And more bulls were abandoning ship than bears likely because of worries related to NAFTA negotiations after the U.S. made fresh demand and after Trump reiterated this threat that the U.S. is ready to walk away.

This fear was likely excacerbated when a Bloomberg report cited unnamed “officials familiar with the [NAFTA] negotiations” as saying that an agreement by December of this year is unlikely, adding that “talks are likely to drag on for months.”

Got any other conclusions you can draw from this latest COT Report? Feel free to share your thoughts in the comments section or if you’re looking for further discussion, community member ForExchange has a lively thread called Trading based on Market Sentiment in the forums awaiting your participation.