In my previous intermarket correlations update, I’ve shown y’all how risk sentiment being in the driver’s seat has reinforced some correlations. This time, I’m seeing the Canadian dollar and crude oil going separate ways while the rest continue to work on their positive relationships.

For the newbie traders out there, don’t forget to review our School lesson on forex correlations before reading on!

USD/CAD vs. Crude Oil

Back in late July and August, market participants had been keeping close tabs on inventory data from the API and EIA to gauge if the global glut is still a concern.

However, Hurricane Harvey soon stole the spotlight on expectations of oil refineries being temporarily shut down in the Gulf area. For the most part of September, crude oil was buoyed higher by falling stockpiles, projections of stronger global demand in 2018, and expectations of an OPEC deal extension.

In contrast, the Loonie was being dragged lower on weakening odds of another BOC interest rate hike before the end of the year. Around that time, Canada had been printing one downbeat report after another, and it didn’t help that BOC policymakers had expressed concerns about CAD strength.

So far this month, crude oil has been recovering from its brief pullback while USD/CAD has popped higher before, during, and after the BOC decision as December hike hopes were dampened.

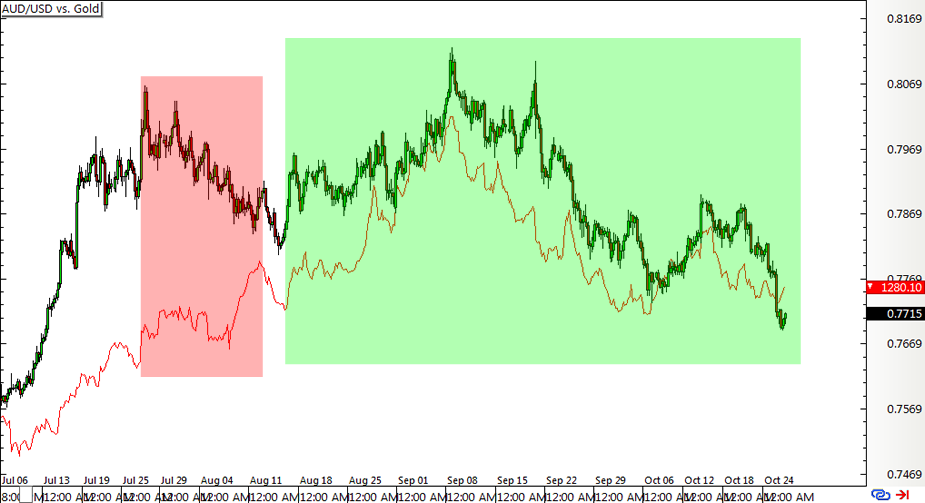

AUD/USD vs. Gold & Iron Ore

The relationship between the Aussie and the precious metal was on the rocks in late July and early August as risk aversion caused gold’s safe-haven quality to shine while the higher-yielding currency was dragged down.

At that time, tensions with North Korea were heightened while the RBA’s neutral stance didn’t exactly encourage traders to buy up the Aussie. The situation started to shift in mid-August, though, as AUD/USD eventually joined in the precious metal’s rally.

And even though gold peaked at the start of September, AUD/USD didn’t leave it behind as it joined in the commodity’s slide as well. This correlation continued to hold up pretty well for the rest of the month until today.

However, there are signs that gold could regain some ground while things aren’t looking too good for the Aussie. For one, the quarterly CPI report from the Land Down Under came in much weaker than expected, which could continue to hurt RBA tightening chances.

EUR/JPY vs. S&P 500 Index

Last but most certainly not least is EUR/JPY and S&P 500, which are often considered barometers of risk sentiment.

The currency pair and the equity index had been moving in lockstep for most of August and until the first week of September. ECB tightening expectations strengthened around the middle of the month, driving EUR/JPY higher, even as the S&P 500 index cruised sideways.

By the time risk appetite and optimism for U.S. tax reform returned, the S&P 500 index resumed its climb but it was EUR/JPY’s turn to lag behind. It does look like the currency pair is starting to catch up, though, especially after the Japanese elections revived bullish momentum.

To sum up, it appears that separate market forces are coming back into play for different asset classes, shaking up some intermarket correlations while reinforcing others. Monetary policy biases also returned to the spotlight, which has led to currency-specific action for the Loonie, Aussie, and euro.