A cooler-than-expected June inflation print set the tone for Tuesday, knocking the dollar to the bottom of the majors as traders unwound bets on a July Fed rate hike. Oil extended Monday’s surge on a fresh round of U.S. strikes against Iran, while stocks, gold, and Bitcoin all pushed higher into the close. Fed Chair Kevin Warsh then leaned against the dovish read in congressional testimony, trimming some of the early move without reversing it.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- New Zealand NZIER Business Confidence for Q2 2026: 8.0% (-8.0% forecast; -4.0% previous)

- New Zealand Visitor Arrivals for May 2026: 6.7% y/y (4.5% y/y forecast; 8.0% y/y previous)

- U.K. BRC Retail Sales Monitor for June 2026: 1.7% y/y (2.5% y/y forecast; 3.4% y/y previous)

- Australia Westpac Consumer Confidence Change for July 2026: 4.1% (2.5% forecast; -2.9% previous)

- Australia NAB Business Confidence for June 2026: -5.0 (-12.0 forecast; -14.0 previous)

- China Balance of Trade for June 2026: 125.62B (110.0B forecast; 105.43B previous)

- Japan Industrial Production Final for May 2026: -2.1% y/y (-1.7% y/y forecast; 2.0% y/y previous)

- Germany Wholesale Prices for June 2026: 4.9% y/y (6.2% y/y forecast; 5.9% y/y previous)

- Swiss Producer & Import Prices for June 2026: -2.1% y/y (-1.9% y/y forecast; -1.8% y/y previous)

- U.S. NFIB Business Optimism Index for June 2026: 97.4 (96.0 forecast; 95.3 previous)

- U.S. ADP Employment Change Weekly for June 27, 2026: 19.75k (21.0k previous)

-

U.S. CPI Growth Rate for June 2026: 3.5% y/y (3.9% y/y forecast; 4.2% y/y previous)

- U.S. Core Inflation Rate for June 2026: 2.6% y/y (2.9% y/y forecast; 2.9% y/y previous)

Promoted: Scale Your Strategies

A softer-than-expected CPI print sent the dollar to the bottom of the majors on Tuesday, only for Warsh’s testimony to claw part of the move back within hours. Navigating whipsaws like that requires more than a good entry, it requires a partner that has seen it all before.While new firms come and go with the volatility, The5ers (4.7★ rating on 32K+ reviews) has spent the last 10 years perfecting a funding model that works for the trader. It’s why over 1.6 million traders worldwide trust them to provide the capital and scaling needed to turn market analysis into meaningful professional growth.

Learn more about The5ers & available discounts

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

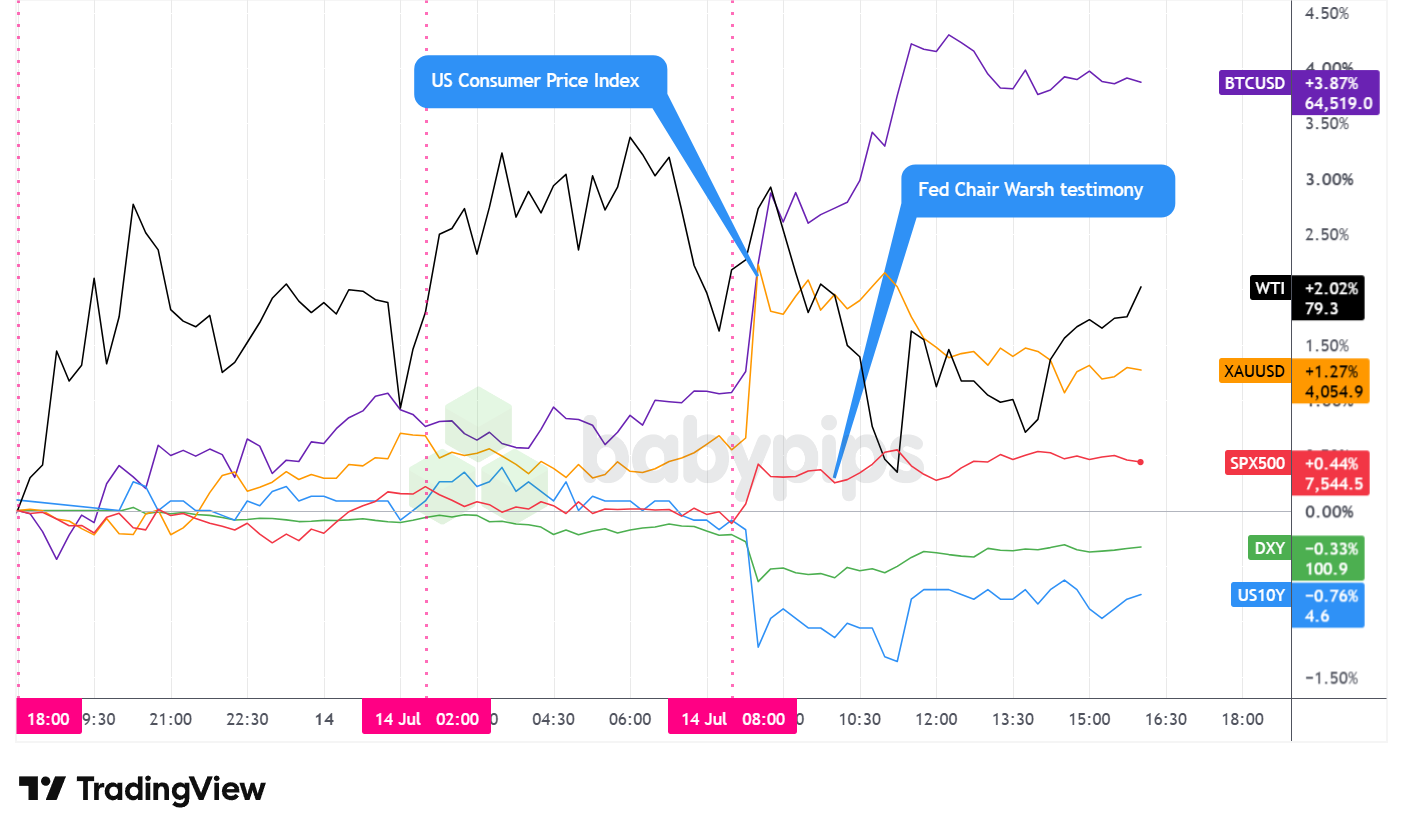

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

The June CPI report was the session’s pivot. Consumer prices fell 0.4% on the month, the first monthly decline in six years and well below the flat reading economists expected, dragging the annual rate down to 3.5% from 4.2%. Core inflation was unchanged on the month and eased to 2.6% year-over-year, also softer than forecast. Risk assets took the print as a green light, and the reaction rippled across every board on the overlay.

The S&P 500 finished up roughly 0.44%, closing near 7,545. The index spent the Asian and London hours chopping in a tight range around 7,510 on the individual chart, then gapped up toward 7,530 on the CPI release and pushed to a session high near 7,567 before settling into the low 7,550s. Big-bank earnings at the start of the reporting season and a rally in chipmakers gave the advance some fundamental support, though a sharp drop in one large-cap tech name capped the broader tape.

Gold closed up around 1.27% near 4,055. The metal’s path was choppier than the number suggests. It climbed steadily through the overnight hours from near 4,002 toward 4,034, then spiked hard on the CPI print to a session high around 4,103 before giving half of that back through the afternoon. The softer inflation read and the accompanying pullback in yields likely supported the initial jump, though the fade into the close suggests the safe-haven bid struggled to hold against firmer oil.

Bitcoin was the standout, finishing up roughly 3.87% near 64,519. It ground higher through the Asian and London sessions from around 62,000, then broke out on the CPI release, running to a session high near 64,918 before flattening out in the mid-64,000s. With no crypto-specific catalyst driving the move, the rally looks tied to the same softer-inflation, lower-yield backdrop that lifted the rest of the risk complex.

WTI crude closed up around 2.02% near 79.3, extending Monday’s rally of more than 9%. The strength was likely due to a third consecutive night of U.S. strikes on Iran and the reinstated naval blockade of Iranian shipping, with WTI trading above 80 during the London morning before pulling back. Crude peaked near 80.52 in the early hours, sold off to a session low near 77.42 around midday, then recovered into the high 79s. President Trump’s decision to shelve a proposed 20% fee on Strait of Hormuz cargo, announced Tuesday afternoon, coincided with some of the early US session pullback, though prices firmed again afterward heading into the close.

The U.S. 10-year Treasury yield fell around 0.76% to near 4.58%. The yield held near 4.60% overnight before dropping sharply on the CPI print to a session low near 4.535%, then stabilizing in the high 4.5s. The move fits the broader unwind of rate-hike bets, with short-dated Treasuries outperforming as money markets pushed the likely timing of the next Fed move further out.

Promoted: Have a solid trading strategy but lack the capital?

Tuesday’s CPI reaction was a two-part move: a fast dollar sell-off on the print, then a choppy rebound after the London close as Warsh pushed back. Trading news like that takes room to breathe. FundedNext empowers disciplined traders by providing simulated trading accounts up to $200K.Unlike other prop firms, FundedNext imposes no artificial time limits on challenges. You even earn a unique 15% profit share during your evaluation! Once funded, you keep up to a 95% profit split with guaranteed 24-hour payouts. Trade CFDs or Futures your way, even during major news events.

Join over 400K traders who have received $300M+ in payouts. Ready to back your edge?

Learn More About FundedNext! Limited time offer: Use code BPFN for discounts on both CFD & Futures plans! T&C apply.

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

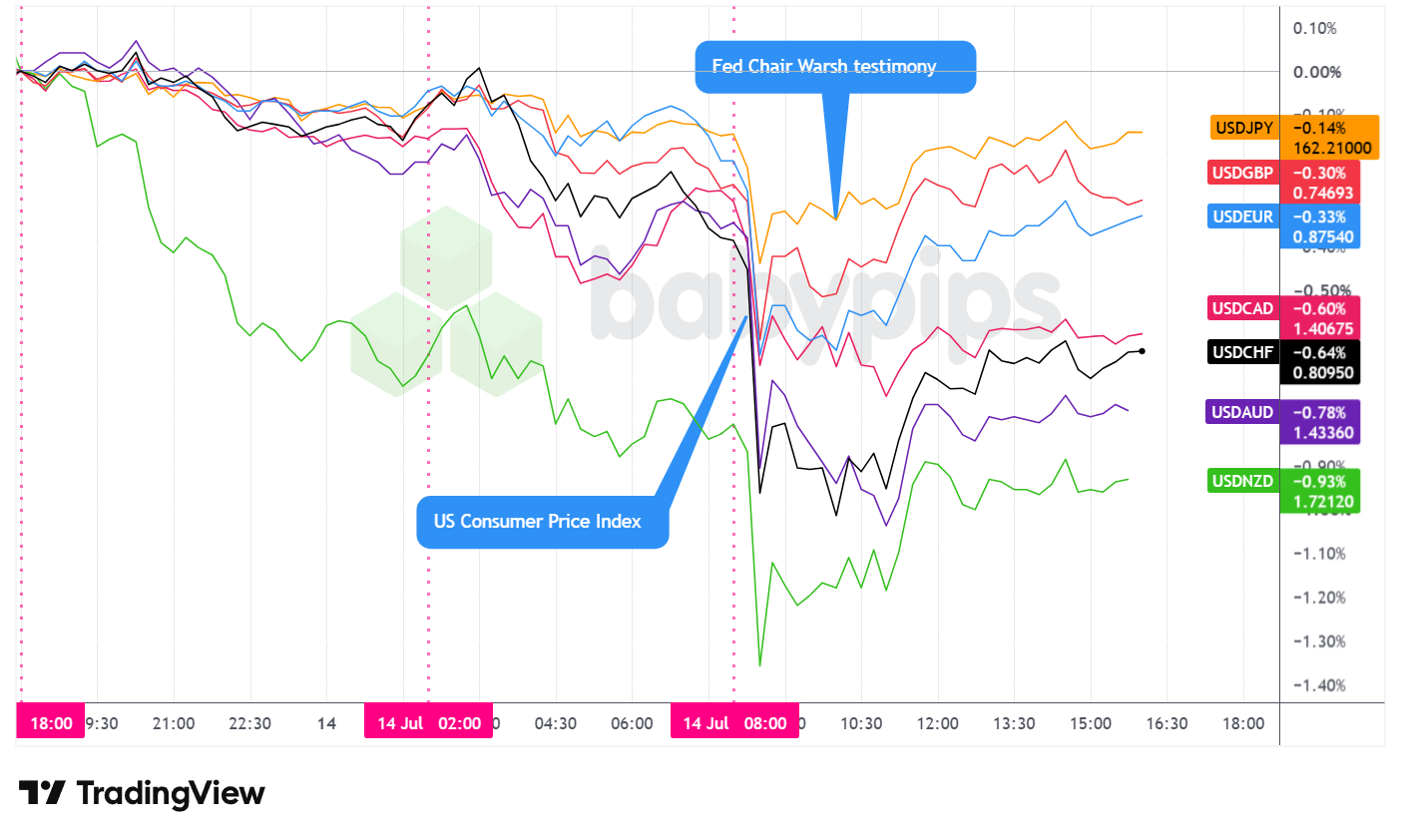

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar was the worst-performing major currency on the day, sliding against all seven of its peers on the overlay.

From the Asian open through the U.S. session open, the dollar drifted steadily lower against the majors. The CPI release then triggered a fast, broad leg down as traders unwound July rate-hike bets, with the greenback hitting its session lows within minutes of the print before quickly stabilizing and trading sideways through the London close.

After the London close, the dollar rebounded off those lows, stabilized, and traded choppily through the end of the session. An argument could be made that Warsh’s testimony helped underpin the bounce, as the Fed chair leaned against the dovish read and reminded lawmakers that policymakers have little patience for elevated inflation. The recovery pared the dollar’s losses without erasing them, leaving it lower across the board at the close.

The kiwi’s outperformance had its own fundamental thread. Comments from RBNZ chief economist Conway reinforcing the central bank’s hawkish framing, confirming last week’s hike to 2.5% and signaling the RBNZ would respond further if Middle East-linked inflation proves persistent. That forward guidance likely gave the currency a clean tailwind on top of the broad dollar selling.

Promoted: Protecting your trading capital starts with securing your access. Don’t let a weak password be the single point of failure for your brokerage or prop firm accounts. LastPass simplifies your digital life by generating and storing complex, encrypted passwords for every site you use.

Try LastPass for Free Today!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- New Zealand Electronic Card Retail Sales & Spending for June 2026 at 10:45 pm GMT

- Japan Reuters Tankan Index for July 2026 at 11:00 pm GMT

- Japan Machinery Orders for May 2026 at 11:50 pm GMT

- China GDP Growth Rate, Retail Sales, Unemployment Rate, Industrial Production for June 30, 2026 at 2:00 am GMT

- China Monetary Developments for June 2026

- Euro area Industrial Production for May 2026 at 9:00 am GMT

- U.S. MBA 30-Year Mortgage Rate & Applications for July 10, 2026 at 11:00 am GMT

- Canada Manufacturing & Wholesale Sales Final for May 2026 at 12:30 pm GMT

- Canada New Motor Vehicle Sales for May 2026 at 12:30 pm GMT

- U.S. PPI Growth Rate for June 2026 at 12:30 pm GMT

- U.S. Fed Williams Speech at 12:45 pm GMT

-

Bank of Canada Interest Rate Decision for July 15, 2026 at 1:45 pm GMT

- BoC Press Conference at 2:30 pm GMT

- Fed Chair Warsh Testimony at 2:00 pm GMT

- EIA Crude Oil Stocks Change for July 10, 2026 at 2:30 pm GMT

Wednesday opens with China’s Q2 GDP release alongside the June activity dump, a test of whether the trade-data strength that surprised markets overnight carries through to the broader economy.

The U.S. session then brings June PPI ninety minutes ahead of the Bank of Canada rate decision, with the producer print especially worth watching after today’s soft CPI, since it either confirms or complicates the cooling-inflation read one day later.

Warsh returns to Capitol Hill for a second day of testimony, and after leaning against the dovish take on Tuesday, any further pushback could keep a floor under the dollar. The path of the U.S.-Iran conflict and the status of Hormuz remain the dominant wildcard, with firmer oil still capable of overriding the calendar at any point.

Stay frosty out there, forex friends!

When the June CPI came in softer than expected, the dollar collapsed within minutes. But when Fed Chair Warsh testified hours later, part of that move reversed. This two-part reaction isn’t random—it follows a specific, predictable pattern. Premium members can read our lesson:

📖 From Data to Price Action: What Happens When Big News Hits

Reading this helps you understand how data deviation from expectations drives the initial algorithmic spike, why secondary information (like central bank communication) modifies that move, and what determines how far each leg travels.

And if you’re not a Premium subscriber yet, consider joining. With Babypips Premium, you get full access to School of Pipsology lessons that help you understand how economic surprises trigger price action, and how central bank communication can reverse or modify those moves.