Markets opened the new quarter on a busy note Wednesday, with oil sliding on optimism around U.S.-Iran talks while Fed Chair Kevin Warsh told a central banking forum that inflation risks had come down, even as he reaffirmed the Fed’s commitment to price stability. Equities finished mixed as a slide in chipmakers offset gains elsewhere, bitcoin led the major assets higher, and the dollar closed with a modest bullish lean.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- U.S. API Crude Oil Stock Change for June 26, 2026: -6.07M (-0.77M previous)

- Australia S&P Global Manufacturing PMI Final for June 2026: 51.5 (51.2 forecast; 50.7 previous)

- Japan Tankan Large Manufacturers Index for Q2 2026: 22.0 (13.0 forecast; 17.0 previous)

- Japan S&P Global Manufacturing PMI Final for June 2026: 54.8 (54.9 forecast; 54.5 previous)

- Australia Building Permits Prel for May 2026: 5.3% y/y (9.5% y/y forecast; 10.2% y/y previous)

- China RatingDog Manufacturing PMI for June 2026: 51.7 (51.4 forecast; 51.8 previous)

- Japan Consumer Confidence for June 2026: 33.8 (32.0 forecast; 33.6 previous)

- U.K. Nationwide Housing Prices for June 2026: 2.2% y/y (2.2% y/y forecast; 1.7% y/y previous)

- Australia Commodity Prices for June 2026: 16.9% y/y (18.0% y/y forecast; 16.8% y/y previous)

- Swiss Retail Sales for May 2026: 3.5% y/y (1.3% y/y forecast; 1.6% y/y previous)

- Swiss procure.ch Manufacturing PMI for June 2026: 54.3 (56.5 forecast; 57.3 previous)

- Euro area S&P Global Manufacturing PMI Final for June 2026: 51.4 (51.3 forecast; 51.6 previous)

- U.K. S&P Global Manufacturing PMI Final for June 2026: 52.5 (53.1 forecast; 53.9 previous)

- Euro area CPI Growth Rate Flash for June 2026: 2.8% y/y (3.1% y/y forecast; 3.2% y/y previous)

- U.S. Challenger Job Cuts for June 2026: 45.85k (85.0k forecast; 97.01k previous)

- U.S. MBA 30-Year Mortgage Rate for June 26, 2026: 6.57% (6.59% previous)

- U.S. ADP National Employment Report for June 2026: 98.0k (105.0k forecast; 122.0k previous)

- U.S. ISM Manufacturing PMI for June 2026: 53.3 (53.6 forecast; 54.0 previous)

- U.S. Construction Spending Prel for May 2026: 0.1% m/m (0.5% m/m forecast; 0.4% m/m previous)

- Fed Chairman Warsh thinks that inflation risks are decreasing and reaffirmed the central bank’s independent commitment to achieving its 2% target. Also reiterated that the Fed will no longer provide “forward guidance” on interest rates, opting instead to chart a new policy course and launch task forces to evaluate its broader economic strategies.

- U.S. decided against renewing the U.S.-Mexico-Canada Agreement

Have a solid trading strategy but lack the capital? FundedNext empowers disciplined traders by providing simulated trading accounts up to $200K.

Unlike other prop firms, FundedNext imposes no artificial time limits on challenges. You even earn a unique 15% profit share during your evaluation! Once funded, you keep up to a 95% profit split with guaranteed 24-hour payouts. Trade CFDs or Futures your way—even during major news events.

Join over 400K traders who have received $300M+ in payouts. Ready to back your edge?

Learn More About FundedNext! Limited time offer: Use code BPFN for discounts on both CFD & Futures plans! T&C apply. T&C apply.Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

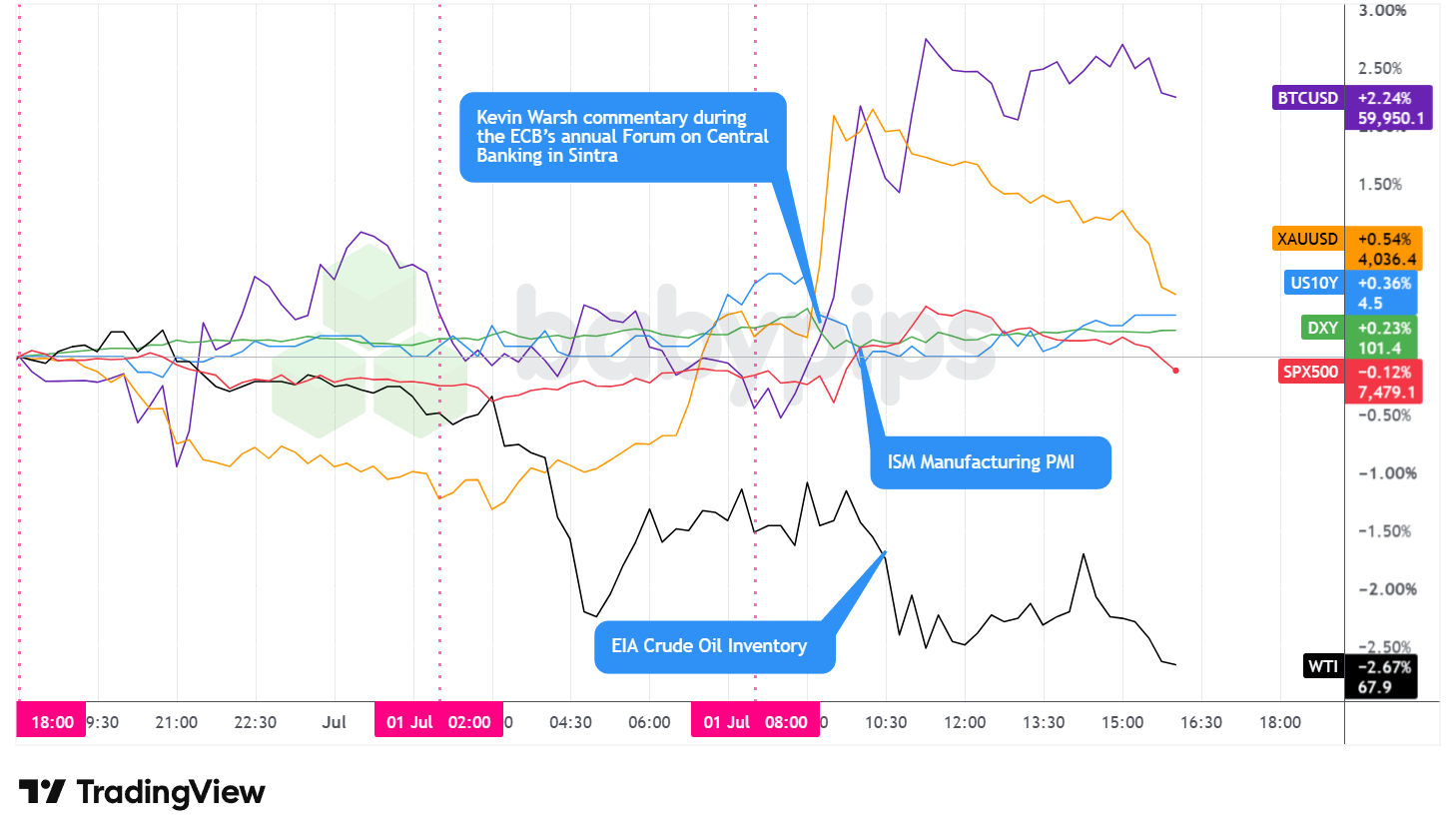

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Wednesday delivered a mixed session across the major asset classes, with easing input-cost pressures and softer oil sitting alongside a wobble in equities.

WTI crude oil was the session’s weakest performer, falling roughly 2.67% to trade around $67.90 per barrel. The decline built steadily from an overnight peak near $69.98, and the move appeared to correlate with growing optimism around U.S.-Iran talks and healthier flows through the Strait of Hormuz. A larger weekly draw in API crude inventories did little to arrest the slide, which points to sentiment on the geopolitical outlook rather than supply data as the dominant driver.

Gold added roughly 0.54% to trade around $4,036 per ounce. The metal pushed to an intraday high near $4,115 during the U.S. morning before easing back through the afternoon, giving up much of the earlier advance. The push higher likely reflected the central bank developments out of Sintra and the dollar weakness that followed them, before the metal drifted lower into the close.

Bitcoin was the standout to the upside, climbing about 2.24% to trade near $59,950. The move carried it to an intraday high around $60,475 late in the morning before it settled into a range through the afternoon. The rally likely lined up with the same central bank developments and softer dollar that lifted gold, with the timing of the surge tracking the Sintra headlines.

The S&P 500 finished little changed, slipping about 0.12% to around 7,479. The index swung through a wide range, spiking to an intraday high near 7,521 late in the morning before fading into the close. The path likely reflected the reaction to the ECB forum alongside a slide in chipmakers, which weighed on the tape even as most index members advanced and left the benchmark to waver around the flat line.

The 10-year Treasury yield firmed modestly, up around 0.36% on the day to trade near 4.44%. Yields climbed through the London morning before easing after the U.S. open in the wake of the Sintra commentary, then recovered into the close.

Promoted: How Do Professionals Trade Central Bank News?

You’ve seen the retail reaction to central bank commentary—now see the institutional one. Brent Donnelly’s “The Art of Currency Trading” (4.7 stars & 517 reviews on Amazon) bridges the gap between the news headlines you read and the execution on your screen. It’s a practical, “no-fluff” guide to how professional FX desks navigate the exact type of geopolitical volatility described in today’s report.

Learn more about “The Art of Currency Trading” at Amazon

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

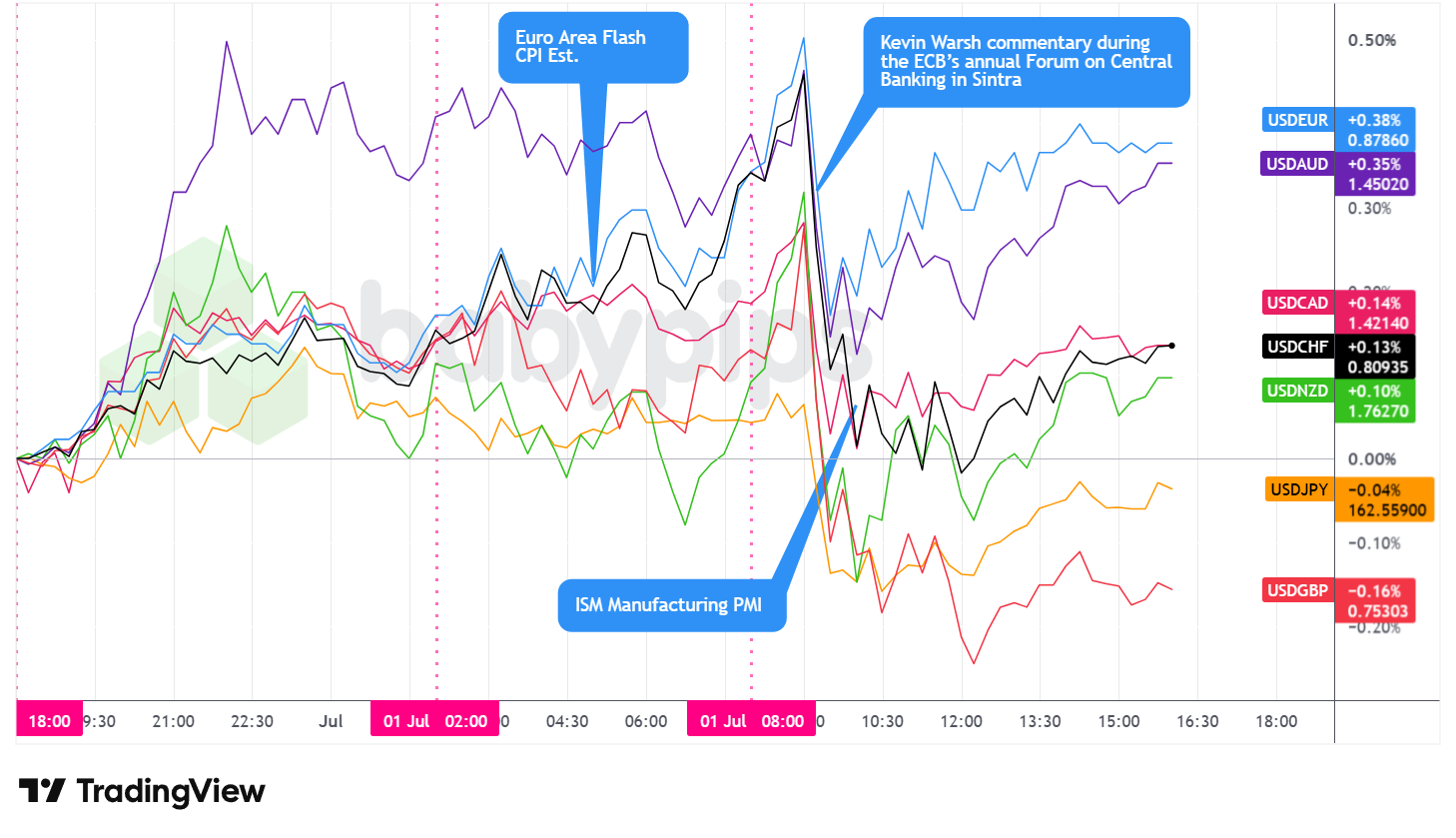

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar traded mixed on Wednesday, but spent most of the day and closed with a net bullish lean against the majors. It gained against the euro, Australian dollar, Canadian dollar, Swiss franc and New Zealand dollar, while slipping against the yen and the British pound.

During the Asian session, the dollar traded net higher against the majors until about mid-Asia morning, where it topped out and pulled back slightly heading into the London session. The yen stayed under pressure, extending its slide to a fresh 40-year low above 162 against the dollar even as Japan’s Tankan survey showed the strongest big-manufacturer sentiment since 2018.

During the London morning session, the dollar traded mixed and mostly sideways against the majors, though arguably with a net bullish bias, especially heading into the U.S. session. Euro area flash CPI cooled more than expected to 2.8%, which possibly left the single currency with little to lean on.

Not long after the U.S. session opened, the dollar fell against the majors, correlating with headlines from the ECB’s annual forum and comments from Fed Chair Warsh. His acknowledgment that inflation risks had come down read as a softer note than a firmly hawkish line, and it landed alongside an ISM manufacturing report whose prices-paid gauge posted its largest monthly drop since 2022, reinforcing a cooler near-term inflation picture. Short-dated Treasury yields fell to session lows after the remarks, which possibly dragged the dollar down with them. The reaction stayed two-sided, though.

Warsh paired the softer inflation read with a refusal to offer forward guidance and a repeated commitment to price stability, which left the rate path open and kept traders guessing on the timing of the next move. That mix of a less hawkish tone and greater uncertainty likely explains why the dollar and the broader markets chopped around the headlines before settling. The greenback stabilized ahead of the London close and rebounded slightly on net against the majors through the rest of the day.

At Wednesday’s close, the dollar traded mixed but arguably net bullish overall against the majors, with the softer tone concentrated against the yen and sterling.

Promoted: Keep Your Automated Edge Running 24/7.

Your algorithmic strategy shouldn’t rely on your home Wi-Fi. In high-volatility events, execution speed and uptime are what separate a winning backtest from a live market success. ForexVPS provides ultra-low latency, dedicated trading servers that keep your algos executing trades around the clock without interruption. Stop letting connectivity issues erode your edge.

Explore VPS plans at ForexVPS!

Disclosure: To help support our free daily content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- Australia Balance of Trade for May 2026 at 1:30 am GMT

- Swiss Financial Stability Report at 4:30 am GMT

- Swiss CPI Rate for June 2026 at 6:30 am GMT

- U.K. BoE Credit Conditions Survey at 8:30 am GMT

- Euro area Unemployment Rate for May 2026 at 9:00 am GMT

- U.S. Employment Situation Update for June 2026 at 12:30 pm GMT

- U.S. Initial Jobless Claims for June 27, 2026 at 12:30 pm GMT

- Canada S&P Global Manufacturing PMI for June 2026 at 1:30 pm GMT

- U.S. Factory Orders for May 2026 at 2:00 pm GMT

- Bank of England Mann Speech at 3:45 pm GMT

- U.S. Total Vehicle Sales for June 2026

Thursday’s calendar centers on the U.S. employment situation report, with consensus looking for around 115,000 jobs added in June and traders watching the unemployment rate for signs of a cooling labor market. A print in that neighborhood alongside a steady jobless rate would reinforce the picture of solid growth without adding much fuel to near-term rate-hike bets.

Ahead of that, Swiss CPI and the euro-area unemployment rate offer a read on European price and labor trends, while a speech from the Bank of England’s Catherine Mann may draw attention given the wider central bank focus on inflation risks and forward guidance this week.

Stay frosty out there, forex friends!

Fed Chair Warsh’s comments at the ECB forum shifted market expectations and moved bond yields, but how much of the nuance did you catch? Premium members can read our lesson:

📖 Hawkish vs. Dovish: How to Read Central Bank Language

Reading this helps you understand when central bank language is hawkish or dovish, how to identify where policymakers actually sit on the rate spectrum, and why a single speech often moves currencies more than the rate decision itself.

And if you’re not a Premium subscriber yet, consider joining.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand how to decode the hidden signals in central bank communication that reshape market expectations before any official rate move.