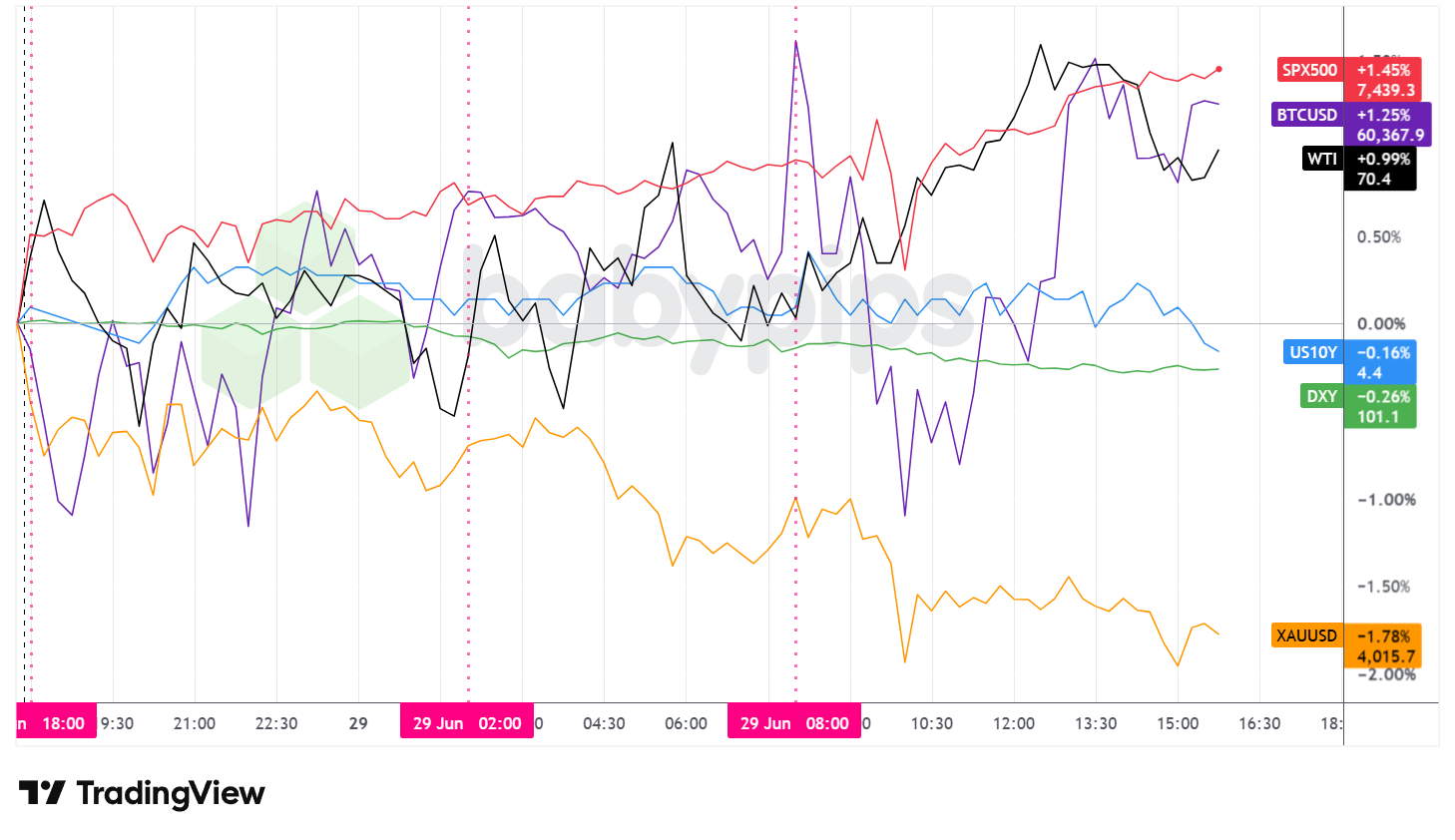

Technology shares led a broad equity rebound into the end of Q2, with the S&P 500 gaining roughly 1.45% as traders returned to risk assets following last week’s AI-sector selloff. Gold fell nearly 1.8% as the renewed U.S.-Iran ceasefire trimmed geopolitical risk premiums, while WTI crude gained roughly 1% with the truce capping the weekend’s initial oil bid. Month-end and half-year rebalancing likely kept intraday conditions choppy across most asset classes.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- The U.S. and Iran exchanged missile and drone strikes over the weekend before both sides agreed Sunday to halt hostilities and return to negotiations in Doha, beginning Tuesday, centered on the mechanics of Strait of Hormuz passage. Vessel transits through the strait fell to 48 over the June 26-28 period, down sharply from 70 on Wednesday before the latest round of exchanges. Analysts warned that tanker backlogs, damaged infrastructure and production shut-ins mean Persian Gulf oil supply could remain constrained well into the second half of the year even if the Doha talks hold.

- Japan Retail Sales for May 2026: 5.3% y/y (2.5% y/y forecast; 2.1% y/y previous); 1.9% m/m (0.7% m/m forecast; 1.3% m/m previous)

-

Euro area Monetary Developments for May 2026

- Euro area M3 Money Supply for May 2026: 3.2% (2.9% forecast; 2.7% previous)

- Euro area Loans to Companies for May 2026: 4.0% y/y (3.6% y/y forecast; 3.4% y/y previous)

- Euro area Loans to Households for May 2026: 3.1% y/y (3.0% y/y forecast; 3.0% y/y previous)

-

U.K. Monetary Developments for May 2026

- U.K. Mortgage Approvals for May 2026: 56.21k (65.4k forecast; 65.94k previous)

- U.K. M4 Money Supply for May 2026: 0.1% m/m (0.3% m/m forecast; 0.2% m/m previous)

- U.K. BoE Consumer Credit for May 2026: 1.66B (1.8B forecast; 1.86B previous)

- U.K. Net Lending to Individuals for May 2026: 4.6B m/m (6.1B m/m forecast; 6.2B m/m previous)

- Euro area Consumer Inflation Expectations for June 2026: 34.0 (42.0 forecast; 40.5 previous)

- Euro area Consumer Confidence for June 2026: -17.7 (-17.7 forecast; -19.0 previous)

- Euro area Economic Sentiment for June 2026: 95.0 (94.5 forecast; 93.5 previous)

- U.S. Dallas Fed Manufacturing Index for June 2026: 0.0 (2.0 forecast; 0.4 previous)

Promoted: Get the Capital You Need to Trade with Confidence.

Navigating unpredictable market swings requires discipline, strategy, and most importantly, adequate capital. Whether you’re trading major macroeconomic shifts or everyday price action, don’t let a lack of liquidity hold you back from capitalizing on prime opportunities.

Alpha Capital Group provides access to simulated funded accounts from $5K to $200K. Starting at just $40, you can execute high-conviction setups with the professional position sizing they deserve. Join 250K+ traders in 180+ countries today!

Learn more about Alpha Capital Group!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

The S&P 500 gained roughly 1.45%, closing near 7,439, capping what appeared set to be among the index’s strongest quarters in roughly six years. An intraday flush early in the U.S. session dragged the index to approximately 7,348 before a sustained recovery pushed it through the afternoon to session highs near 7,444. Technology shares drove the advance, with the Nasdaq 100 gaining at approximately twice the S&P’s pace.

WTI crude oil settled near $70.30, gaining approximately 0.99%. Prices dipped to roughly $69.15 near the Asian session lows before climbing through the European and U.S. sessions to a high near $70.91, then pulled back toward the close. An initial bid at Monday’s open may have reflected the weekend Iran-U.S. strikes, with gains likely contained once the fresh ceasefire and Doha talks were announced.

Gold fell roughly 1.78%, settling near $4,016. The decline ran through most of the session, holding near $4,040–$4,052 into the U.S. open before a sharper leg lower briefly approached $4,000. No clear gold-specific catalyst emerged, though the renewed ceasefire and easing of immediate geopolitical tension may have weighed on safe-haven positioning.

Bitcoin gained approximately 1.25%, settling near $60,368. The range was wide: a spike to roughly $60,714 around the U.S. open reversed quickly to near $58,867 before recovering, tracking the broader risk-on tone in equities through the afternoon.

The 10-year Treasury yield edged roughly 0.16% lower, settling near 4.36%, with the bond market trading broadly steady through the session.

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Most trading mistakes aren’t technical—they’re psychological. In the classic “Trading in the Zone” by Mark Douglas (⭐ 4.7★ | 10,000+ reviews on Amazon), you’ll learn how to master the probabilistic thinking and emotional discipline mentioned in today’s article. If you struggle with hesitation or breaking your rules, this is your manual for consistent execution.

Click on the link to learn more about “Trading in the Zone” by Mark Douglas!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

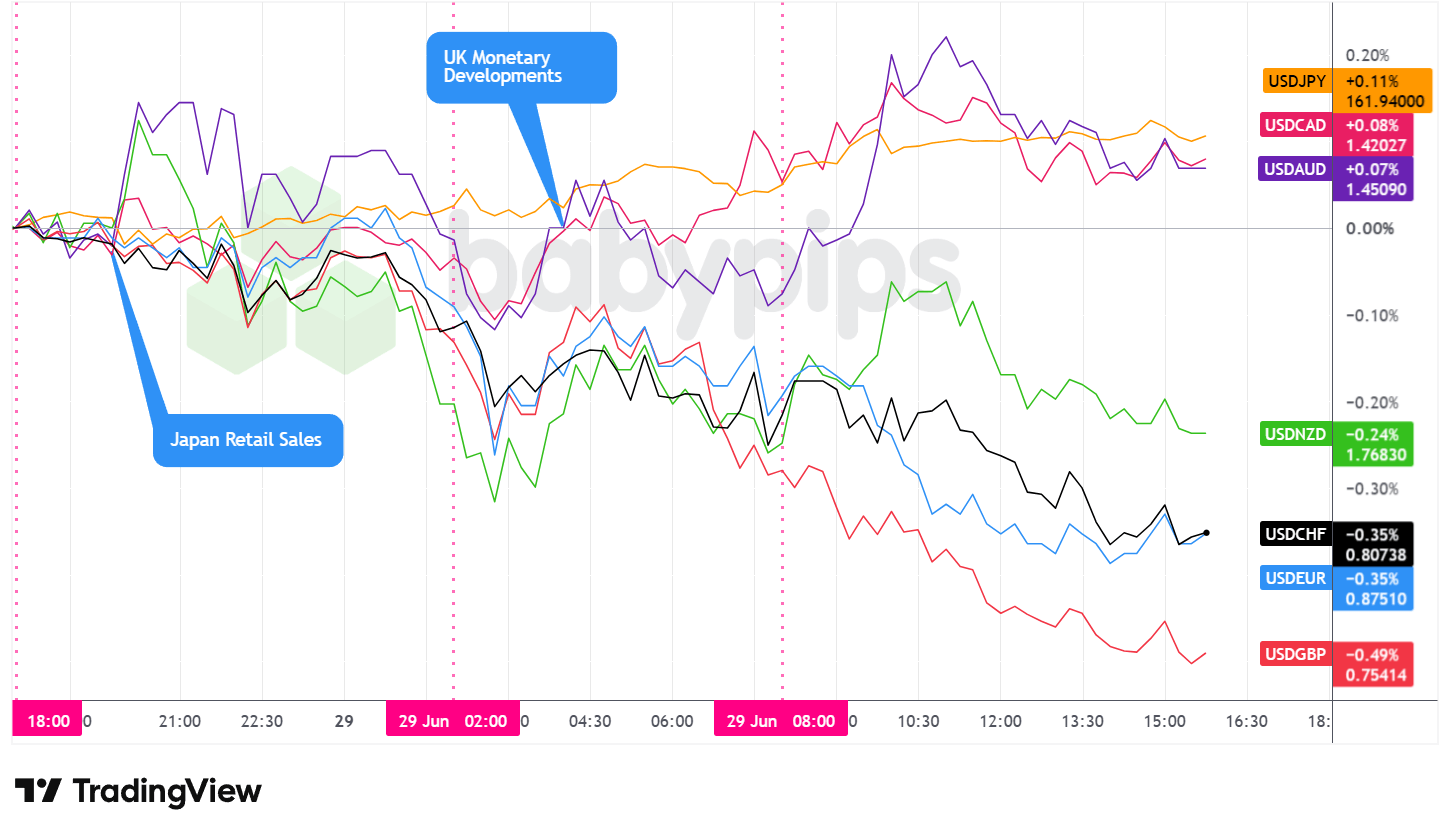

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar ended Monday with a net bearish lean against the majors, though the directional path shifted across all three sessions.

During the Asian session, the dollar traded net bearish, with losses deepening into the London open. Japan’s May retail sales surged to 5.3% year-on-year, the strongest print since November 2023, well above the 2.5% forecast. The initial yen strength faded through the session, and the dollar drifted to approximately 161.94 against the yen by the close, the yen’s weakest reading against the dollar since 1986.

After the London open, the dollar dipped briefly before stabilizing and rebounding. UK Monetary Developments data landed during the session: mortgage approvals for May came in at 56,210, well below the 65,400 forecast. Despite the weak UK housing print, sterling ended the day as the strongest performer against the dollar among the majors. Month-end and quarter-end positioning may offer one possible explanation for the divergence, though other market dynamics could have been at play.

ECB President Christine Lagarde, speaking at the ECB Forum on Central Banking in Sintra, described the June rate hike as a deliberate, evidence-based decision and said nothing observed since had called that assessment into question. She noted the ECB’s reaction function is now well understood by markets, allowing financial conditions to adjust before any formal policy decision. ECB Executive Board member Isabel Schnabel has separately argued borrowing costs likely still need to rise further. The euro held broadly firmer against the dollar through the European and U.S. sessions, though isolating the Sintra commentary as the driver, independent of broader USD softness and month-end flows, is difficult from price action alone.

Heading into the U.S. open, the dollar found buying interest. After the open it initially traded with a net bullish lean, then reversed course through the afternoon. By the close, the dollar’s losses against European currencies and NZD outweighed small gains against JPY, CAD, and AUD, leaving it with a net bearish lean on the day.

Promoted: Keep Your Automated Edge Running 24/7.

Your algorithmic strategy shouldn’t rely on your home Wi-Fi. In high-volatility events, execution speed and uptime are what separate a winning backtest from a live market success. ForexVPS provides ultra-low latency, dedicated trading servers that keep your algos executing trades around the clock without interruption. Stop letting connectivity issues erode your edge.

Explore VPS plans at ForexVPS!

Disclosure: To help support our free daily content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- U.K. BRC Shop Price Inflation for June 2026 at 11:01 pm GMT

- Japan Unemployment Rate for May 2026 at 11:30 pm GMT

- Japan Industrial Production Prel for May 2026 at 11:50 pm GMT

- New Zealand ANZ Business Confidence for June 2026 at 1:00 am GMT

- Australia RBA Meeting Minutes at 1:30 am GMT

- Australia Housing & Private Credit for May 2026 at 1:30 am GMT

- China PMI Updates for June 2026 at 1:30 am GMT

- Japan Housing Starts for May 2026 at 5:00 am GMT

- Germany Retail Sales for May 2026 at 6:00 am GMT

- U.K. Nationwide Housing Prices for June 2026 at 6:00 am GMT

- U.K. GDP Growth Rate Final for March 31, 2026 at 6:00 am GMT

- Swiss KOF Leading Indicators for June 2026 at 7:00 am GMT

- Germany Unemployment Change for June 2026 at 7:55 am GMT

- ECB Schnabel Speech at 9:40 am GMT

- BoE Breeden Speech at 10:40 am GMT

- Germany Inflation Rate Prel for June 2026 at 12:00 pm GMT

- Canada GDP Prel for May 2026 at 12:30 pm GMT

- U.S. S&P/Case-Shiller Home Price for April 2026 at 1:00 pm GMT

- ECB Lane Speech at 1:30 pm GMT

- U.S. Chicago PMI for June 2026 at 1:45 pm GMT

- U.S. JOLTs Job Openings & Quits for May 2026 at 2:00 pm GMT

- CB U.S. Consumer Confidence for June 2026 at 2:00 pm GMT

- U.S. Dallas Fed Services Index for June 2026 at 2:30 pm GMT

- Canada Budget Balance for April 2026 at 3:00 pm GMT

Tuesday packs a heavy slate into a holiday-shortened week as markets approach the U.S. Independence Day period. China’s June PMI updates at 1:30 am GMT offer an early read on whether economic momentum held through the month. Germany’s preliminary June CPI at noon GMT arrives as a live inflation data point for the ongoing Sintra discussions, particularly following Monday’s sharp undershoot in euro area consumer inflation expectations. UK GDP final data for Q1 at 6:00 am GMT and the BoE Breeden speech provide fresh context for UK rate expectations. U.S. JOLTS job openings and the Conference Board consumer confidence reading, both at 2:00 pm GMT, carry the most direct potential for USD volatility later in the North American session.

Stay frosty out there, forex friends!

After months of sector rotation and selloffs, traders returned to risk assets Monday with the S&P 500 rebounding hard. But currency traders need to understand what’s actually driving those moves across the forex complex and which pairs benefit most. Premium members can read our lesson:

📖 Equities and Currencies: The Big Picture

Reading this helps you understand how equity market performance shapes risk sentiment and drives currency flows, which major pairs strengthen when equities rally, and how to read FX action through the lens of broader asset class behavior.

And if you’re not a Premium subscriber yet, consider joining.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand how major market moves across stocks, bonds, and commodities ripple through the forex market and shape your currency pair performance.