Markets leaned risk-off on Wednesday as a fresh slide in chipmakers ahead of Micron Technology’s after-hours results weighed on equities, while easing Middle East tensions pulled oil back toward pre-conflict levels and dragged Treasury yields lower. The U.S. dollar firmed against every major counterpart and finished as the day’s strongest currency, and both gold and bitcoin extended their recent declines as traders held to expectations for further Federal Reserve rate hikes over the coming year.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- U.S. API Crude Oil Stock Change for June 19, 2026: -0.77M (-8.33M previous)

-

Australia CPI Growth Rate for May 2026: 4.0% y/y (4.4% y/y forecast; 4.2% y/y previous)

- Australia RBA Trimmed Mean CPI for May 2026: 3.6% y/y (3.5% y/y forecast; 3.4% y/y previous)

- Australia RBA Weighted Median CPI for May 2026: 3.6% y/y (3.6% y/y forecast; 3.5% y/y previous)

- Swiss Economic Sentiment Index for June 2026: -25.0 (1.5 forecast; -11.1 previous)

- Germany Ifo Business Climate for June 2026: 85.6 (85.5 forecast; 84.9 previous)

- U.S. MBA 30-Year Mortgage Rate for June 19, 2026: 6.59% (6.6% previous)

- U.S. MBA Mortgage Applications for June 19, 2026: 1.0% (-3.8% previous)

- Canada Manufacturing Sales Prel for May 2026: 1.1% m/m (-1.3% m/m forecast; 4.2% m/m previous)

- U.S. Current Account for Q1 2026: -226.8B (-220.0B forecast; -190.7B previous)

- U.S. Building Permits Final for May 2026: -0.9% m/m (-0.7% m/m forecast; 4.4% m/m previous)

- Swiss SNB Quarterly Bulletin: medium-term inflation pressure is still broadly unchanged, and the Bank is more willing to intervene in FX markets if needed. It also notes solid Swiss growth in Q2, but slower global momentum and higher oil-related import costs are likely to keep near-term inflation elevated while weighing on growth, with GDP still expected to rise about 1% in 2026 and 1.5% in 2027.

- U.S. New Home Sales for May 2026: -7.3% m/m (2.9% m/m forecast; -6.2% m/m previous)

Promotion: Lux Trading Firm funds with real capital (up to $10M in buying power), refunds 1-step evaluation fees 100% after Stage 1. Highly competitive Instant funding plans & prediction market plans are available. Get a certified track record, and a potential salary for long-term focused, highly qualified performers.

Learn More at Lux Trading Firm

Disclosure: To help support our free daily content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

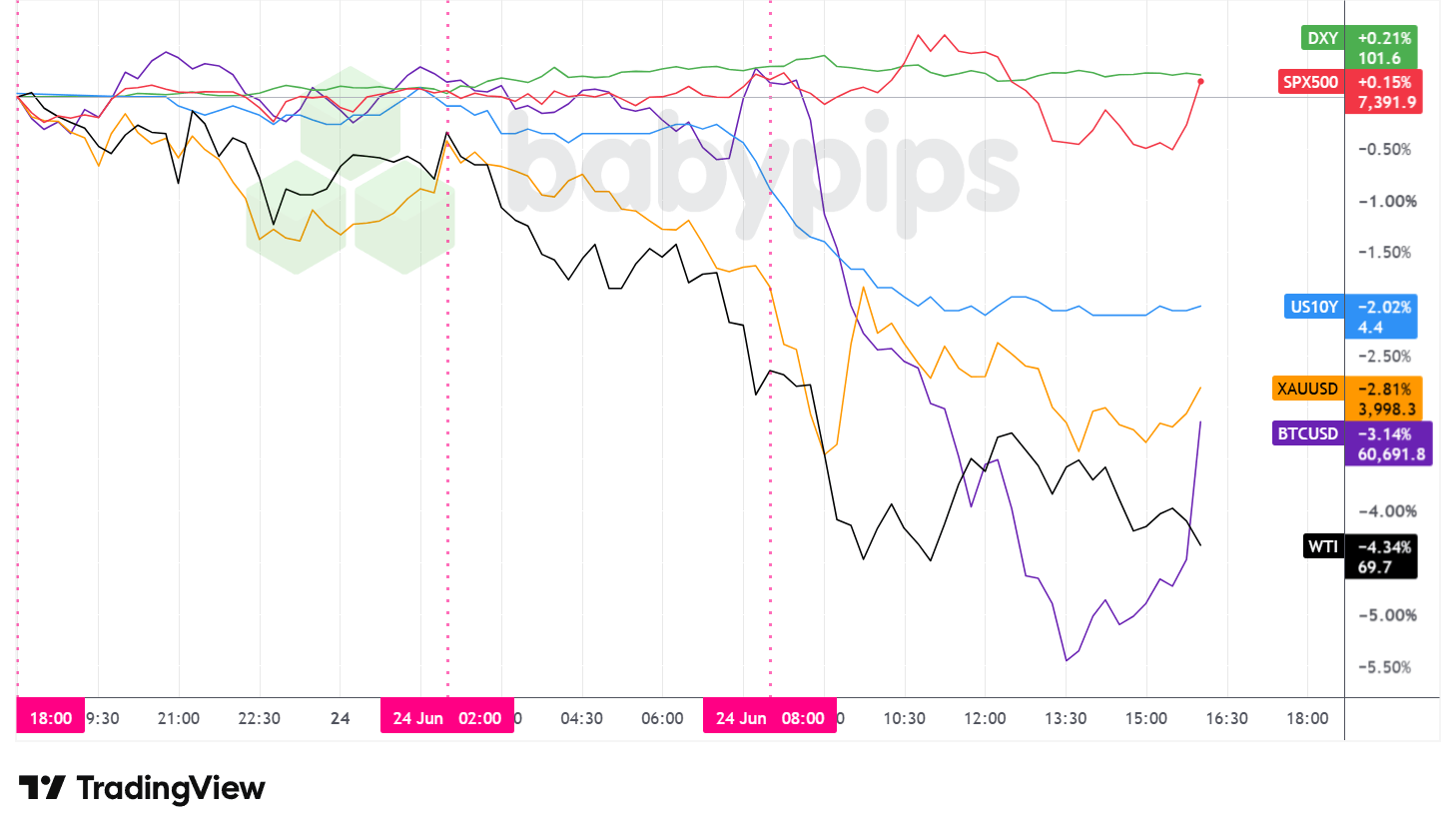

Broad Market Price Action:

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

WTI crude posted one of the session’s steepest declines, sliding roughly 3.8% to around $69.90 per barrel and dipping below the $70 mark intraday. The move extended a multi-day retreat as progress in regional peace talks and signs of normalizing traffic through the Strait of Hormuz continued to unwind the war-driven premium that had built up earlier in the month.

The S&P 500 eased around 0.3% to close near 7,350 after pushing above 7,420 in late morning and then fading. A renewed pullback in chipmakers ahead of Micron Technology’s results, due after the closing bell, weighed on the index even as the majority of its components advanced. Micron itself fell about 2.5%. Strategists at JPMorgan struck a more constructive tone, lifting their year-end S&P 500 target to 7,800 and pointing to solid earnings and the prospect of a peace deal to end the Iran conflict.

Gold extended its slide, falling roughly 3% to trade near $3,987 per ounce, with the metal probing levels just under $3,960 at its intraday low before steadying. The weakness appeared to track the prevailing rate narrative, as markets continued to price two to three Federal Reserve rate hikes over the next year following last week’s hawkish signals from Fed Chair Kevin Warsh. Softer oil prices, by easing some of the near-term inflation impulse, may also have trimmed demand for the inflation hedge.

Bitcoin was the day’s weakest major asset, dropping roughly 4.2% to around $59,800 after sliding from above $62,800 once the U.S. morning got underway. It carved out an intraday low near $59,000 in the early afternoon before recovering into the close. With no clear crypto-specific catalyst on the wires, the decline possibly reflected the broader risk-off tone running through speculative assets this week.

The U.S. 10-year Treasury yield declined, falling roughly 9 basis points to around 4.40%, with the sharpest leg lower unfolding through the U.S. morning. The drop appeared to correlate with the retreat in oil prices, which eased some of the market’s near-term inflation concerns ahead of Thursday’s PCE report, the Fed’s preferred inflation gauge.

Promoted: Profitable Trading Isn’t Reserved for Wall Street.

Most traders quietly wonder if consistent profitability is actually achievable for someone like them—or if it’s just a story people tell. Jack Schwager’s newest book, “Market Wizards: The Next Generation,” answers that question directly. The legendary author behind the original Market Wizards series interviews a new generation of successful traders—many self-taught—who built real wealth and income through the markets. Their common thread isn’t genius or insider access. It’s a deliberate process, disciplined risk management, and the conviction to take trading seriously as a pursuit worth mastering.

If that sounds like something worth exploring, this is a good place to start.

Get Market Wizards: The Next Generation on Amazon!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

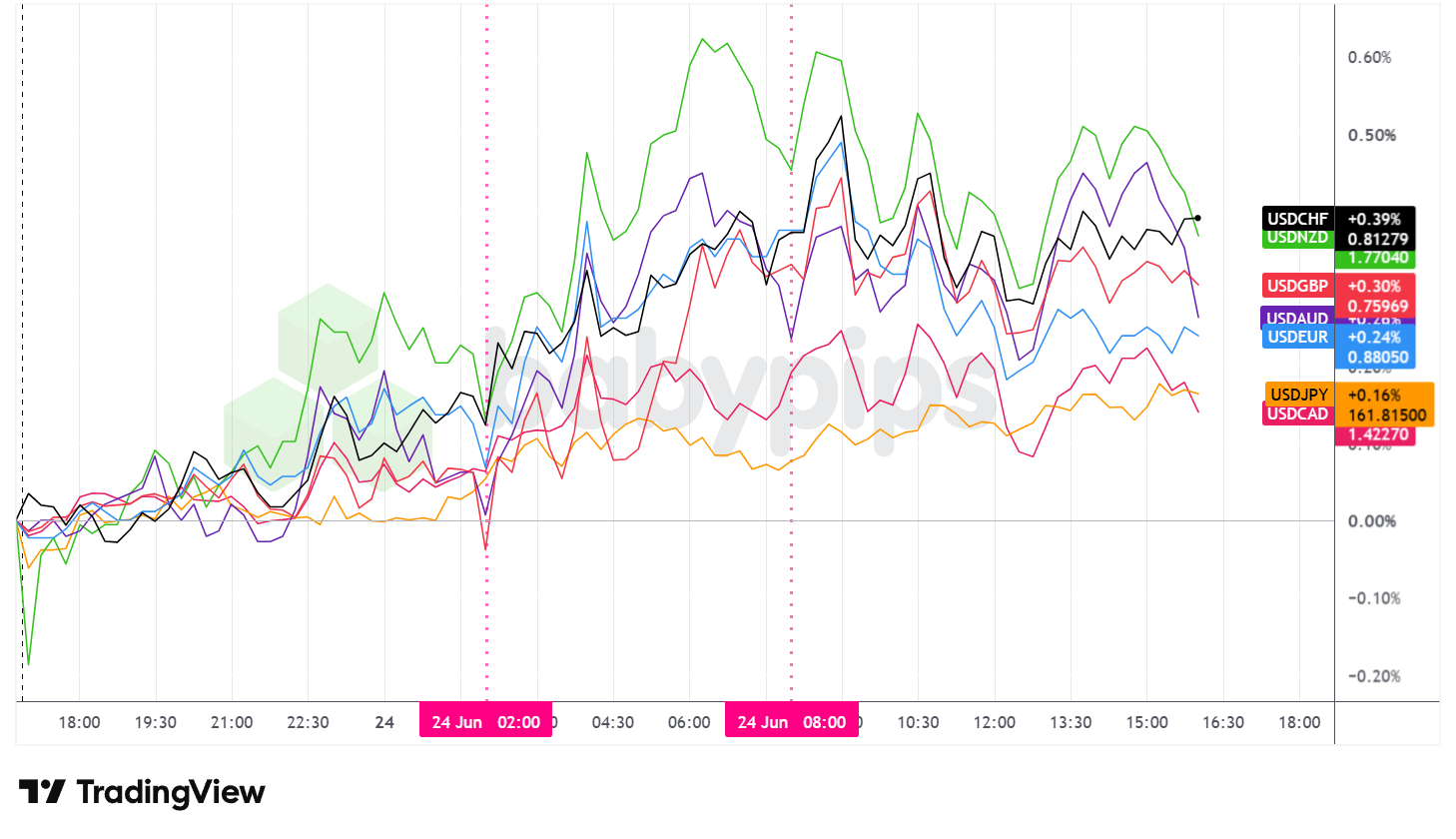

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar firmed against all of its major counterparts on Wednesday and finished as the strongest major currency on the day. The Dollar Index held a modest gain, settling around 101.6 after an intraday push toward 101.80.

From the Wednesday Asia open through to just after the U.S. session got underway, the dollar traded with a net higher bias against the majors. The Australian and New Zealand dollars sat among the weakest performers, with the Aussie pinned near multi-week lows and the kiwi close to a seven-month trough. Australia’s May CPI delivered a split message, as headline inflation slowed to 4.0% year-on-year and undershot forecasts while the RBA’s trimmed mean core measure accelerated to 3.6%, leaving the central bank’s policy path unresolved. RBA Deputy Governor Hauser said there is still work to do to bring inflation down, describing it as far too high.

In Japan, the Bank of Japan’s June Summary of Opinions revealed a board leaning further toward normalization, with some members floating the case for hikes every few months to reach a neutral rate. BOJ Governor Kazuo Ueda reiterated that he expects additional rate increases as underlying inflation picks up. Even so, the yen held near multi-decade lows and registered the smallest dollar gain among the majors, which suggests the hawkish signals did little to reverse its broader weakness.

Through the London session the dollar built on its advance, reaching its intraday peak around the European morning. Germany’s Ifo business climate index improved for a second month, edging up to 85.6, though the firmer read drew limited currency reaction. Swiss sentiment moved the other way, with the economic sentiment index tumbling to -25.0 from -11.1.

After the U.S. session opened, the dollar pulled back slightly from its highs and then stabilized, holding the bulk of its gains through the rest of the day. The greenback’s resilience came alongside the broader risk-off tone, with softer equities, lower oil, and steady Fed hike expectations all possibly lending it underlying support.

By the Wednesday close, the dollar held net gains against every major currency, with its firmest performance against the New Zealand dollar and Swiss franc and its most muted against the yen and Canadian dollar.

Promoted: Keep Your Automated Edge Running 24/7.

Your algorithmic strategy shouldn’t rely on your home Wi-Fi. In high-volatility events, execution speed and uptime are what separate a winning backtest from a live market success. ForexVPS provides ultra-low latency, dedicated trading servers that keep your algos executing trades around the clock without interruption. Stop letting connectivity issues erode your edge.

Explore VPS plans at ForexVPS!

Disclosure: To help support our free daily content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- U.K. Car Production for May 2026 at 11:01 pm GMT

- Australia Employment Situation Update for May 2026 at 1:30 am GMT

- Australia Household Spending for May 2026 at 1:30 am GMT

- Japan Leading Indicators Index for April 2026 at 5:00 am GMT

- Germany GfK Consumer Confidence for July 2026 at 6:00 am GMT

- France Consumer Confidence for June 2026 at 6:45 am GMT

- ECB Lane Speech at 10:00 am GMT

- U.K. CBI Distributive Trades for June 2026 at 10:00 am GMT

- Canada Average Weekly Earnings for April 2026 at 12:30 pm GMT

- U.S. Initial Jobless Claims for June 20, 2026 at 12:30 pm GMT

- Chicago Fed National Activity Index for May 2026 at 12:30 pm GMT

- U.S. Durable Goods Orders for May 2026 at 12:30 pm GMT

- U.S. Core PCE Price Index for May 2026 at 12:30 pm GMT

- U.S. Personal Income & Spending for May 2026 at 12:30 pm GMT

- U.S. Kansas Fed Manufacturing Index for June 2026 at 3:00 pm GMT

- U.S. Fed Williams Speech at 7:40 pm GMT

- U.S. Fed Goolsbee Speech at 10:30 pm GMT

Thursday’s session centers on the U.S. Core PCE Price Index, the Federal Reserve’s preferred inflation measure, which forecasters expect to show acceleration on both a monthly and annual basis in May. With markets already leaning toward additional tightening, a hotter reading could harden those expectations. The release arrives alongside durable goods orders, personal income and spending, and the weekly jobless claims print, while remarks from Fed officials Williams and Goolsbee later in the day may add color on the policy outlook. ECB’s Lane is also due to speak during the European morning.

Stay frosty out there, forex friends!

Wednesday’s broad market slide shows why reading just the currency chart leaves you blind to half the story: while oil retreated on geopolitical relief and the dollar firmed on Fed rate expectations, gold slid and bitcoin crashed as traders rotated into a risk-off mood. Premium members can read our lesson:

📖 What Is Intermarket Analysis?

Reading this helps you understand how currencies connect to stocks, bonds, commodities, and each other, why watching multiple asset classes together gives you a more complete read on market direction, and how to spot cross-asset themes before they hit your chart.

And if you’re not a Premium subscriber yet, this is exactly the type of multi-asset context that separates traders who see the full picture from those who get blindsided.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand how to read the dollar, commodity markets, and bond market as one interconnected system instead of isolated pieces.