Wednesday’s session was shaped by the most significant direct military exchange between the United States and Iran since the conflict began earlier this year, with President Trump threatening further strikes on Tehran and accusing the country of prolonging peace negotiations. Crude oil advanced on supply disruption concerns while the S&P 500 extended its recent slide toward multi-week lows, pressured by a deepening tech-led selloff and geopolitical unease. In an unusual twist for a session characterized by risk-off sentiment, gold posted a steep decline despite the escalating conflict backdrop.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Australia Building Permits Final for April 2026: -3.4% m/m (-3.4% m/m forecast; -10.5% m/m previous)

- Australia Private House Approvals Final for April 2026: -1.0% m/m (-1.0% m/m forecast; 0.9% m/m previous)

- China CPI Growth Rate for May 2026: 1.2% y/y (1.4% y/y forecast; 1.2% y/y previous)

- China PPI for May 2026: 3.9% y/y (3.8% y/y forecast; 2.8% y/y previous)

- U.S. MBA 30-Year Mortgage Rate for June 5, 2026: 6.6% (6.57% previous)

- U.S. MBA Mortgage Applications for June 5, 2026: 10.8% (-2.5% previous)

-

U.S. CPI Growth Rate for May 2026: 4.2% y/y (4.0% y/y forecast; 3.8% y/y previous)

- U.S. Core Inflation Rate for May 2026: 2.9% y/y (2.9% y/y forecast; 2.8% y/y previous)

- Bank of Canada Interest Rate Decision for June 10, 2026: 2.25% (2.25% forecast; 2.25% previous)

- U.S. EIA Crude Oil Stocks Change for June 5, 2026: -7.23M (-7.97M previous)

- On Wednesday, US President Trump vowed to strike Iran after saying the country has been delaying talks on a peace deal

Promoted: Scale Your Forex Strategies

As persistent inflation and shifting central bank policies whipsaw traders, navigating the current macro landscape requires more than just a good entry—it requires a partner that has seen it all before.While new firms come and go with the volatility, The5ers (4.7★ rating on 32K+ reviews) has spent the last 10 years perfecting a funding model that works for the trader. It’s why over 1.6 million traders worldwide trust them to provide the capital and scaling needed to turn market analysis into meaningful professional growth.

Learn more about The5ers & available discountsDisclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

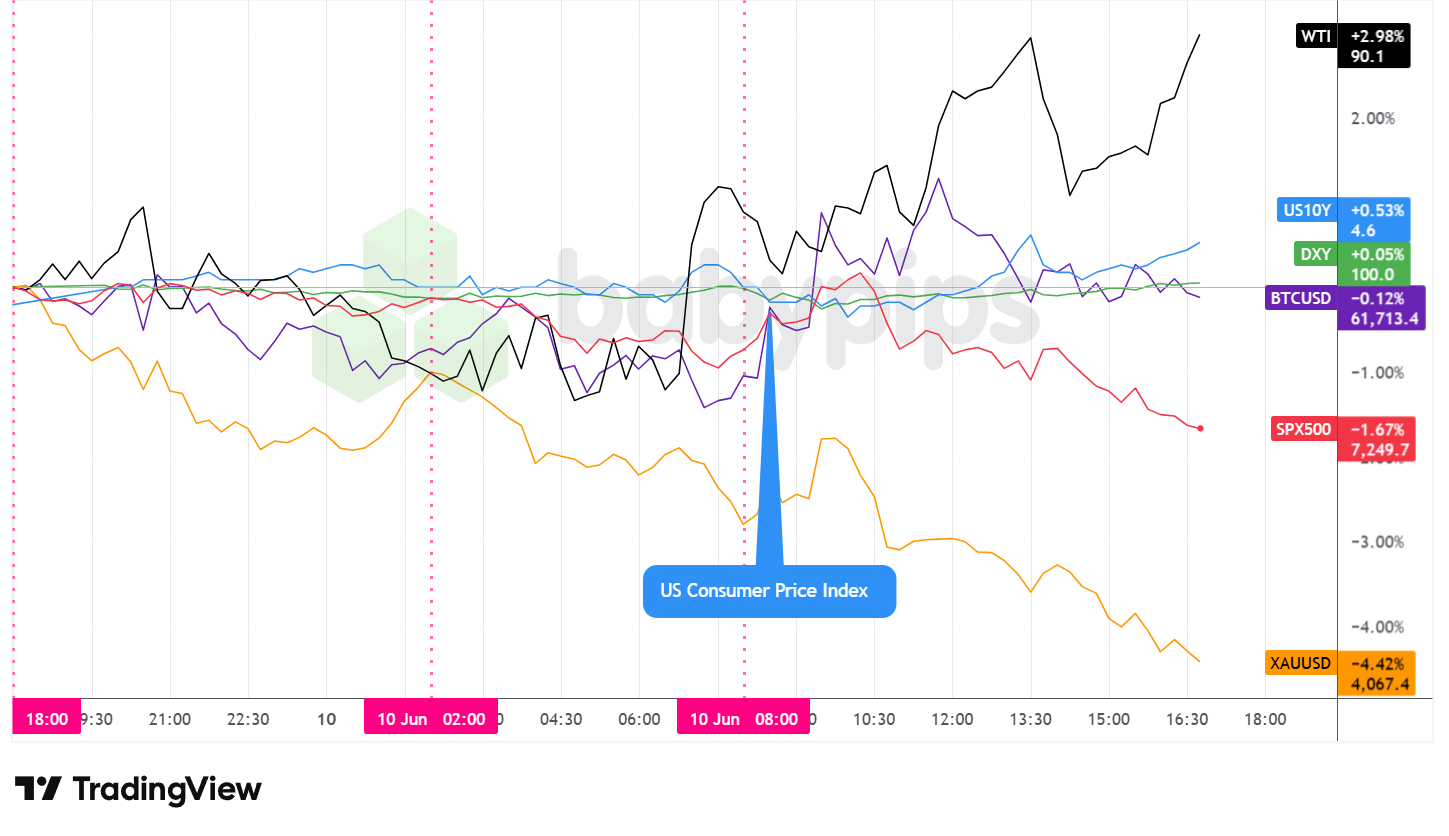

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Wednesday delivered a session of sharp and unusual asset divergence. Crude oil advanced steadily as geopolitical risk and another significant US inventory drawdown reinforced supply concerns, while equities declined under the weight of geopolitical unease and intensifying tech-sector selling pressure. Most striking was gold’s steep decline, which unfolded despite the escalating US-Iran conflict likely sparking safe haven flows and represented one of the metal’s largest single-session drops in recent months.

WTI crude oil was the session’s clear outperformer, closing approximately 1.5% higher near $89 per barrel. Prices climbed progressively through the session, appearing to track Trump’s increasingly pointed warnings of imminent additional strikes against Iran and growing concerns about Strait of Hormuz supply disruptions. Further support likely came from the EIA’s confirmation that US crude inventories fell by approximately 7.23 million barrels for the week ending June 5, extending what appears to be a protracted streak of consecutive weekly inventory declines.

The S&P 500 declined approximately 1.5% on the session, sliding toward multi-week lows. While Trump’s midday remarks about renewed strikes on Iran appeared to accelerate selling, the pressure was more broadly driven by a tech-led unwind that had been building throughout the week. Semiconductor stocks and AI-adjacent megacaps drew renewed scrutiny over valuations and the sustainability of AI infrastructure spending. Market chatter also suggests that profit-taking in high-flying AI-sector positions was likely necessary to keep risk within manageable parameters following an extended run, and noted that the approaching wave of new equity issuance, including the SpaceX IPO scheduled for this week, may be prompting institutional and retail investors to raise cash in anticipation.

Gold posted the session’s most striking and arguably puzzling move, declining approximately 4% to trade in the vicinity of $4,080. The precious metal was already drifting lower from elevated overnight levels before the US session opened, and selling accelerated steadily through the afternoon. With geopolitical escalation providing a traditionally supportive backdrop for safe-haven assets, the depth of the decline warrants careful interpretation. One possible explanation is that the above-consensus headline CPI print, at 4.2% year-over-year versus the 4.0% forecast, reinforced expectations of a higher-for-longer rate environment, weighing on the non-yielding metal as real yield expectations shifted higher. The core monthly reading of 0.2% month-over-month, which came in slightly below the 0.3% forecast, added ambiguity to the inflation picture rather than providing clear directional guidance for the gold market. It is also worth noting that gold had been trading near historically elevated levels in recent months, and position liquidation or profit-taking may have amplified the move.

The US 10-year Treasury yield rose modestly, trading near approximately 4.5% by the afternoon. Yields climbed around the US session open in a move that appeared to correlate with the hotter-than-expected headline CPI release, as the bond market priced in a somewhat more cautious Fed outlook.

Bitcoin was approximately flat on the session, trading near $61,700, holding up notably better than equities and remaining broadly disconnected from the day’s geopolitical and inflation-driven risk-off dynamics.

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Today’s wild intraday swings in oil and the rapid recovery in equities prove just how fast a geopolitical headline can flip the market. When price action reverses on a dime due to sudden comments from leaders, knowing the fundamentals isn’t enough—you need the psychological discipline to stick to your plan without panicking.

In “Unknown Market Wizards,” (⭐ 4.6★ | 1,400+ reviews on Amazon) Jack Schwager interviews under-the-radar trading pros to reveal what truly separates them from the pack: unbreakable mental resilience and rigid risk control. Learn how top traders stay clinical, manage their exposure, and execute flawlessly when the rest of the market is swept up in the emotion of geopolitical chaos.

Master Your Trading Mindset with Market Wizards!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

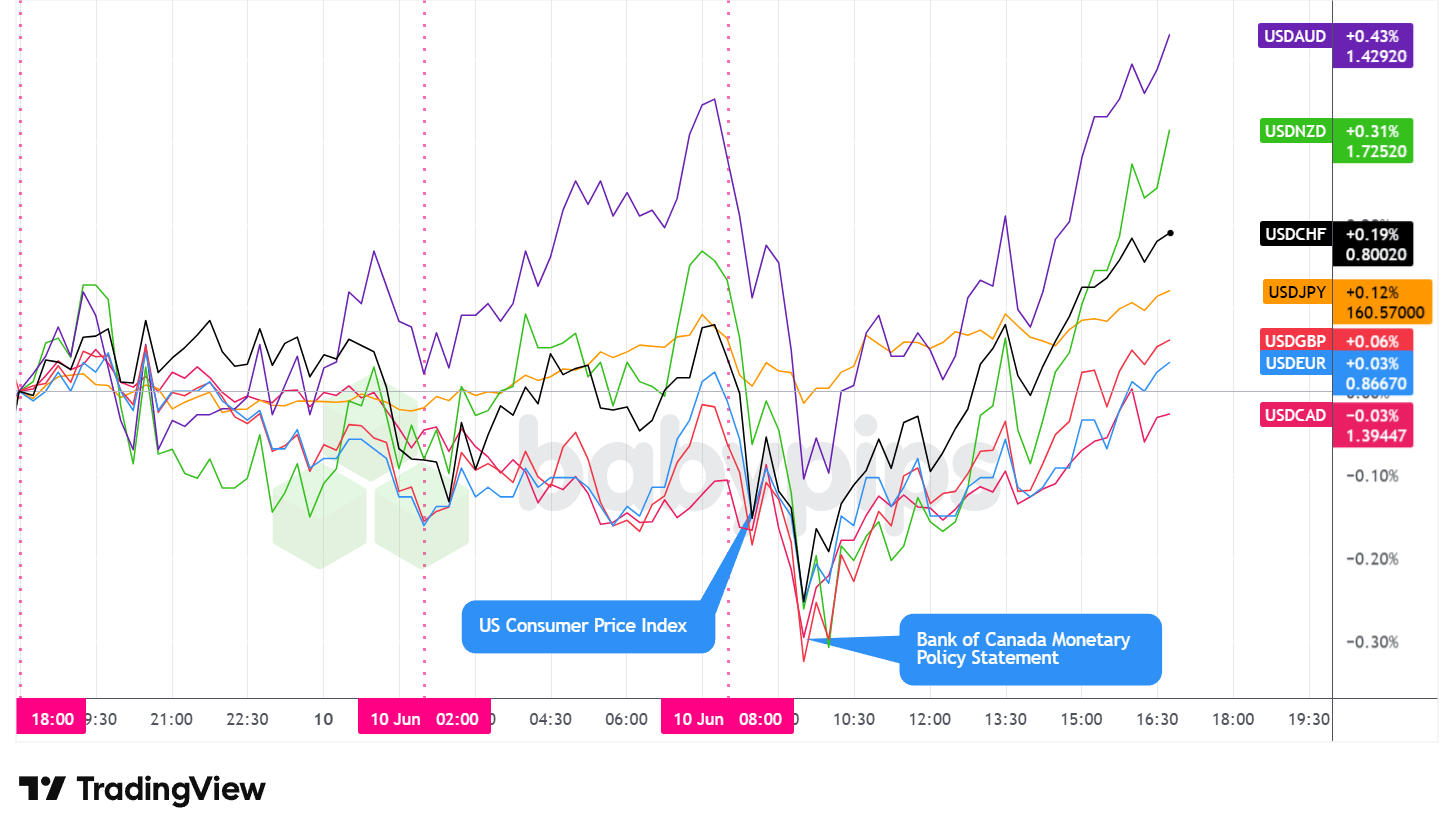

Overlay of USD vs. Majors – Chart Faster With TradingView

The US dollar traded with a mixed but arguably net positive lean on Wednesday. The US Dollar Index (DXY) ended the session near 100, essentially unchanged on the day, though the intraday path involved meaningful swings as successive geopolitical developments and the CPI release shifted short-term positioning.

During the Asian session, the dollar traded with an arguably neutral bias against major currencies. China’s May CPI came in at 1.2% year-over-year, below the 1.4% consensus, while factory-gate prices accelerated to 3.9% year-over-year, a divergence pointing to industrial-sector margin compression without generating a decisive directional FX response. Australia’s building permit data came in broadly in line with forecasts, providing limited impetus for the Australian dollar.

During the London session, the dollar gradually shifted to a net bullish lean, particularly as the session approached the US open. Escalating geopolitical news flow around Trump’s renewed Iran rhetoric and reports of continued overnight military exchanges may have contributed to mild safe-haven flows toward the greenback, consistent with a broader risk-off shift in equity futures that were under meaningful pressure ahead of the New York open. The euro and sterling were comparatively resilient during this period, with no major European economic releases providing a decisive catalyst in either direction.

In the US session, the dollar initially encountered some selling pressure around the time of the CPI release, possibly reflecting a market reaction to the core monthly reading of 0.2% month-over-month, which came in slightly below the 0.3% forecast and offered some initial relief to rate-sensitive positioning. However, the dollar found a floor around the US equity market open and rebounded through the remainder of the session. Trump’s explicit pledges to strike Iran “very hard” appeared to compound the risk-off tone and supported the greenback against risk-sensitive and commodity-linked currencies. The Bank of Canada’s decision to hold rates at 2.25%, as widely anticipated, produced minimal reaction in the Canadian dollar pair, which closed near flat. Separately, news that BOJ Governor Kazuo Ueda had been hospitalized and was expected to miss next week’s policy meeting may have contributed to modest yen underperformance relative to other major currencies, as it introduces some uncertainty around BoJ communications at the upcoming meeting. At the Wednesday close, the dollar posted its most notable gains against the Australian and New Zealand dollars, consistent with risk-off pressure on commodity-linked currencies, while performance against the euro and sterling was essentially flat on the day.

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Today’s daily recap highlights a market driven geopolitical developments and shifts in Fed policy expectations. But as any pro will tell you, understanding market drivers can aren’t enough if the trader lacks the discipline to execute a solid plan on it.

In “Unknown Market Wizards,” (⭐ 4.6★ | 1,400+ reviews on Amazon) Jack Schwager interviews successful traders to reveal a common truth: their edge isn’t just knowledge or skills—it’s their psychological resilience and rigid risk control. Whether you’re navigating shifting geopolitical themes or top tier economic data, learn how the “wizards” stay clinical and execute when the rest of the market is emotional.

Master Your Trading Mindset with Market Wizards!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- U.S. Monthly Budget Statement for May 2026 at 6:00 pm GMT

- U.K. RICS House Price Balance for May 2026 at 11:01 pm GMT

- Japan BSI Large Manufacturing for June 30, 2026 at 11:50 pm GMT

- Australia Consumer Inflation Expectations for June 2026 at 1:00 am GMT

- European Central Bank Interest Rate Decision for June 11, 2026 at 12:15 pm GMT

- Canada Building Permits for April 2026 at 12:30 pm GMT

- Germany Current Account for April 2026 at 12:30 pm GMT

- U.S. PPI for May 2026 at 12:30 pm GMT

- U.S. Initial Jobless Claims for June 6, 2026 at 12:30 pm GMT

- Euro area ECB Press Conference at 12:45 pm GMT

- U.S. Fed Balance Sheet for June 10, 2026 at 8:30 pm GMT

Thursday’s session is headlined by the European Central Bank’s rate decision at 12:15 pm GMT and subsequent press conference at 12:45 pm GMT. The ECB outcome will be watched closely for signals on the pace of future policy easing, particularly in the context of persistently elevated global energy prices and the potential inflationary pass-through from ongoing Strait of Hormuz disruptions.

The simultaneous US data slate at 12:30 pm GMT adds further volatility potential. The producer price index reading arrives one day after the hotter-than-expected headline CPI and will be especially relevant for gauging where the inflation pipeline stands heading into the summer. Initial jobless claims will be monitored for any signs of labor market deterioration that could complicate the Fed’s calculus as it weighs competing risks between cooling growth and sticky inflation.

Stay frosty out there, forex friends!