Tuesday’s session opened with a cautious risk-on tone following Monday’s Israel-Iran ceasefire agreement, only to reverse sharply in the afternoon after President Trump blamed Iran for shooting down a U.S. military helicopter over the Strait of Hormuz and declared the U.S. must respond, reigniting escalation fears across markets. A concurrent wave of selling in high-valuation technology and semiconductor stocks compounded the pressure, as investors grew increasingly skeptical about whether AI-era valuations could hold heading into a wave of high-profile new equity issuances.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- New Zealand Manufacturing Sales for Q1 2026: 2.8% y/y (-0.8% y/y forecast; -0.7% y/y previous)

- U.K. BRC Retail Sales Monitor for May 2026: 3.4% y/y (-3.0% y/y forecast; -3.4% y/y previous)

- Australia Westpac Consumer Confidence Change for June 2026: -2.9% (-1.2% forecast; 3.5% previous)

- Australia NAB Business Confidence for May 2026: -14.0 (-22.0 forecast; -24.0 previous)

- China Balance of Trade for May 2026: 105.43B (89.0B forecast; 84.82B previous)

- Germany Balance of Trade for April 2026: 14.5B (13.6B forecast; 14.3B previous)

- U.S. NFIB Business Optimism Index for May 2026: 95.3 (95.7 forecast; 95.9 previous)

- U.S. ADP Employment Change Weekly for May 23, 2026: 29.0k (35.75k previous)

- Canada Balance of Trade for April 2026: 2.72B (1.5B forecast; 1.78B previous)

- U.S. Balance of Trade for April 2026: -55.9B (-57.9B forecast; -60.3B previous)

- U.S. Existing Home Sales for May 2026: 3.2% m/m (0.5% m/m forecast; 0.2% m/m previous)

- U.S. Wholesale Inventories for April 2026: 0.6% m/m (0.5% m/m forecast; 1.3% m/m previous)

- President Trump said on Tuesday that Iran shot down an American military helicopter off Oman and that the US must respond

Promotion: If your confidence has grown in your market awareness & strategies, and you wanna take action, Maven Trading can help. They provide simulated funding challenges starting as low as $15, allowing you to trade major pairs with professional-sized capital. No time limits mean you can take swing plays on these market themes without the pressure of a ticking clock.

Learn More About Maven Trading Today! And for a limited time: Use code “ETERNAL” for 10% off Challenge fee!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

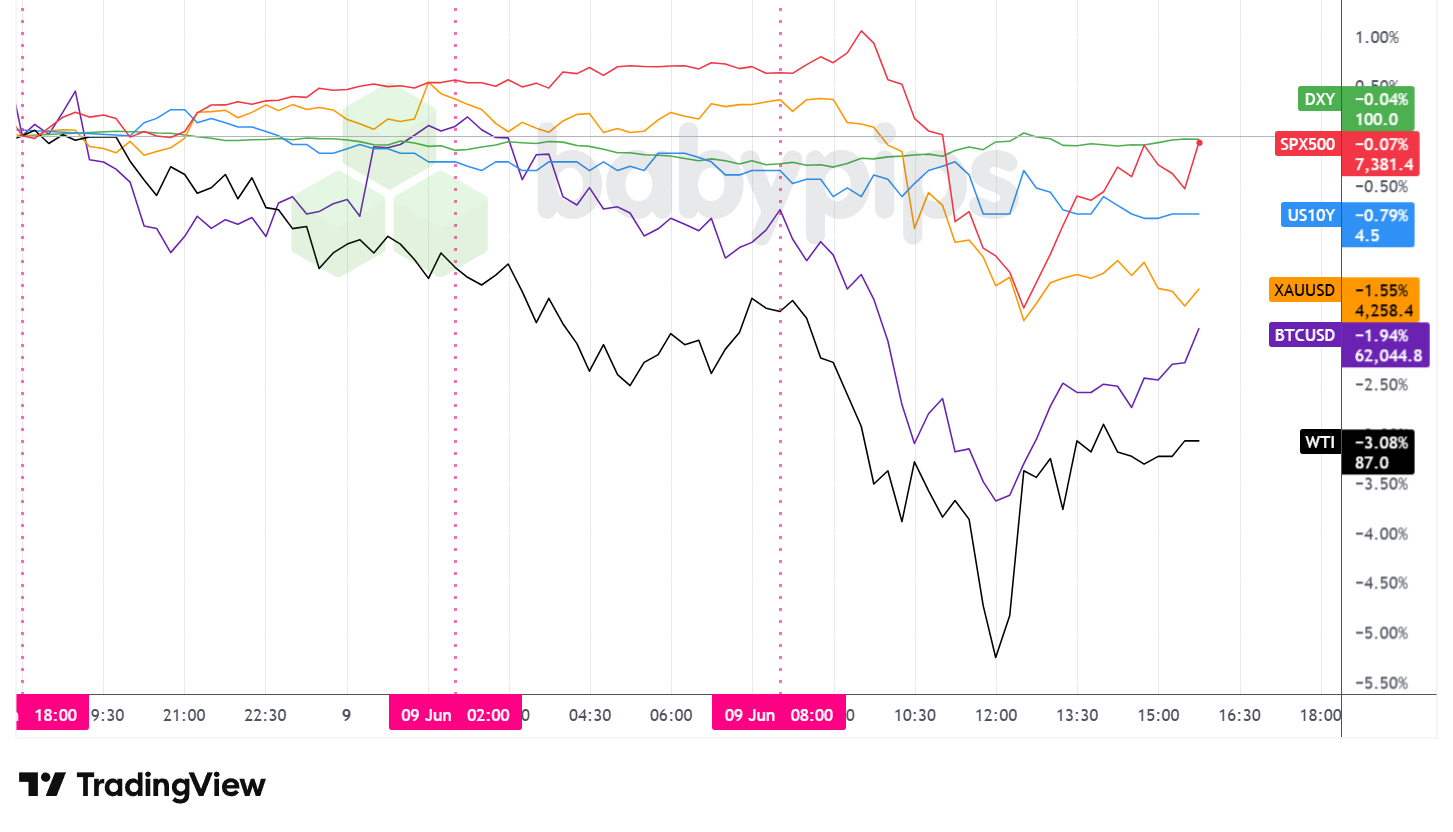

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Tuesday’s session was defined by mixed behavior early, which then lead into a tech-driven equity selloff and a US session escalation in the U.S.-Iran conflict. Most risk assets pared their worst intraday levels heading into the close, though the damage in oil, gold, and crypto was notable.

The S&P 500 closed down approximately 0.07%, settling near 7,381. The index climbed gradually through the Asian and European hours to reach intraday highs near the 7,480 area before turning lower as New York trading progressed. Selling accelerated toward midday, pushing the index to session lows near the 7,237 area, before a broad recovery returned it to near-flat territory by the close. Notably, around 370 of the index’s component stocks ended the day in positive territory despite the headline loss, a pattern possibly consistent with a rotation away from high-valuation technology and semiconductor names and into a broader range of equities. Chipmakers, which had been leading the recovery from war-driven market lows, swung violently through the session, and the Nasdaq 100 closed down roughly 1.1%. Growing investor scrutiny of AI infrastructure spending valuations, combined with potential capital absorption concerns tied to the anticipated SpaceX IPO pricing this week, may have contributed to the sector’s pressure.

WTI crude oil was the session’s weakest performer, closing down roughly 3%, near the $87 area. Oil had been declining steadily throughout the Asian and London sessions, possibly reflecting a reduction in the supply risk premium that had accumulated during the period of Strait of Hormuz blockades, as signals emerged that some crude flows through the waterway were resuming — Kuwait’s offer to sell crude to Asian refiners for the first time since the conflict began was among those signals. Trump’s afternoon statement attributing the helicopter incident to Iran helped oil pare some of its steepest intraday losses, as the prospect of a U.S. military response reintroduced supply-side uncertainty to the market.

Gold closed down approximately 1.55%, settling near $4,258. The precious metal held relatively steady through the overnight hours before declining sharply after the New York open, possibly driven by a combination of profit-taking following a period of elevated pricing, the dollar’s intraday recovery from session lows, and pre-positioning ahead of Wednesday’s U.S. CPI report. Gold recovered partially from intraday lows near $4,237 into the close, a move that may have reflected a modest safe-haven bid as geopolitical risk resurfaced in the afternoon.

Bitcoin closed down approximately 1.94%, settling near $62,045. The cryptocurrency tracked the broader risk-off move through the U.S. session, falling to intraday lows near $60,748 before recovering alongside equities in the afternoon.

The U.S. 10-year Treasury yield declined approximately 0.79% on the day, settling near 4.50%. Yields had drifted lower through the Asian and early European hours, possibly reflecting pre-positioning ahead of Wednesday’s CPI release and rising geopolitical tensions. The yield briefly rose toward the 4.56 area around midday before reversing sharply lower, a move broadly consistent with the volatile equity action seen in the same window.

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Today’s wild intraday swings in oil and the rapid recovery in equities prove just how fast a geopolitical headline can flip the market. When price action reverses on a dime due to sudden comments from leaders, knowing the fundamentals isn’t enough—you need the psychological discipline to stick to your plan without panicking.

In “Unknown Market Wizards,” (⭐ 4.6★ | 1,400+ reviews on Amazon) Jack Schwager interviews under-the-radar trading pros to reveal what truly separates them from the pack: unbreakable mental resilience and rigid risk control. Learn how top traders stay clinical, manage their exposure, and execute flawlessly when the rest of the market is swept up in the emotion of geopolitical chaos.

Master Your Trading Mindset with Market Wizards!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

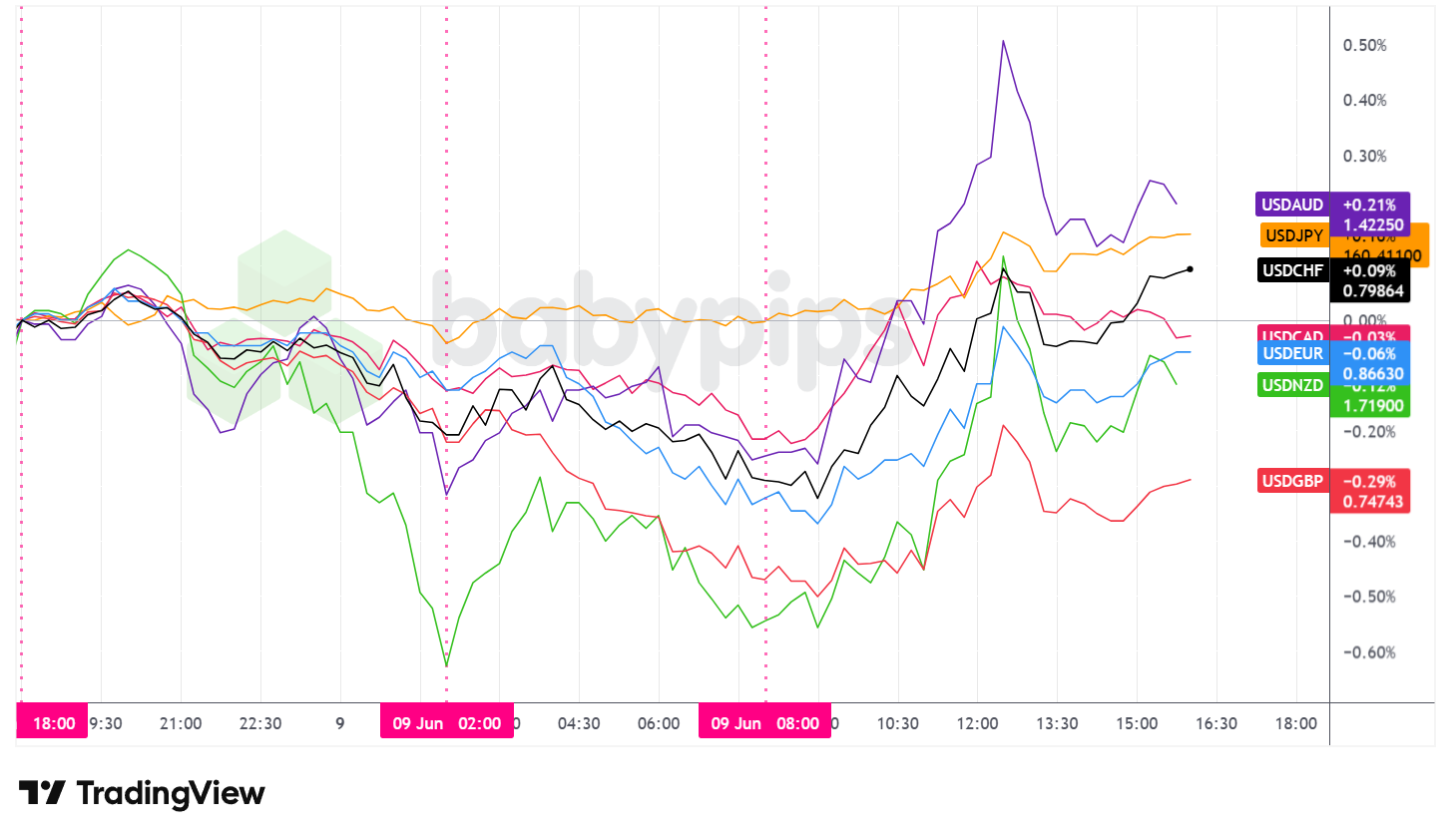

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar traded net lower against most major currencies from the Asian open through to the start of the U.S. session on Tuesday, before stabilizing and recovering a portion of those losses through the New York afternoon. At the close, the dollar was mixed on a daily basis, with an arguably net bearish lean overall.

During the Asian session, the dollar drifted broadly lower across most major currency pairs. Risk-on sentiment following Monday’s call from Trump for a ceasefire appeared to weigh on safe-haven demand for the greenback early in the session. China’s May trade data, which significantly beat expectations with exports rising 19.4% year-over-year and the trade surplus reaching $105.43 billion, likely reinforced a constructive tone for Asia-Pacific currencies. .

During the London session, the dollar continued to lose ground, reaching session lows near the time of the U.S. session open. The broader market backdrop remained supportive of risk assets through most of the European morning, with equities bid and oil extending its decline. The British pound saw saw some support during the London session, a move that may have been reinforced by the stronger-than-expected UK BRC Retail Sales data — the 3.4% year-over-year gain for May came in sharply above the -3.0% forecast, representing the biggest annual increase since April 2025.

The U.S. session brought a meaningful shift. As New York trading got underway, the dollar began to stabilize and recover against most of the major currencies, coinciding with a deterioration in risk sentiment as equities reversed sharply from intraday highs. Trump’s statement blaming Iran for the helicopter incident and signaling that the U.S. must respond may have added a further safe-haven impulse to the dollar in the second half of the session.

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Today’s daily recap highlights a market driven geopolitical developments and shifts in Fed policy expectations. But as any pro will tell you, understanding market drivers can aren’t enough if the trader lacks the discipline to execute a solid plan on it.

In “Unknown Market Wizards,” (⭐ 4.6★ | 1,400+ reviews on Amazon) Jack Schwager interviews successful traders to reveal a common truth: their edge isn’t just knowledge or skills—it’s their psychological resilience and rigid risk control. Whether you’re navigating shifting geopolitical themes or top tier economic data, learn how the “wizards” stay clinical and execute when the rest of the market is emotional.

Master Your Trading Mindset with Market Wizards!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- API Crude Oil Stock Change for June 5, 2026 at 8:30 pm GMT

- Japan PPI for May 2026 at 11:50 pm GMT

- Australia Building Permits Final for April 2026 at 1:30 am GMT

- China CPI & PPI for May 2026 at 1:30 am GMT

- MBA 30-Year Mortgage Rate for June 5, 2026 at 11:00 am GMT

- U.S. CPI Growth Rate for May 2026 at 12:30 pm GMT

-

BoC Interest Rate Decision for June 10, 2026 at 1:45 pm GMT

- BoC Press Conference at 2:30 pm GMT

- EIA Crude Oil Stocks Change for June 5, 2026 at 2:30 pm GMT

- U.S. Monthly Budget Statement for May 2026 at 6:00 pm GMT

Wednesday’s calendar is headlined by the U.S. CPI report for May at 12:30 pm GMT, which carries elevated significance given ongoing uncertainty about the Fed’s rate path and could either reinforce or push back against hawkish rate pricing heading into the summer.

The Bank of Canada interest rate decision at 1:45 pm GMT, followed by Governor Tiff Macklem’s press conference at 2:30 pm GMT, is the second major event for currency traders and will be closely watched for any shift in the BoC’s guidance following Tuesday’s stronger-than-expected April trade data.

China CPI and PPI at 1:30 am GMT may also attract early attention given the broad-based strength of Tuesday’s Chinese trade figures.

Stay frosty out there, forex friends!

Tuesday’s U.S.-Iran escalation sent the market spinning from risk-on to risk-off in minutes. Most traders react to headlines, but they don’t understand the mechanism beneath them. Premium members can read our lesson:

📖 Geopolitical Risk, Trade Policy, and Safe Haven Flows

Reading this helps you understand how geopolitical events move currencies, which currencies act as safe havens when the world becomes uncertain, and why the dollar strengthened as risk sentiment collapsed.

And if you’re not a Premium subscriber yet, now’s a good time to sign up. With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just what the chart is showing, but the fundamental forces behind every market swing, from geopolitical escalations to central bank decisions to risk sentiment shifts.