Markets kicked off the holiday-shortened week with a decidedly geopolitical flavor on Tuesday, as progress toward a US-Iran peace deal overshadowed fresh overnight military exchanges in the Strait of Hormuz and drove a complex mix of risk-on and risk-off price action across asset classes. The US dollar climbed steadily from the Asia open through the London close to finish as the strongest major currency on the day, while gold retreated as deal optimism eroded some of its recent safe-haven premium.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- US forces reported it conducted self-defense strikes against Iran near the Strait of Hormuz overnight

- U.K. BRC Shop Price Inflation for May 2026: 1.2% (1.2% forecast; 1.0% previous)

- Japan Leading Indicators Index for March 2026: 114.0 (114.5 forecast; 113.3 previous)

- U.K. CBI Distributive Trades for May 2026: -46.0 (-60.0 forecast; -68.0 previous)

- Canada Manufacturing Sales Prel for April 2026: 4.6% m/m (1.4% m/m forecast; 3.0% m/m previous)

- U.S. Chicago Fed National Activity Index for April 2026: 0.14 (-0.3 forecast; -0.2 previous)

- U.S. House Price Index for March 2026: 0.1% m/m (0.1% m/m forecast; 0.0% m/m previous)

- U.S. S&P/Case-Shiller Home Price for March 2026: 1.0% m/m (0.5% m/m forecast; 0.4% m/m previous)

- CB U.S. Consumer Confidence for May 2026: 93.1 (92.0 forecast; 92.8 previous)

- U.S. Dallas Fed Manufacturing Index for May 2026: 0.4 (-1.0 forecast; -2.3 previous)

- ECB Board member Schnabel said they should raise interest rates in June, even if ongoing peace talks with Iran yield a deal

- Trump to hold rare cabinet meeting at Camp David as Iran tensions rise over US strikes

Promoted: Day traders & Scalpers have better odds of making great decisions if they’re alerted to market catalysts right away, like news of a potential US-Iran agreement, right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

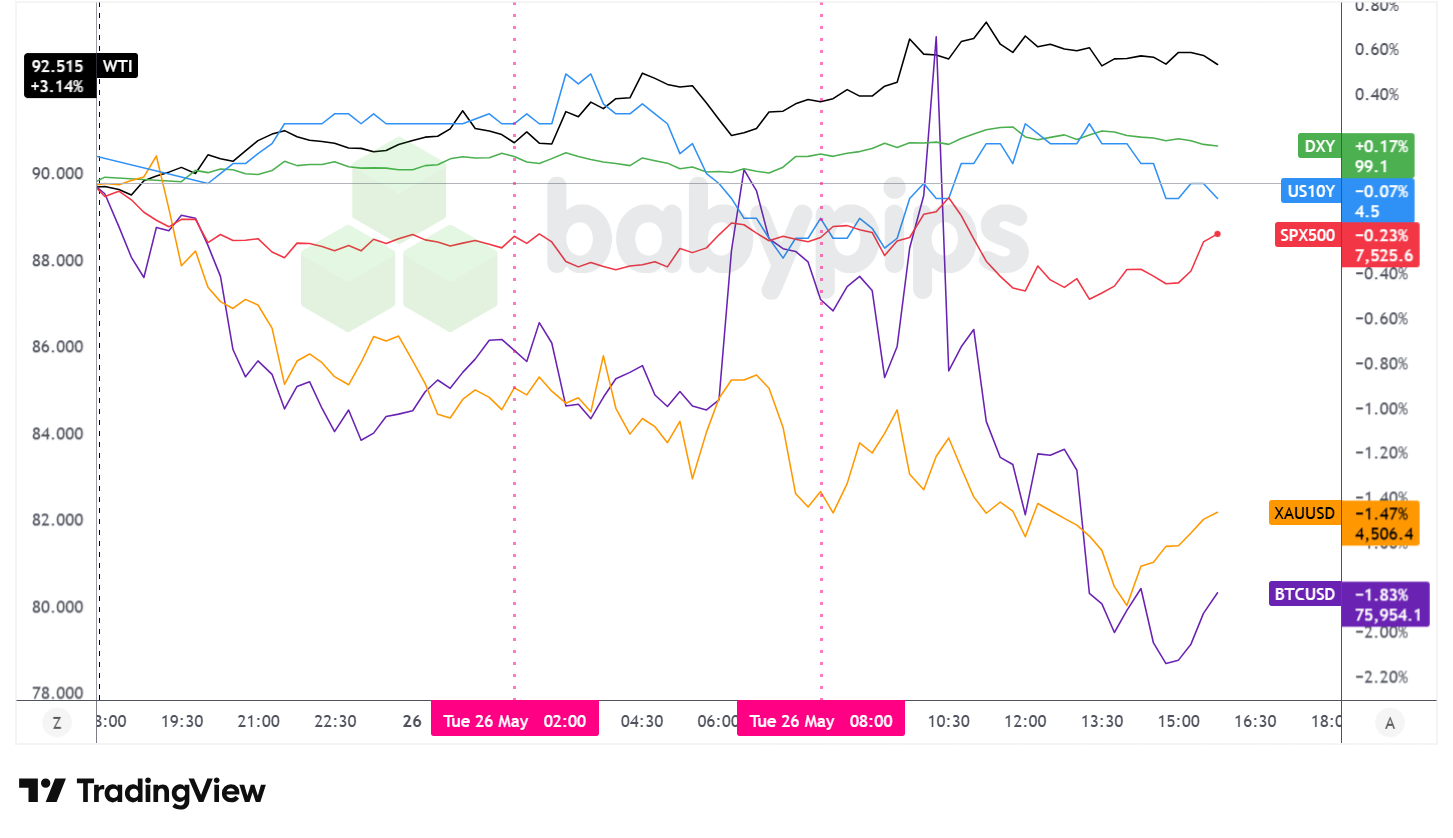

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Tuesday’s session was shaped almost entirely by the evolving US-Iran diplomatic situation. The two sides were simultaneously exchanging strikes in the Strait of Hormuz and negotiating through Qatari mediation, and markets appeared to read that combination as proximity to a finish line rather than a conflict at risk of widening. Progress reportedly centered on Iran’s $24 billion in frozen assets as the final obstacle to a Memorandum of Understanding, while President Trump publicly softened his prior position on Iran’s enriched uranium, indicating that destruction in place under IAEA supervision or transfer to a third country would be acceptable. Secretary of State Rubio cautioned that deal language would likely take a few more days to finalize.

The S&P 500 touched record territory intraday before settling back to close at approximately 7,525.6, off around 0.23% on the day. The index briefly cleared prior highs around the 10:30 AM ET hour before fading through the afternoon, suggesting that while peace deal optimism provided a meaningful bid, traders remained reluctant to press the move aggressively into the close without more tangible diplomatic progress.

US consumer confidence for May came in at 93.1, a modest beat relative to the 92.0 forecast, though it slipped slightly from the prior month’s upwardly revised reading of 92.8 as consumers cited rising prices linked to the ongoing conflict. The Chicago Fed National Activity Index also surprised to the upside in April at 0.14 versus a -0.3 consensus, and the Dallas Fed Manufacturing Index turned positive at 0.4 against a -1.0 forecast, adding to a picture of resilient US economic activity.

WTI crude oil was the session’s most volatile asset and its strongest performer, gaining approximately 3.14% to trade near $92.52 per barrel. Global benchmark Brent rose to around $100 a barrel during the session, partially recovering from Monday’s near-7% decline. The rebound appeared to reflect the rise in overnight hostilities, the unresolved question of the Hormuz passage fees Iran has sought to impose, and ongoing uncertainty over the frozen assets dispute.

Gold fell approximately 1.47% to trade near $4,506 per ounce, unwinding some of its recent safe-haven premium in a move that was broad and steady across all three sessions. The decline likely reflected U.S. dollar strength, as well as easing inflation concerns tied to a possible Hormuz reopening that may have reduced pressure on the Federal Reserve to hike rates aggressively, as signaled by the tick lower in yields.

Bitcoin declined roughly 1.83% to trade near $75,954. The cryptocurrency spiked intraday toward approximately $78,000 around the US open before reversing sharply and drifting lower through the afternoon, leaving it as one of the session’s weaker performers with no clear single catalyst apparent for the reversal.

The 10-year Treasury yield edged slightly lower, settling near 4.50%, off around 0.07% on the day. The modest bond bid appeared to correlate with reduced near-term inflation expectations tied to the possibility of a Hormuz resolution, with traders also paring back wagers on near-term Federal Reserve rate hikes on the view that a de-escalation of the conflict could meaningfully ease energy-driven price pressures.

Promoted: The Prop Firm Built for Serious Traders.

Don’t let your trading strategy be held back by capital limitations. Alpha Capital Group offers access to simulated funded accounts from $5K to $200K, with entry prices starting as low as $40. They are distinguished by their features, including zero commissions, unlimited trading days during evaluation, and an 80% profit split. Start with a professional-sized account and scale your buying power up to $2M. Join 250K+ traders in 180+ countries today.

Learn more about Alpha Capital Group and current discount codes here!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

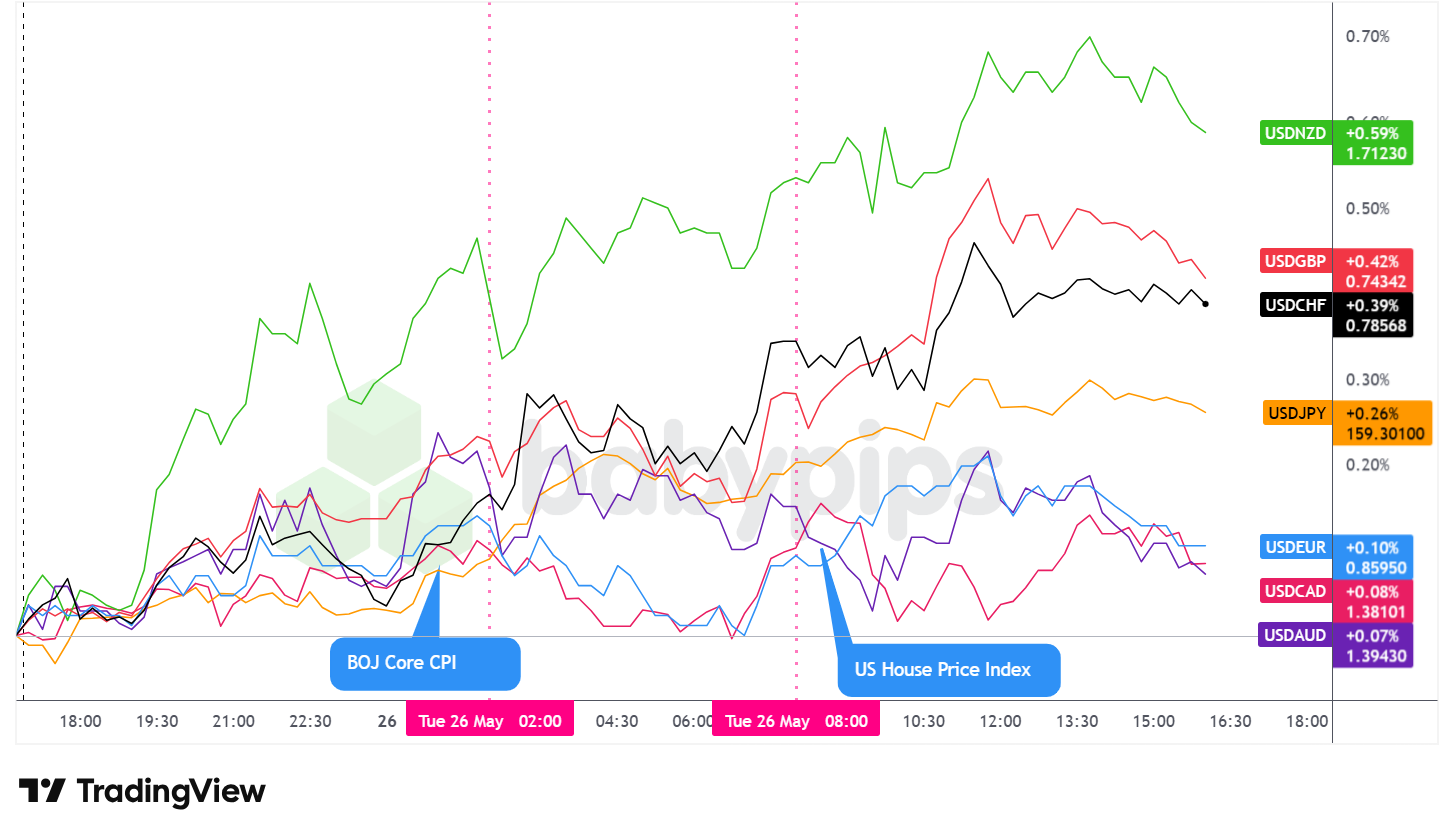

Overlay of USD vs. Majors – Chart Faster With TradingView

The US dollar trended broadly higher from the Tuesday Asia open through approximately the London close, before pulling back modestly heading into the end of the US session. At the Tuesday close, the dollar finished as the best-performing major currency on the day, posting gains against all seven major pairs tracked on the overlay.

During the Asian session, the dollar traded with a net bullish lean against the major currencies. The overnight geopolitical backdrop was particularly active: US forces confirmed sinking two IRGC mine-laying speedboats in the Strait of Hormuz and striking a missile site at Bandar Abbas, while Iran launched anti-ship cruise missiles toward US naval assets in response. Despite the renewed hostilities, markets appeared to interpret the situation as consistent with a deal in its closing stages, with CENTCOM maintaining that the ceasefire framework remained operative.

During the London session, the dollar extended its gains as the bullish trend continued with little interruption. ECB policymakers confirmed market expectations of a June rate hike but offered limited guidance on additional tightening, which may have weighed modestly on the euro. UK CBI Distributive Trades for May printed at -46.0 against a -60.0 forecast, better than expected but still deeply negative, providing limited support for sterling.

During the US session, the dollar held its gains through the early hours, likely supported by the string of better-than-expected US data including the consumer confidence beat and the positive Dallas Fed print. The greenback pulled back modestly from its intraday highs in the afternoon, with the late-day retreat possibly reflecting some position squaring as traders awaited further news from the Doha mediation talks. The pullback was orderly and did not materially alter the day’s dominant direction.

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Most trading mistakes aren’t technical—they’re psychological. In the classic “Trading in the Zone” by Mark Douglas (⭐ 4.7★ | 10,000+ reviews on Amazon), you’ll learn how to master the probabilistic thinking and emotional discipline mentioned in today’s article. If you struggle with hesitation or breaking your rules, this is your manual for consistent execution.

Click on the link to learn more about “Trading in the Zone” by Mark Douglas!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- Australia CPI Growth Rate for April 2026 at 1:30 am GMT

-

New Zealand RBNZ Interest Rate Decision for May 27, 2026 at 2:00 am GMT

- New Zealand RBNZ Press Conference at 3:00 am GMT

- France Consumer Confidence for May 2026 at 6:45 am GMT

- Swiss Economic Sentiment Index for May 2026 at 8:00 am GMT

- Euro area ECB Financial Stability Review at 8:00 am GMT

- U.S. Fed Logan Speech at 8:00 am GMT

- U.S. MBA 30-Year Mortgage Rate & Applications for May 22, 2026 at 11:00 am GMT

- U.S. ADP Employment Change Weekly for May 9, 2026 at 12:15 pm GMT

- U.S. Richmond Fed Manufacturing Index for May 2026 at 2:00 pm GMT

- U.S. Dallas Fed Services Index for May 2026 at 2:30 pm GMT

- U.S. Fed Cook Speech at 7:55 pm GMT

- U.S. API Crude Oil Stock Change for May 22, 2026 at 8:30 pm GMT

Wednesday’s calendar is headlined by two high-impact events in the early Asian session. The Australia CPI Growth Rate for April 2026 at 1:30 AM GMT and the RBNZ Interest Rate Decision at 2:00 AM GMT, followed by the RBNZ Press Conference at 3:00 AM GMT, could drive significant moves in AUD and NZD pairs. Bank of Japan Governor Ueda’s Speech also warrants close attention given Deputy Governor Himino’s reaffirmation of the rate hike trajectory on Tuesday.

Into the European morning, the ECB Financial Stability Review at 8:00 AM GMT may offer additional ECB color on risks stemming from the Middle East conflict and energy market dynamics. The Swiss Economic Sentiment Index for May 2026 will print at 8:00 AM GMT, alongside the U.S. Fed Logan Speech, which could attract attention for any commentary on the inflation and policy path.

The US session brings the ADP Employment Change at 12:15 PM GMT and the Richmond Fed Manufacturing Index at 2:00 PM GMT, both of which could inform views on US economic momentum.

Fed Cook’s Speech at 7:55 PM GMT and the API Crude Oil Stock Change at 8:30 PM GMT round out the day, with the crude inventory reading potentially adding to oil market volatility given the ongoing Hormuz situation.

Stay frosty out there, forex friends!

Tuesday’s market action was shaped almost entirely by US-Iran diplomatic progress and overnight military exchanges in the Strait of Hormuz. But understanding why the dollar strengthened while gold retreated during simultaneous escalation and peace talks requires knowing how geopolitical risk actually moves currencies. Premium members can read our lesson:

📖 Geopolitical Risk, Trade Policy, and Safe Haven Flows

Reading this helps you understand how geopolitical events and trade policy shifts drive currency moves, which safe havens to watch when global tensions rise, and how to read conflicting signals when military risk and diplomatic progress happen simultaneously.

And if you’re not a Premium subscriber yet, consider joining to unlock the full School of Pipsology curriculum.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just what the market is pricing in today, but the geopolitical and macroeconomic forces driving those price moves.