Iran-U.S. deal optimism swept through financial markets on Monday, pulling crude oil sharply lower while equities, gold, and Bitcoin all advanced in holiday-thinned conditions. With U.S. cash markets closed for Memorial Day and much of Europe also offline for local bank holidays, thin liquidity likely amplified the session’s moves, leaving the U.S. dollar as the weakest major currency at the day’s close.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Over the weekend, Trump announced that a peace deal has been “largely negotiated” with an announcement coming, prompting large gap opens in the futures market on Monday.

- China FDI (YTD) for April 2026: -10.3% y/y (-6.8% y/y forecast; -7.3% y/y previous)

- Canada Wholesale Sales Prel for April 2026: 0.1% m/m (0.8% m/m forecast; 1.9% m/m previous)

- European and U.S. cash markets were closed on Monday for various holidays

- U.S. President Donald Trump said on Truth Social Monday that Iran negotiations were “proceeding nicely,” adding to weekend signals that an interim deal to reopen the Strait of Hormuz may be approaching; Pakistani military chief Asim Munir separately told China an agreement is “close to being reached”

Promoted: Day traders & Scalpers have better odds of making great decisions if they’re alerted to market catalysts right away, like news of a potential US-Iran agreement, right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

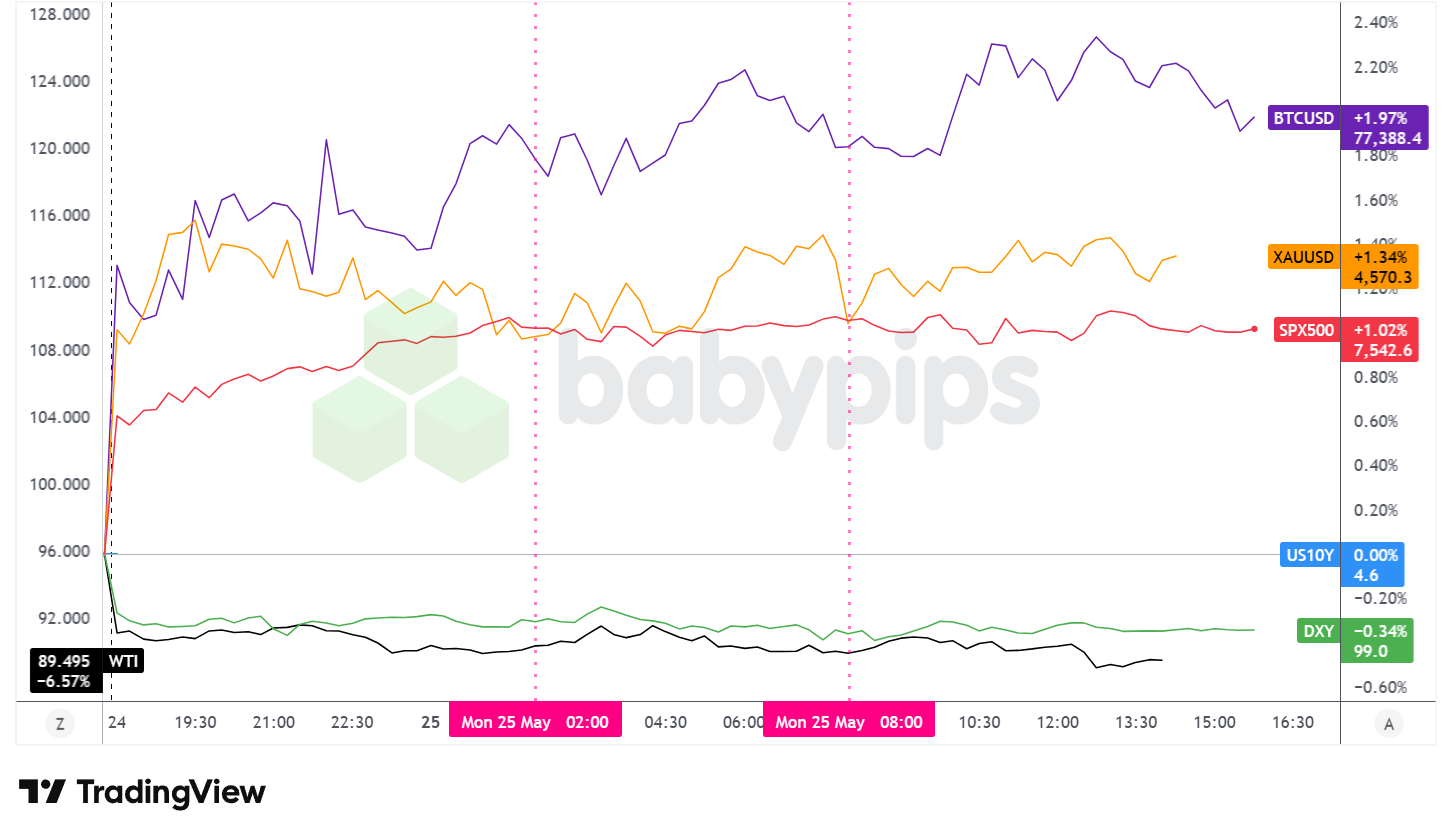

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Monday’s price action was shaped almost entirely by a single macro theme: growing optimism that the U.S. and Iran are nearing an agreement to reopen the Strait of Hormuz and restore regional oil flows. With U.S. cash equity and bond markets shuttered for the Memorial Day holiday, and the UK, Switzerland, Norway, and Denmark also closed for local bank holidays, volumes were notably thin across most asset classes. That context likely amplified the magnitude of moves, particularly in crude oil, where the relief trade was pronounced.

WTI crude oil was the session’s standout mover, declining roughly 6.57% to trade near $89.50 per barrel. The sharp drop correlated with weekend reports of a preliminary U.S.-Iran memorandum of understanding and was reinforced by Trump’s Monday post describing talks as “proceeding nicely.” The move unwound a meaningful portion of the war-risk premium that had accumulated in oil prices since the conflict’s outbreak in February.

S&P 500 futures advanced approximately 1.02% to around 7,542.6. With U.S. cash markets closed for the holiday, this figure reflects futures activity. The gains aligned with a broadly constructive global tone: Europe’s Stoxx 600 climbed for a sixth straight session to its highest close since the outbreak of the Iran war, and the MSCI All Country World Index reportedly reached an all-time high closing level.

Gold added roughly 1.34%, trading near $4,570. The precious metal likely benefited from a combination of the weaker dollar making bullion more accessible to buyers in other currencies and persistent underlying uncertainty around the Iran situation. Key unresolved issues including uranium enrichment, sanctions relief terms, and the Israel-Lebanon front may have supported continued safe-haven demand even as the headline diplomatic tone improved.

Bitcoin gained approximately 1.97% to trade near $77,388.4. The advance was broadly consistent with the session’s risk-on character, though the individual BTC chart shows price action consolidating in a relatively narrow range between approximately $77,090 and $77,835 for much of the day after an initial surge around the Monday Asia open.

The 10-year U.S. Treasury yield was little changed on the day, reflecting the closure of U.S. bond markets for the Memorial Day holiday.

Promoted: The Prop Firm Built for Serious Traders.

Don’t let your trading strategy be held back by capital limitations. Alpha Capital Group offers access to simulated funded accounts from $5K to $200K, with entry prices starting as low as $40. They are distinguished by their features, including zero commissions, unlimited trading days during evaluation, and an 80% profit split. Start with a professional-sized account and scale your buying power up to $2M. Join 250K+ traders in 180+ countries today.

Learn more about Alpha Capital Group and current discount codes here!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

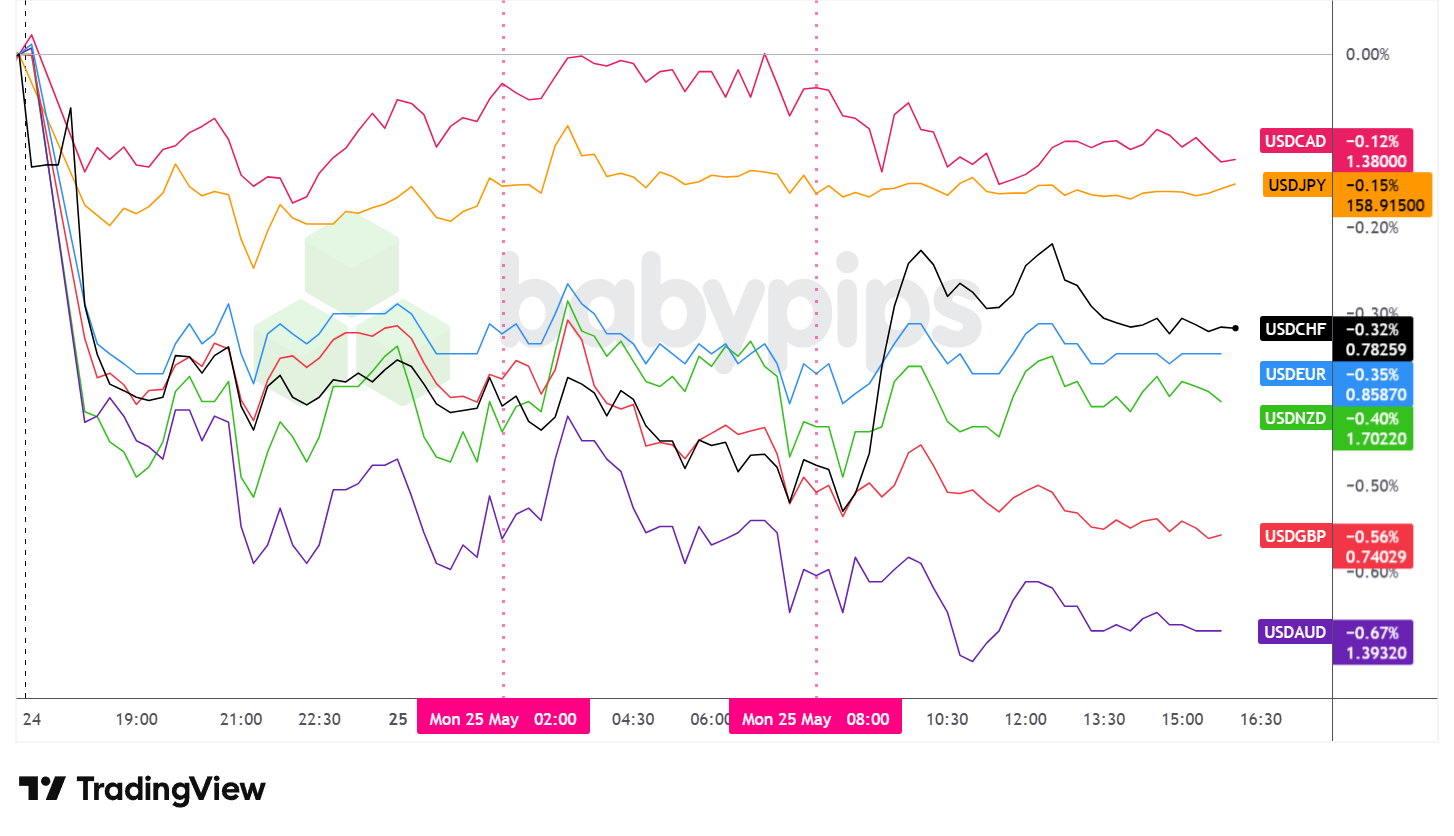

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar closed Monday as the weakest performing major currency, pressured from the outset by the shift in geopolitical risk sentiment and unable to reclaim meaningful ground as the session wore on through thinly traded holiday conditions.

At the Monday Asia open, the dollar fell sharply against the major currencies as markets digested weekend reports of U.S.-Iran deal progress alongside the PBOC’s yuan fixing at a three-year high for the Chinese currency. The move lower was swift but relatively contained; the dollar quickly stabilized and spent the remainder of the Asian session drifting sideways around the lower levels established at the open. The overlay chart shows the bulk of the dollar’s daily losses locked in during this initial burst of activity, with AUD and GBP among the major currencies that the dollar fell against the most.

The London session offered little additional directional catalyst. With the UK and much of continental Europe offline for bank holidays, liquidity was exceptionally thin and currency pairs largely drifted without meaningful follow-through in either direction. The dollar held its earlier losses but did not extend them materially during this window.

The U.S. session continued in a similar vein, with Memorial Day keeping U.S. cash market participants on the sideline and overall participation remaining light. The dollar traded choppy and sideways with no meaningful recovery attempt, leaving it broadly weaker at the close against all major peers.

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Most trading mistakes aren’t technical—they’re psychological. In the classic “Trading in the Zone” by Mark Douglas (⭐ 4.7★ | 10,000+ reviews on Amazon), you’ll learn how to master the probabilistic thinking and emotional discipline mentioned in today’s article. If you struggle with hesitation or breaking your rules, this is your manual for consistent execution.

Click on the link to learn more about “Trading in the Zone” by Mark Douglas!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- U.K. BRC Shop Price Inflation for May 2026 at 11:01 pm GMT

- Japan Leading Indicators Index for March 2026 at 5:00 am GMT

- U.K. CBI Distributive Trades for May 2026 at 10:00 am GMT

- Canada Manufacturing Sales Prel for April 2026 at 12:30 pm GMT

- Chicago Fed National Activity Index for April 2026 at 12:30 pm GMT

- U.S. House Price Index for March 2026 at 1:00 pm GMT

- U.S. S&P/Case-Shiller Home Price for March 2026 at 1:00 pm GMT

- CB U.S. Consumer Confidence for May 2026 at 2:00 pm GMT

- Dallas Fed Manufacturing Index for May 2026 at 2:30 pm GMT

- U.S. Money Supply for April 2026 at 5:00 pm GMT

Tuesday brings U.S. markets back online in full following the Memorial Day holiday, and the May CB Consumer Confidence reading at 2:00 pm GMT will be the day’s headliner. The reading arrives against a backdrop of elevated energy prices relative to pre-conflict norms, ongoing Middle East diplomatic uncertainty, and the transition at the Federal Reserve following Kevin Warsh’s swearing-in last Friday.

U.S. housing data due at 1:00 pm GMT, including the House Price Index and S&P/Case-Shiller figures for March, may attract attention given continued sensitivity to mortgage rate and affordability conditions.

Canada’s Manufacturing Sales preliminary figure and the Chicago Fed National Activity Index round out the morning releases. Any fresh Iran deal headlines, particularly around the unresolved sticking points of uranium enrichment, sanctions relief, and the Israel-Lebanon front, will likely continue to drive sentiment ahead of the data.

Stay frosty out there, forex friends!

Promoted: Protecting your trading capital starts with securing your access. Don’t let a weak password be the single point of failure for your brokerage or prop firm accounts. LastPass simplifies your digital life by generating and storing complex, encrypted passwords for every site you use.

Try LastPass for Free Today!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Monday’s market moves were driven by shifting geopolitical risk sentiment around Iran-U.S. negotiations, but many traders don’t fully understand how these events reshape currency flows and safe-haven demand. Premium members can read our lesson:

📖 Geopolitical Risk, Trade Policy, and Safe Haven Flows

Reading this helps you understand how geopolitical events move currency pairs, why the dollar weakened even as oil fell, and which safe havens to watch when regional tensions shift.

And if you’re not a Premium subscriber yet, now’s a good time to sign up.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just which currencies move in response to geopolitical shocks, but why institutional flows pivot between risk-on and risk-off regimes when the narrative shifts.