We’re kicking off a new week of FX trading by throwing AUD/JPY onto the watchlist today. Check out the fresh move lower and potential catalysts that could keep the bear train going.

Intermarket Snapshot

| Equity Markets | Bond Yields | Commodities & Crypto |

| DAX: 12310.88 -1.26% FTSE: 7320.45 -0.30% S&P 500: 2990.12 -0.07% DJIA: 26892.96 -0.16% |

US 10-yr 1.678% -0.075 Bund 10-YR -0.581% -0.061 UK 10-YR: 0.560% -0.068 JPN 10-YR: -0.217% +0.011 |

Oil: 58.05 -0.07% Gold: 1530.40 +1.01% Bitcoin: 9806.96 -2.463% Etherium: 206.45 -1.98% |

Fresh Market Headlines & Economic Data:

- Oil drops amid conflicting reports about speed of Saudi recovery

- Flash U.S. Manufacturing PMI at 51.0 (50.3 in August). 5-month high

- IHS Markit Flash Eurozon PMI falls in September further into contractionary territory to 45.6 vs. 47.0 in August.

- Boris Johnson seeks Brexit deal progress in New York talks

- UK’s top court to rule on Tuesday on Johnson’s parliament suspension

- Corbyn faces showdown with party members over Brexit

- Visa’s UK Consumer Spending Index shows spending down -1.3% y/y in August

- Euro zone economic rebound not in sight: ECB’s Draghi

- ECB’s Knot: New economic stimulus program ‘disproportionate’

- Australian services PMI rebounds to 51.9 in Sept (49.3 previous) whle manufacturing PMI contracts to 49.4 (50.9 previous)

Upcoming Potential Catalysts on the Forex Calendar:

- Fed’s Bullard speaks at 6:00 pm GMT

- Japan Flash manufacturing PMI at 1:30 am GMT (Sept. 24)

- Bank of Japan Governor Kuroda speaks at 6:30 am GMT (Sept. 24)

- German Ifo Business survey at 9:00 am GMT (Sept. 24)

- U.K. Public sector borrowing at 9:30 am GMT (Sept. 24)

- Reserve Bank of Australia Governor Lowe speaks at 10:55 am GMT (Sept. 24)

- U.S. Home prices at 2:00 pm GMT (Sept. 24)

- U.S. Consumer confidence at 3:00 pm GMT (Sept. 24)

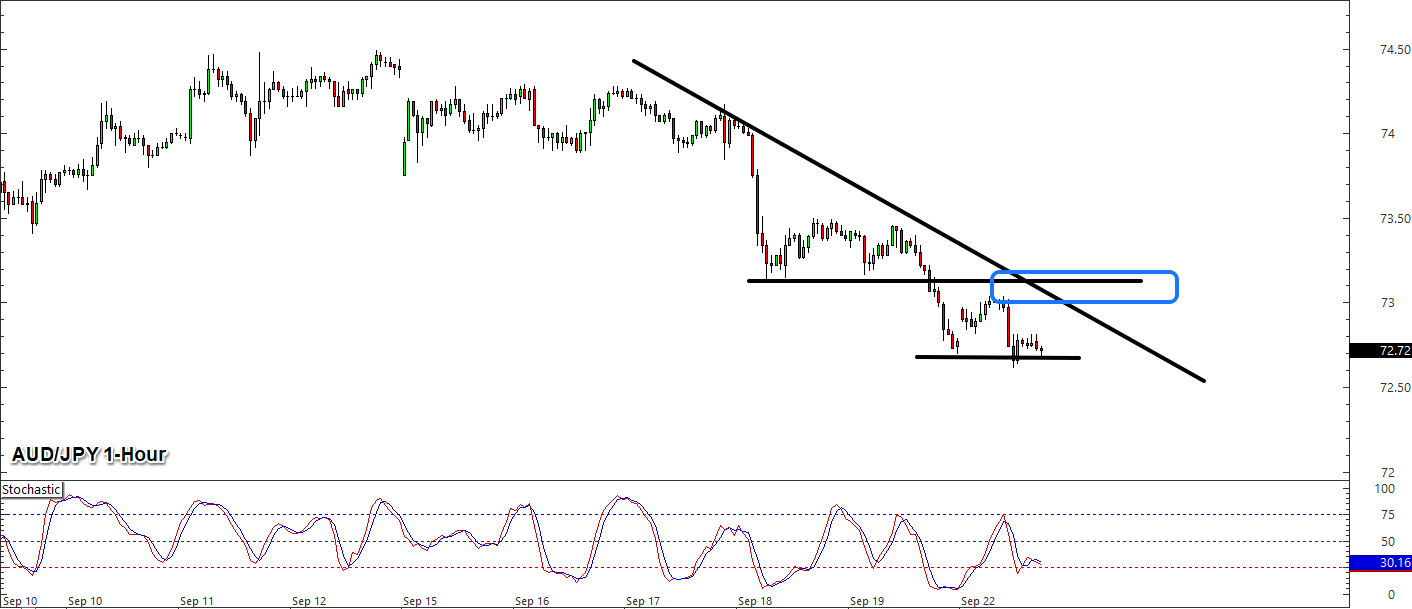

What to Watch: AUD/JPY

Last week, AUD/JPY sentiment shifted back to the longer-term trend lower in reaction to the Bank of Japan’s latest monetary policy meeting (no massive stimulus package as expected) and likely on expectations of more rate cuts from the Reserve Bank of Australia. So, the momentum is back in favor of the bears on AUD/JPY, and after a gap higher at this week’s open, the bears have taken back control so far in the U.S. session.

Looking forward, we’ve got potential catalysts for both the Aussie and yen coming in the form of speeches from both BOJ Governor Kuroda and RBA Governor Lowe. Odds are that we’re not lot likely going to hear something new on economic conditions or monetary policy outlook, but if we do the reaction would be likely a fast and furious short-term spike in volatility for either currency. Also, today’s focus and concern for the global economy after another round of weak PMI updates from Europe will likely play a role in direction sentiment bias for now.

For the bears, the current global risk sentiment and price action is in your favor, and any negative comments from RBA Governor Lowe would likely push AUD/JPY lower. That makes the potential break of the minor support around current levels (72.70ish) one to watch, but if you’re more conservative, a bounce up to the falling ‘highs’ pattern and major psychological level of 73.00 a potential shorting area.

For the bulls, it’s a tough case to argue for a long position unless we get surprise commentary from either central bank governor today AND strong break of the falling ‘highs’ pattern and Thursday/Friday’s minor resistance area around 73.50. A positive turn in the U.S.-China trade negotiation story would likely be a big boost to AUD/JPY as well. 73.50 is just outside of the daily ATR range of around 60 pips, but with a surprise central bank comment, this could easily be reached and broken within the next session or two.