Markets opened Monday cautiously as traders navigated nine weeks of Strait of Hormuz disruption and assessed new diplomatic signals from Tehran that offered some hope for resolution. Oil prices stayed elevated, equities clung to record territory, and gold and Bitcoin pulled back as participants held their positions ahead of a week packed with mega-cap tech earnings and five major central bank decisions. The U.S. dollar ended the session mixed but arguably net negative, reflecting the broadly uncertain and event-driven mood.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- China Industrial Profits (YTD) for March 2026: 15.5% y/y (18.0% y/y forecast; 15.2% y/y previous)

- Japan Leading Indicators Index for February 2026: 113.3 (112.4 forecast; 112.1 previous)

- Germany GfK Consumer Confidence for May 2026: -33.3 (-30.0 forecast; -28.0 previous)

- U.K. CBI Distributive Trades for April 2026: -68.0 (-47.0 forecast; -52.0 previous)

- Dallas Fed Manufacturing Index for April 2026: -2.3 (-0.8 forecast; -0.2 previous)

- Iran passed a new proposal to the White House via Pakistani mediators, offering to reopen the Strait of Hormuz and lift the naval blockade first, with nuclear negotiations to follow at a later stage

- U.S. Secretary of State Rubio said Iran wants to retain control of the Strait of Hormuz, which is an unacceptable condition for the U.S.

- The White House confirmed national security officials reviewed the Iranian proposal but maintained red lines on any deal, including preventing Tehran from obtaining a nuclear weapon

Promoted: Day traders & Scalpers have better odds of making great decisions if they see market catalysts right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

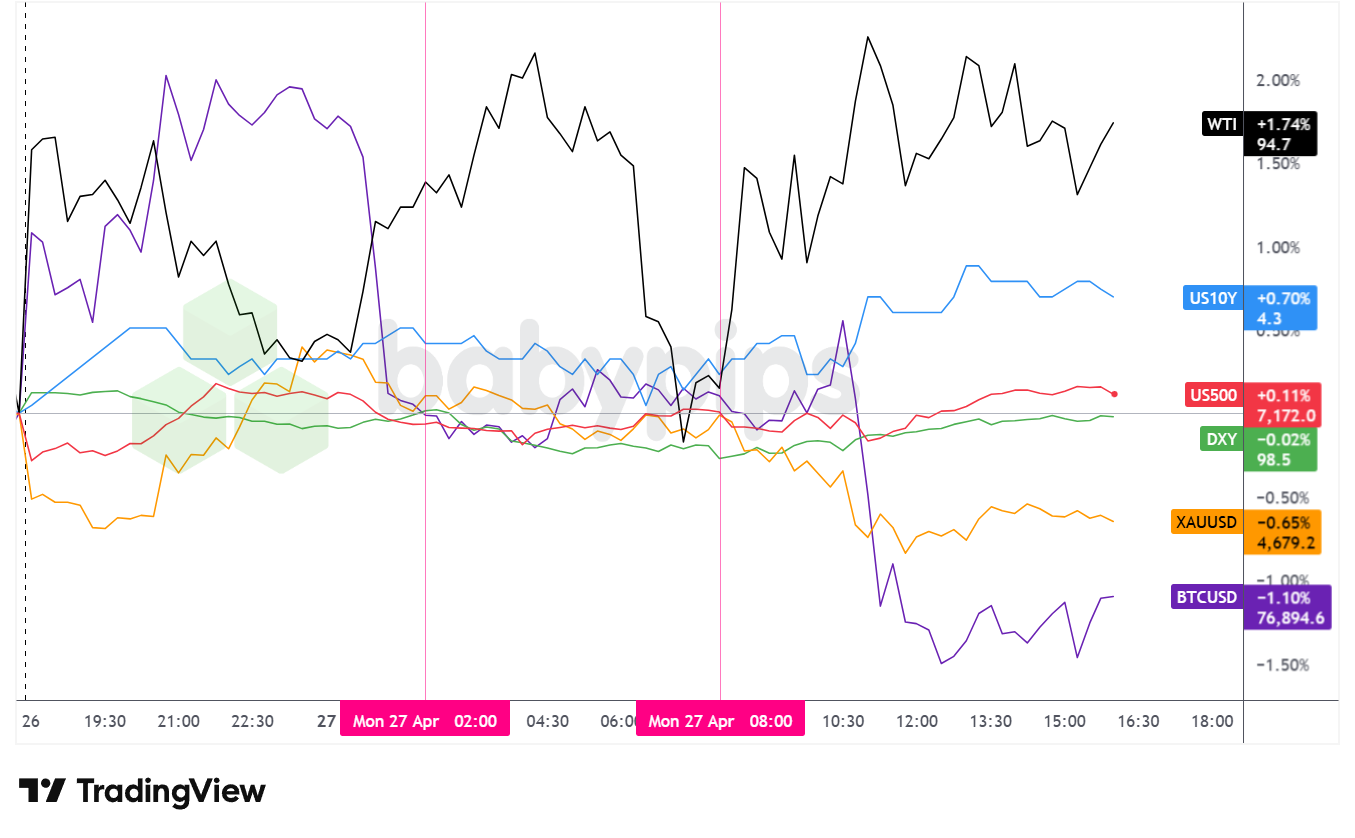

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Monday’s session was defined by patience and restraint. With mega-cap tech earnings, five major central bank decisions, and an unresolved geopolitical standoff all converging on the same week, participants appeared reluctant to commit to strong directional bets across most asset classes.

WTI crude oil was the session’s standout performer, closing up approximately 1.75% to around $94.75 per barrel. The intraday chart tells a volatile story: prices opened the week on the front foot during Sunday evening trade as Iran’s continued Hormuz closure and Trump’s cancelled Islamabad envoy trip elevated the risk premium, but the early gains proved short-lived. The chart shows prices pulling back through the Asia session and plunging to a session low near the $92.80 area around the London open, before recovering steadily through the remainder of the day.

The fundamental backdrop keeping a floor under oil remained unchanged: the Strait of Hormuz has been effectively closed for a ninth straight week, with daily transits reduced to near zero. Gains off the session low were partly trimmed as Iran’s proposal to reopen Hormuz gained wider coverage following the Axios report, with the prospect of a diplomatic resolution introducing some caution into long positions.

The S&P 500 closed fractionally higher, up approximately 0.12% to around 7,172, holding near record territory. The index tracked a narrow intraday range throughout the session, reflecting broad hesitation ahead of a massive earnings slate. Participants appeared largely content to wait for results from Alphabet, Microsoft, Amazon, and Meta, all due Wednesday, followed by Apple on Thursday. The relative calm in equities despite elevated geopolitical risk possibly reflects continued confidence in the AI-driven technology rally, with chip names staying well bid through the session.

Gold closed lower, declining approximately 0.66% to around $4,678 per ounce. The precious metal peaked during the Asia session near $4,720 before selling off steadily from around 02:00 ET through the rest of the session. The decline possibly reflected a partial unwinding of geopolitical risk premium as the Iranian diplomatic proposal began circulating more widely, though the downside appeared contained given the continued uncertainty around the conflict.

Bitcoin closed down approximately 1.73% to around $76,912. The cryptocurrency peaked near $79,500 in the early Asia session before a sharp and persistent decline through the Asian and London sessions, with the largest leg lower coinciding with a deterioration in broad market tone around the London open. Bitcoin’s weakness appeared to broadly track shifting risk appetite, consistent with its sensitivity to swings in speculative sentiment.

The U.S. 10-year Treasury yield closed up approximately 0.77% to around 4.332%, grinding higher across the session. Yields pushed up despite the soft Dallas Fed Manufacturing print, possibly reflecting a combination of pre-positioning ahead of this week’s Federal Reserve decision and ongoing inflation concerns tied to the sustained energy supply disruption from the Hormuz closure.

Promoted: Pay Once. Trade Forever.

Most prop firms quietly drain your account with monthly subscription fees long before you ever see a payout. Tradeify operates differently — evaluations are a one-time purchase with no recurring charges. Pass the eval, get activated instantly, and keep more of what you earn. With ~$150M in verified payouts and growing, the math speaks for itself.

Learn More About Tradeify!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

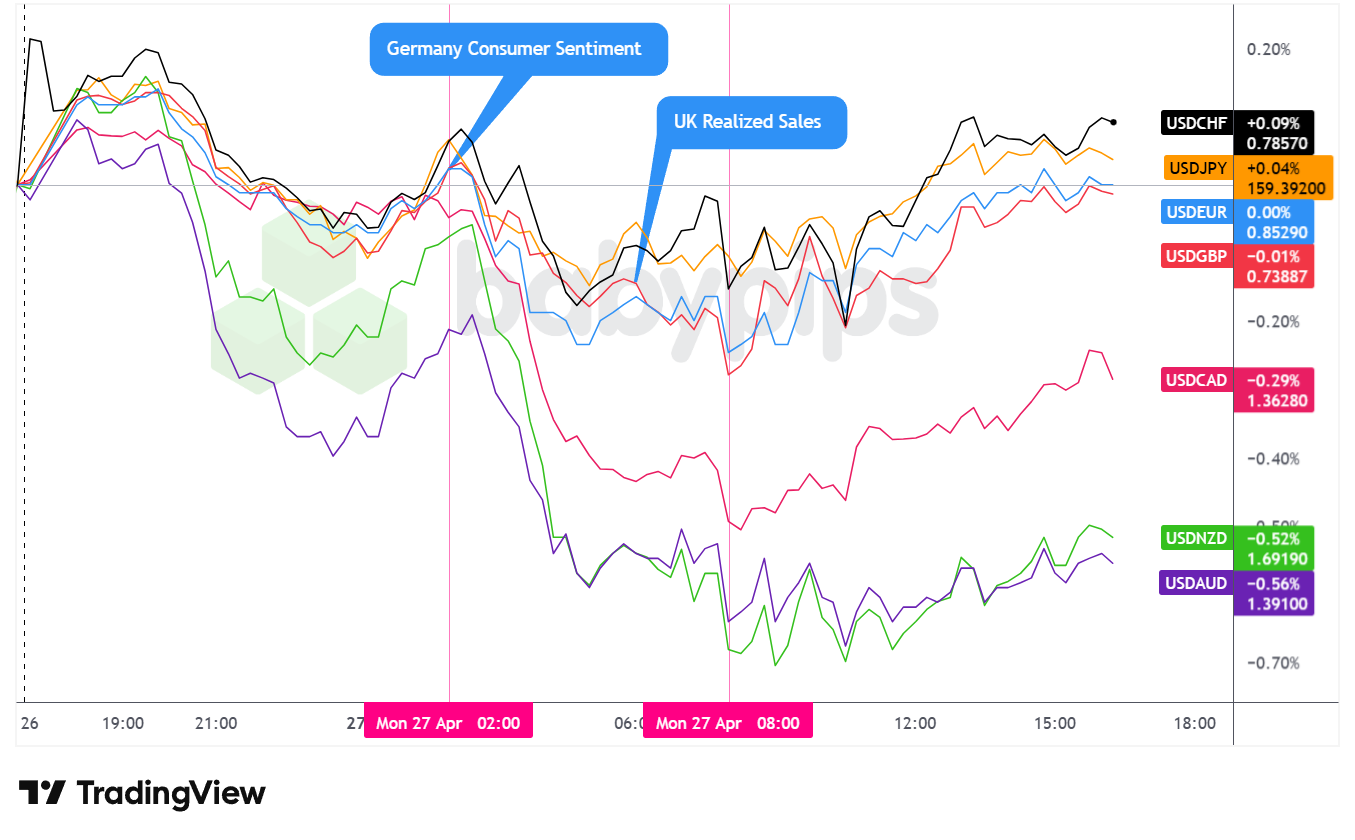

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar closed Monday mixed against the major currencies but arguably net negative on the day, with the most pronounced weakness against the commodity-linked currencies and broadly stable performance against the European pairs and yen.

During the Asian session, the dollar opened with a brief bounce, possibly reflecting some initial safe-haven demand following the weekend’s unsettling geopolitical developments, including Trump’s cancelled envoy trip to Islamabad and Iran’s continued Hormuz closure. However, the greenback quickly found a ceiling and reversed lower, pressing into net negative territory ahead of the London open, as early risk appetite improved on reports of the Iranian diplomatic proposal and stabilizing equity index futures.

The London session brought continued bearish pressure on the dollar. Two notable misses from European data landed during the session. Germany’s GfK consumer sentiment for May printed at -33.3, well below the -30.0 forecast and a marked deterioration from the prior -28.0 reading. The U.K. CBI Distributive Trades survey for April came in at -68.0 against a -47.0 forecast, a significant downside miss that pointed to sharp pressure on retail conditions. Despite the weak European readings, the dollar failed to find meaningful support, suggesting broader greenback softness was the dominant driver rather than any compelling relative macro story. The dollar gradually stabilized through the latter portion of the London session ahead of the New York open.

The U.S. session saw the dollar reverse course and trade net higher against most major currencies through the afternoon. The Dallas Fed Manufacturing Index for April came in at -2.3, below the -0.8 forecast and a further deterioration from the prior -0.2 reading, pointing to softening conditions in Texas manufacturing. However, the data did not appear to derail the dollar’s intraday recovery. The greenback’s firming through the U.S. afternoon possibly reflected broad pre-positioning ahead of a dense week of central bank decisions, with the Federal Reserve, European Central Bank, Bank of Japan, Bank of England, and Bank of Canada all scheduled to set policy rates.

At Monday’s close, the dollar posted modest gains against the Swiss franc (+0.09%) and Japanese yen (+0.04%), was essentially flat against the euro (0.00%), and showed slight losses against the pound (-0.01%). The sharpest losses came against the commodity-linked currencies, with the dollar falling approximately 0.29% against the Canadian dollar, 0.52% against the New Zealand dollar, and 0.56% against the Australian dollar. The relative outperformance of AUD, NZD, and CAD likely reflects commodity-linked tailwinds from elevated oil prices, and in Canada’s case the domestic news of the newly announced $25 billion sovereign wealth fund may have provided additional support for CAD. Overall, the greenback ended the session in mixed but arguably net negative territory, with cautious positioning ahead of a consequential week for global monetary policy the likely backdrop.

Upcoming Potential Catalysts on the Economic Calendar

- U.K. BRC Shop Price Inflation for April 2026 at 11:01 pm GMT

- Japan Unemployment Rate for March 2026 at 11:30 pm GMT

- Bank of Japan Governor Ueda Speech

- Bank of Japan Interest Rate Decision for April 28, 2026 at 3:00 am GMT

- ECB Consumer Inflation Expectations for March 2026 at 9:00 am GMT

- New Zealand Global Dairy Trade Price Index for April 28, 2026

- U.S. S&P/Case-Shiller Home Price for February 2026 at 1:00 pm GMT

- U.S. House Price Index for February 2026 at 1:00 pm GMT

- Richmond Fed Manufacturing Index for April 2026 at 2:00 pm GMT

- CB U.S. Consumer Confidence for April 2026 at 2:00 pm GMT

- U.S. Dallas Fed Services Index for April 2026 at 2:30 pm GMT

- U.S. Money Supply for March 2026 at 5:00 pm GMT

- ECB President Lagarde Speech at 6:30 pm GMT

Tuesday’s calendar opens overnight with the Bank of Japan rate decision, and Governor Ueda’s press conference is likely to draw considerable attention given the yen is hovering near 159 against the dollar and traders will be watching closely for any shift in tone on the pace of policy normalization.

In Europe, ECB Consumer Inflation Expectations and an address from President Lagarde in the evening could provide early signals ahead of the ECB’s own rate decision later this week.

Stateside, the CB Consumer Confidence reading for April will be closely monitored as one of the first broad gauges of how U.S. consumers are absorbing higher energy costs from the ongoing oil supply disruption. Any fresh developments on the Iran diplomatic front remain the wildcard capable of moving oil, gold, and risk sentiment sharply in either direction.

Stay frosty out there, forex friends!

Promotion: When the Market Swings, Are You Reacting or Executing?

In “Positive Trading Psychology,” renowned psychologist Brett Steenbarger reveals in his newest book that the secret to navigating volatility like we’ve been seeing isn’t to “fix” your flaws—it’s doubling down on your innate character strengths. Learn how to stay clinical while the rest of the market is emotional, turning Wednesday’s geopolitical uncertainty into your professional edge.

Learn more about “Positive Trading Psychology: Turning personal strengths into trading strengths” on Amazon!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.