Wednesday was one of those sessions where the headline chaos and the market reaction told two very different stories. Iran seized more ships in the Strait of Hormuz, ceasefire talks stalled, and both sides dug in on the naval blockade standoff, yet stocks hit a fresh record, Bitcoin ripped over 4%, and oil climbed without spiraling. The key ingredient? Trump announced an indefinite ceasefire extension, pulling back from a Wednesday bombing deadline that markets had been eyeing all week.

Throw in a strong batch of Q1 earnings beating expectations, and risk appetite had all it needed to stage a comeback after two straight down days. The dollar found its footing too, grinding higher through the U.S. session after a shaky Asian start.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- President Trump extended the U.S.-Iran ceasefire indefinitely on Wednesday, stepping back from a deadline to resume bombing and signaling the move is intended to allow more time for diplomacy

- Iran’s IRGC seized the MSC Francesca and Epaminondes in the Strait of Hormuz attempting to leave the gulf

- API Crude Oil Stock Change for April 17, 2026: -4.4M (6.1M previous)

- Japan Balance of Trade for March 2026: 667.0B (970.0B forecast; 57.3B previous)

- Australia Westpac Leading Index for March 2026: -0.1% m/m (0.2% m/m forecast; -0.1% m/m previous)

- U.K. CPI Growth Rate for March 2026: 0.7% m/m (0.8% m/m forecast; 0.4% m/m previous); 3.3% y/y (3.4% y/y forecast; 3.0% y/y previous)

- U.S. MBA 30-Year Mortgage Rate for April 17, 2026: 6.35% (6.42% previous)

- U.S. MBA Mortgage Applications for April 17, 2026: 7.9% (1.8% previous)

- Canada New Housing Price Index for March 2026: -0.2% m/m (0.1% m/m forecast; 0.3% m/m previous)

- Euro area Consumer Confidence Flash for April 2026: -20.6 (-17.9 forecast; -16.3 previous)

- EIA Crude Oil Stocks Change for April 17, 2026: 1.93M (-0.91M previous)

- European Central Bank Chief Economist Philip Lane said on Wednesday that the effect of the Iran war on the Euro area economy is still unclear.

Promoted: Day traders & Scalpers have better odds of making great decisions if they see market catalysts right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

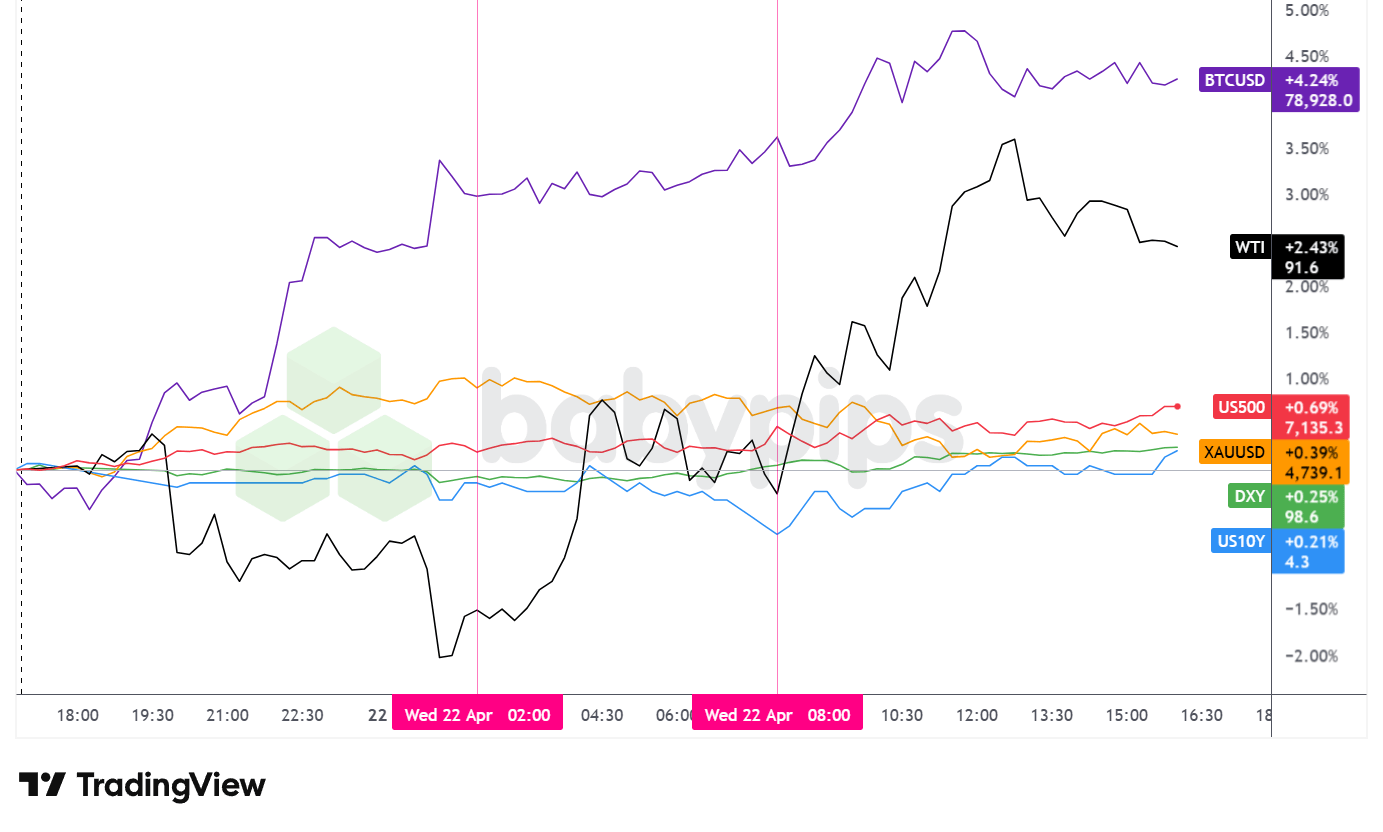

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Wednesday’s session was shaped by two dominant forces: President Trump’s decision to extend the Iran ceasefire indefinitely, which removed the near-term threat of renewed U.S. bombing, and a wave of strong first-quarter corporate earnings that helped carry U.S. equities to fresh record levels. Broad risk appetite was arguably the theme of the day, with Bitcoin and oil both posting the largest gains among major assets tracked in this recap.

Bitcoin was the session’s standout performer, advancing approximately 4.18% to close near $78,877. The cryptocurrency climbed steadily from around $75,400 during the Tuesday evening U.S. session and continued higher through the Asian and London sessions, pushing above the $78,000-$78,400 area following the U.S. open and consolidating near session highs into the close. No direct Bitcoin-specific catalyst was apparent for the move; the advance may reflect the broader risk-on shift following the ceasefire extension and strong corporate earnings flow, though the specific drivers remain speculative without additional sourcing.

WTI crude oil posted gains of approximately 2.45%, closing near $91.61 per barrel. The session was notably volatile for oil: prices slipped from around $89.30 during the prior U.S. evening session to a low near $87.73 ahead of the London open, before staging a sharp recovery through European and into U.S. hours. The session high came in near $92.72, with prices easing modestly into the close. The advance coincided with continued Strait of Hormuz disruptions, including Iran’s IRGC seizure of the MSC Francesca and Epaminondas and reported attacks on a third vessel. Notably, the EIA crude inventory report showed a surprise build of 1.93 million barrels versus a prior draw of 0.91 million barrels, which ordinarily could weigh on prices; however, this did not appear to meaningfully cap oil’s advance on the day, possibly as geopolitical supply-disruption concerns remained the more dominant near-term factor.

The S&P 500 climbed approximately 0.66% to close near 7,133, touching an intraday high of approximately 7,138. The index started near the 7,087 area and broadly trended higher throughout the session. Bloomberg reported the advance was driven by strong first-quarter earnings, with roughly 81% of S&P 500 companies reporting results having beaten analyst estimates, and notable contributions from Boeing and Philip Morris International. Bloomberg also reported that chipmakers extended their winning streak for a 16th consecutive session.

Gold ended approximately 0.39% higher at around $4,737.80, though the session’s intraday arc told a more complex story than the net gain suggests. The precious metal rallied sharply from around $4,716 during the Asian session to a high near $4,772 through the London session, before steadily pulling back through U.S. hours to close well below the day’s peak. The pullback may reflect some profit-taking as risk appetite strengthened on the ceasefire extension, though ongoing Hormuz uncertainty appeared to limit any larger reversal.

U.S. 10-year Treasury yields closed near 4.294%, reflecting a modest intraday decline of approximately 0.9 basis points per the individual yield chart. Yields were volatile during the session, posting a high above 4.30% early before dropping to a low near 4.262% during European hours, then recovering through the U.S. session without fully retracing the earlier move.

Promoted: Pay Once. Trade Forever.

Most prop firms quietly drain your account with monthly subscription fees long before you ever see a payout. Tradeify operates differently — evaluations are a one-time purchase with no recurring charges. Pass the eval, get activated instantly, and keep more of what you earn. With ~$150M in verified payouts and growing, the math speaks for itself.

Learn More About Tradeify!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

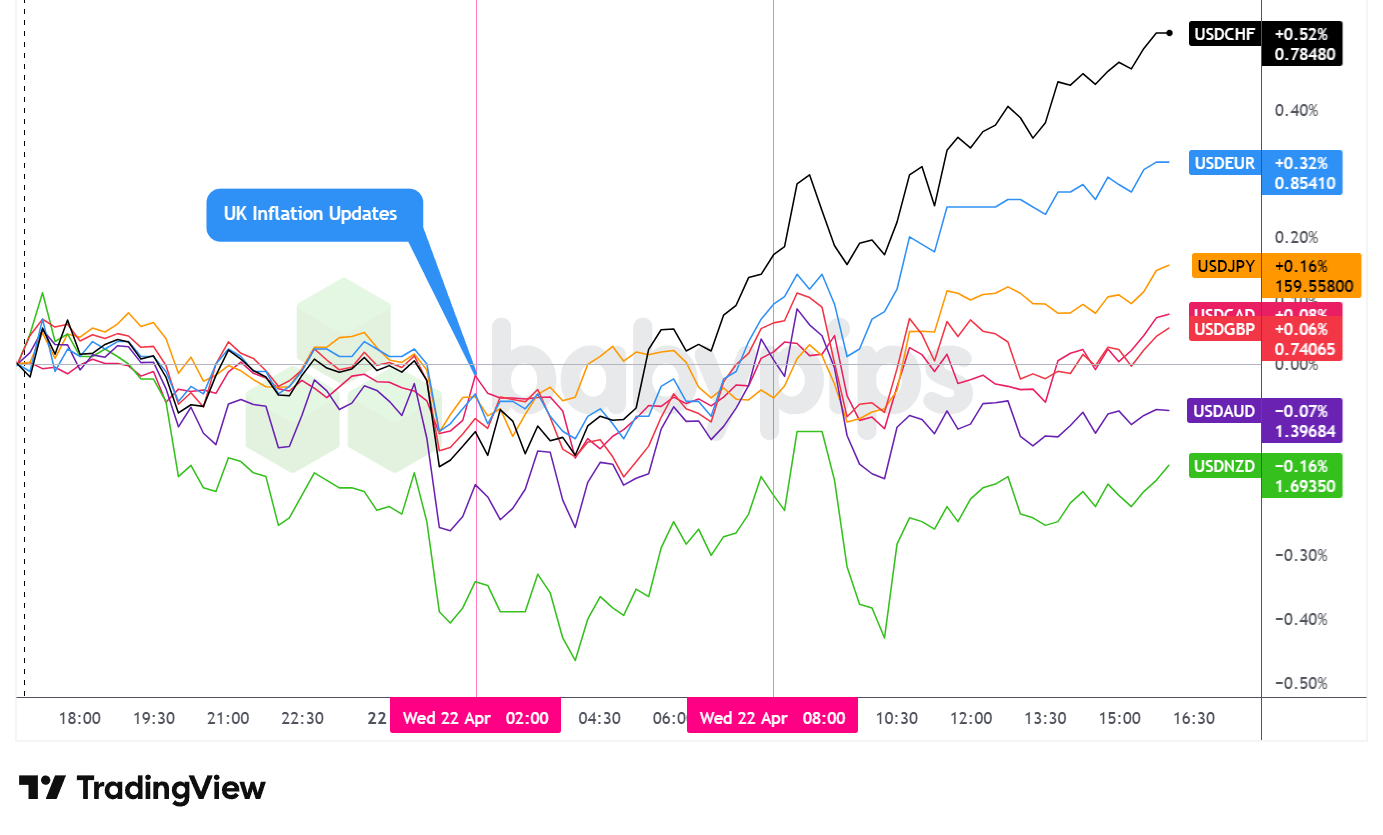

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar navigated a choppy session on Wednesday, ultimately closing with a net bullish lean against most major currencies despite a weak start during Asian hours. By the close, the dollar posted its largest gains against the Swiss franc (+0.52%) and euro (+0.32%), while seeing marginal losses against the Australian dollar (-0.07%) and New Zealand dollar (-0.16%).

During the Asian session, the dollar traded net lower against the major currencies, with the weakness most evident in the run-up to the London session open. The move lower coincided with continued geopolitical uncertainty around the Strait of Hormuz, though no single clear catalyst fully accounts for the directional shift without additional sourcing.

The London session brought initially choppy price action in the dollar against the major currencies. The U.K. CPI release, which showed headline inflation at 3.3% year-on-year (slightly below the 3.4% forecast) and core CPI at 3.1% year-on-year (below the 3.2% expected), was the primary scheduled economic catalyst of the session. The softer-than-expected readings may have limited near-term Bank of England hawkish repricing, though the immediate FX reaction was contained, with GBP ending only marginally lower against the dollar on the day (+0.06% in USDGBP terms). Following the initial choppy phase, the dollar developed a bullish lean heading into the U.S. session open, a shift that coincided with a Bloomberg report that Iran had received “some sign” the U.S. was ready to lift the naval blockade, which may have provided a modest positive risk tone that contributed to some safe-haven currency unwinding.

After the U.S. session open, the dollar dipped briefly against the major currencies before quickly stabilizing and rebounding. From the London close onward, the greenback held a broadly bullish bias through the remainder of the session, with no major scheduled U.S. economic data releases to drive a clear directional catalyst. The continuation of the bullish trend may reflect a combination of improved risk sentiment alongside possible position adjustment as the session wound down.

Upcoming Potential Catalysts on the Economic Calendar

- Australia S&P Global Manufacturing & Services PMI Flash for April 2026 at 11:00 pm GMT

- Japan S&P Global Manufacturing & Services PMI Flash for April 2026 at 12:30 am GMT

- New Zealand Credit Card Spending for March 2026 at 3:00 am GMT

- U.K. Public Sector Net Borrowing Ex Banks for March 2026 at 6:00 am GMT

- France Business Confidence for April 2026 at 6:45 am GMT

- Euro area S&P Global Manufacturing & Services PMI Flash for April 2026 at 8:00 am GMT

- U.K. S&P Global Manufacturing & Services PMI Flash for April 2026 at 8:30 am GMT

- U.K. CBI Business Optimism Index & Industrial Trends Orders for June 30, 2026 at 10:00 am GMT

- Canada Manufacturing Sales Prel for March 2026 at 12:30 pm GMT

- Canada PPI for March 2026 at 12:30 pm GMT

- U.S. Initial Jobless Claims for April 18, 2026 at 12:30 pm GMT

- U.S. Chicago Fed National Activity Index for March 2026 at 12:30 pm GMT

- U.S. S&P Global Manufacturing & Services PMI Flash for April 2026 at 1:45 pm GMT

- U.S. Kansas Fed Manufacturing Index for April 2026 at 3:00 pm GMT

Thursday’s calendar is front-loaded with flash PMI readings overnight from Australia and Japan, followed by European and U.K. PMIs that could offer the first broad look at how manufacturing and services activity is holding up amid sustained Hormuz supply disruptions. The U.S. session brings initial jobless claims alongside the flash U.S. PMIs, which markets may watch for early signs of any economic softening linked to elevated energy prices. Any fresh developments in the Iran-U.S. ceasefire talks, particularly around the naval blockade, are likely to continue serving as a key backdrop driver across all sessions.

Stay frosty out there, forex friends!

Promotion: When the Market Swings, Are You Reacting or Executing?

In “Positive Trading Psychology,” renowned psychologist Brett Steenbarger reveals in his newest book that the secret to navigating volatility like we’ve been seeing isn’t to “fix” your flaws—it’s doubling down on your innate character strengths. Learn how to stay clinical while the rest of the market is emotional, turning Wednesday’s geopolitical uncertainty into your professional edge.

Learn more about “Positive Trading Psychology: Turning personal strengths into trading strengths” on Amazon!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.