Monday’s session was dominated by geopolitical risk as escalating U.S.-Iran tensions and mounting doubts over peace talks in Pakistan sent oil sharply higher, snapped a five-day winning streak for U.S. equities, and contributed to broad-based U.S. dollar weakness by the close of trade.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Over the weekend, the U.S. Navy seized an Iranian-flagged vessel in the Gulf of Oman after it allegedly breached the naval blockade, with Iran calling the action “armed piracy” and threatening retaliation. President Trump warned the ceasefire expires Wednesday and that an extension is “highly unlikely.”

- Iranian officials said that Tehran had no current plans to attend fresh negotiations in Pakistan even as a U.S. delegation led by Vice President Vance prepared to fly to Islamabad.

- The strait remained effectively closed to most commercial shipping on Monday, sustaining the global energy supply crisis that has been building since U.S. and Israeli strikes on Iran began in late February.

- New Zealand Balance of Trade for March 2026: 0.7B (0.27B forecast; -0.26B previous)

- Japan Tertiary Industry Activity Index for February 2026: -0.4% (9.6% forecast; 1.7% previous)

- Germany PPI for March 2026: 2.5% m/m (0.8% m/m forecast; -0.5% m/m previous); -0.2% y/y (-1.8% y/y forecast; -3.3% y/y previous)

- Canada CPI Growth Rate for March 2026: 0.9% m/m (1.0% m/m forecast; 0.5% m/m previous); 2.4% y/y (2.5% y/y forecast; 1.8% y/y previous)

- The Bank of Canada’s first-quarter 2026 Survey of Consumer Expectations: trade tensions are weighing a little less on consumers, with the overall indicator edging up from recent lows and spending plans improving slightly. At the same time, high prices and broader economic uncertainty are still holding back households, and near-term inflation expectations remain elevated

- The Bank of Canada’s first‑quarter 2026 Business Outlook Survey showed that business sentiment improved slightly from last quarter, with firms expecting modest gains in sales growth and a smaller share of businesses now budgeting for a recession, as trade‑tension drag eases and public spending supports demand.

- Chinese President Xi Jinping called Saudi Arabia’s Crown Prince Mohammed bin Salman, stating that normal passage through the Strait of Hormuz should be maintained and calling for an immediate and comprehensive ceasefire

Promoted: Day traders & Scalpers have better odds of making great decisions if they see market catalysts right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

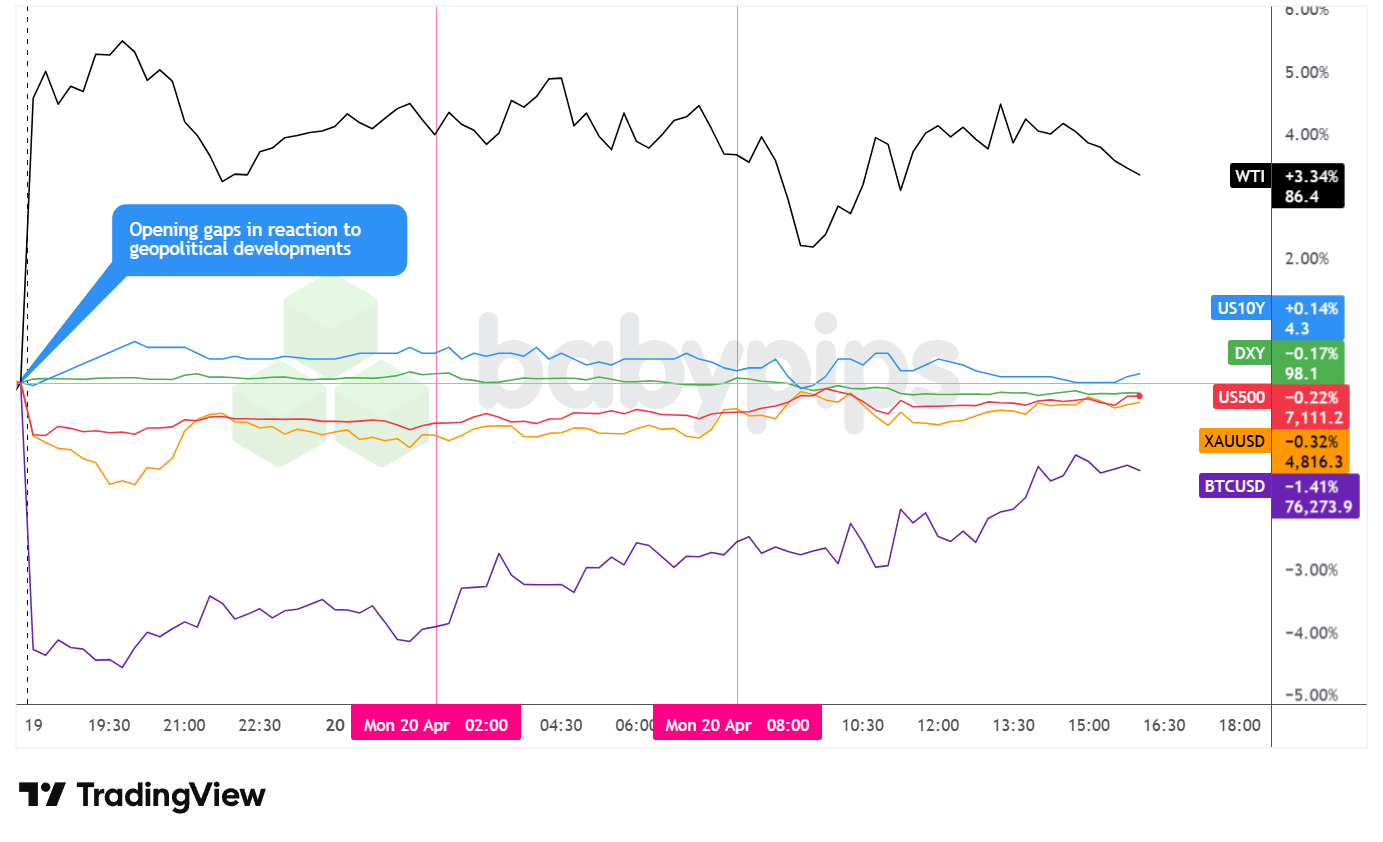

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Monday’s broad market session was defined by a sharp opening gap in oil prices, a partial but ultimately contained retreat in equities from record highs, and a notable divergence between traditional safe havens and risk assets as traders assessed the uncertain geopolitical backdrop.

WTI crude oil was the session’s standout performer, gaining approximately 3.77% to close near $86.49 per barrel. The move traced directly to the weekend’s geopolitical developments: the U.S. Navy’s seizure of the Iranian cargo vessel Touska, Iran’s reversal on reopening the Strait of Hormuz, and President Trump’s comments effectively ruling out a ceasefire extension. WTI gapped sharply higher at Sunday’s market open, possibly reflecting accumulated weekend headlines, and while the move faded somewhat through the session, the 13:30 area saw another leg of selling that briefly pushed prices toward the $85.14 support region before recovering. Brent crude was reported hovering near $95 per barrel as of mid-afternoon ET, with analysts flagging potential for further upside should the strait remain blocked.

Gold edged lower by approximately 0.26%, closing near $4,817 per ounce, in a session marked by sharp intraday swings rather than a clean directional move. The precious metal opened Sunday evening at elevated levels near $4,830, then sold off aggressively through the Asian session, dropping to lows near the $4,737-$4,750 area. A recovery through the London session saw gold retrace most of those losses, briefly touching the $4,827-$4,829 resistance zone near the U.S. open before fading again. The pullback from that intraday high left gold unable to hold its earlier levels, and it stabilized in the $4,792-$4,816 range through the U.S. afternoon. The volatile intraday pattern — a gap higher, a sharp drop, and a partial recovery — possibly reflected competing forces, with one interpretation being initial weekend safe-haven positioning giving way to profit-taking or margin-related selling, before prices stabilized.

The S&P 500 fell approximately 0.23%, closing near 7,110, halting a five-day advance. The index initially pushed higher after the U.S. open, reaching an intraday peak near 7,122-7,123 around 10:00-10:30 ET, before retreating as Trump’s escalatory ceasefire comments and reports of Iran’s hesitance to send negotiators to Pakistan weighed on sentiment. Tech heavyweights contributed to the drag. Despite the pullback, the index remained close to all-time high territory, which may suggest broader market conviction in the underlying economic backdrop remained relatively intact, though that interpretation is speculative.

After an opening drop, Bitcoin climbed steadily to close near $76,340. There were no direct Bitcoin-specific catalysts to point to, so one possible explanation is bears unloading short positions as geopolitical fears waned, or another could be a demand for alternative stores of value and/or technical momentum following intraday session lows in the $73,800-$74,000 area.

The U.S. 10-year Treasury yield closed near 4.252%, essentially flat on the day. Yields opened the session at elevated levels in the 4.28-4.29% range and drifted gradually lower through trade, a move that possibly reflected modest safe-haven demand in bonds, though the scale of that demand appeared limited given the overall geopolitical backdrop.

Promotion: If your confidence has grown in your market awareness & strategies with this market recap, and you wanna take action, Maven Trading can help. They provide simulated funding challenges starting as low as $13, allowing you to trade major pairs with professional-sized capital. No time limits mean you can take swing plays on these market themes without the pressure of a ticking clock.

Learn More About Maven Trading Today!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

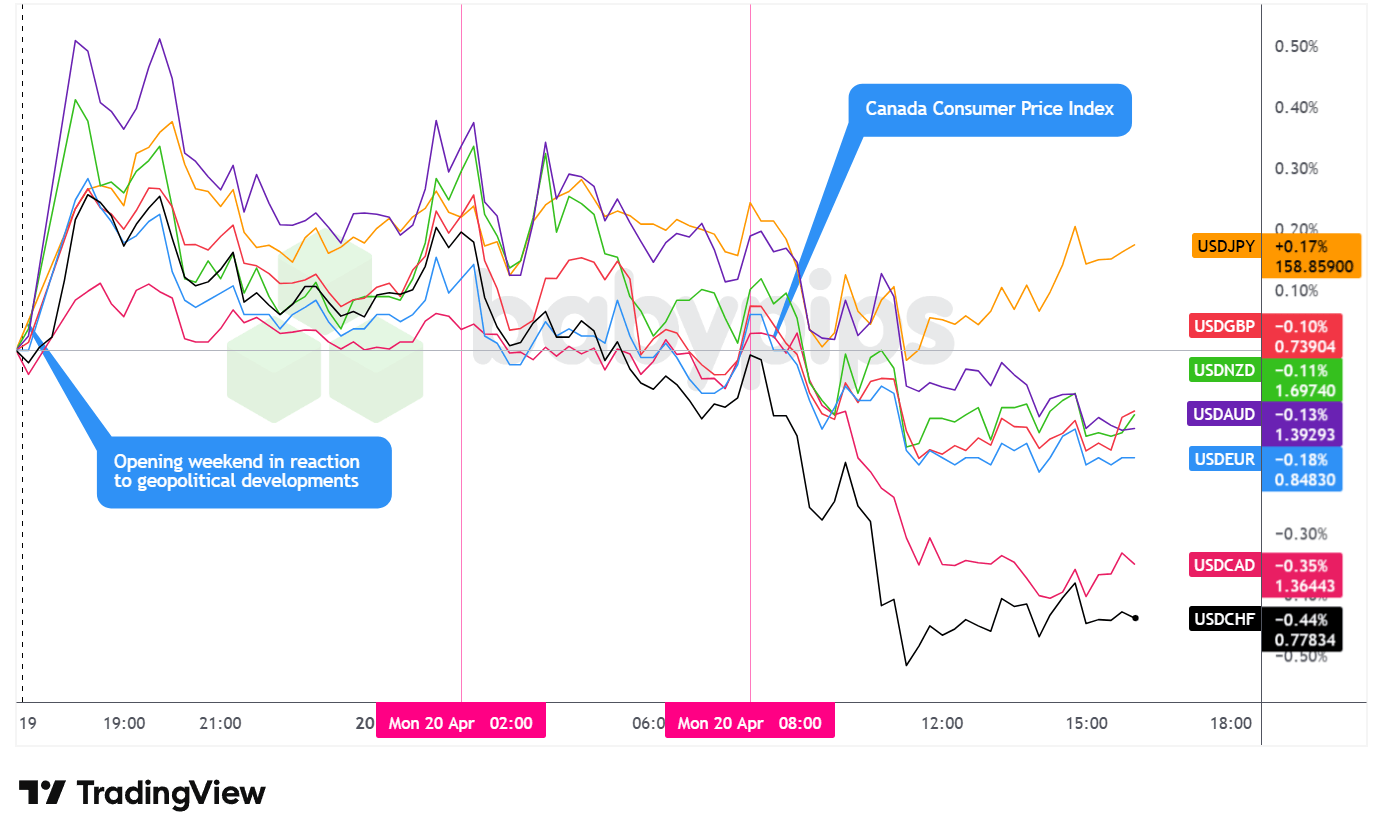

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar opened Monday with a sharp spike higher in reaction to the weekend’s geopolitical developments but quickly reversed course, ultimately closing as one of the weakest performers among the major currencies on the day, posting a gain only against the Japanese yen.

During the Asian session, the dollar traded with a net bullish lean against most major currencies. The initial spike appeared consistent with a flight-to-safety impulse following the accumulated weekend headlines on U.S.-Iran tensions, the Touska seizure, and Iran’s renewed Hormuz restrictions. However, the move faded relatively quickly and the greenback maintained only a mild positive bias into the London open rather than extending those initial gains.

The London session marked the turning point for the dollar. From the London open through the European close, the greenback traded net lower against most major currencies, possibly as risk sentiment partially stabilized, though it is also worth noting that broader dollar-negative positioning may have been a contributing factor independent of geopolitical developments. Canada’s Consumer Price Index data, annotated on the USD vs. Majors overlay chart as a catalyst near the U.S. session open, appeared to have contributed to notable Canadian dollar strength: USDCAD fell approximately 0.35% on the day to trade near 1.3644. The Swiss franc was the session’s standout gainer against the dollar, with USDCHF declining approximately 0.44% to trade near 0.7783, a move possibly consistent with typical CHF safe-haven demand during periods of elevated geopolitical risk.

The remaining U.S. session saw the dollar stabilize following the London-session losses, trading in a relatively narrow range for the remainder of the day. With no major U.S. economic data on the calendar, price action was primarily driven by geopolitical headlines surrounding the Iran negotiations and Trump’s public commentary on the ceasefire timeline.

At Monday’s close, the dollar posted a gain only against the Japanese yen, with USDJPY rising approximately 0.17% to near 158.86. One possible explanation for the yen’s underperformance is its well-documented sensitivity to oil prices: as a major energy importer, Japan is arguably more exposed than most to Hormuz-related supply disruptions, which may have weighed on yen demand in a session defined by sharp oil gains — though this interpretation is an educated guess in the absence of a direct catalyst.

Upcoming Potential Catalysts on the Economic Calendar

- New Zealand Business Confidence for March 31, 2026 at 10:00 pm GMT

- New Zealand CPI Growth Rate for March 31, 2026 at 10:45 pm GMT

- Swiss Balance of Trade for March 2026 at 6:00 am GMT

- U.K. Employment Situation Update for February 2026 at 6:00 am GMT

- ECB Guindos Speech at 7:00 am GMT

- Germany ZEW Economic Sentiment Index for April 2026 at 9:00 am GMT

- U.S. Retail Sales for March 2026 at 12:30 pm GMT

- New Zealand Global Dairy Trade Price Index for April 21, 2026

- U.S. Pending Home Sales for March 2026 at 2:00 pm GMT

- Fed Chair Nominee Kevin Warsh Confirmation Hearing at 2:00 pm GMT

- U.S. Fed Waller Speech at 6:30 pm GMT

- U.S. API Crude Oil Stock Change for April 17, 2026 at 8:30 pm GMT

Federal Reserve Chair nominee Kevin Warsh is scheduled to testify before the Senate Banking Committee at 10:00 AM ET. Prepared remarks viewed by Bloomberg indicate a commitment to monetary policy independence, with Warsh stating that “the conduct of monetary policy remains strictly independent.” Markets may closely watch the Q&A for any signals on his rate outlook and broader policy philosophy, though what specifically draws market attention will depend on how the hearing unfolds.

U.S. Retail Sales data for March 2026 is also due Tuesday. Analysts project a headline jump driven largely by increased gasoline spending, though the reading excluding gasoline and autos may signal more tepid underlying demand as elevated fuel costs pressure consumer discretionary budgets.

Beyond the scheduled data, markets will likely remain sensitive to any headlines from the U.S.-Iran talks in Pakistan, where Vice President Vance’s delegation was expected to arrive Tuesday. With Trump framing the ceasefire expiry as “Wednesday evening Washington time,” any signal of a deal, breakdown, or extension could plausibly move oil and risk-sensitive assets sharply, though the direction and magnitude would depend on the nature of any development.

Stay frosty out there, forex friends!

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

In “Unknown Market Wizards,” (⭐ 4.6★ | 1,400+ reviews on Amazon) Jack Schwager interviews successful traders to reveal a common truth: their edge isn’t just knowledge or skills—it’s their psychological resilience and rigid risk control. Whether you’re navigating shifting geopolitical themes or top tier economic data, learn how the “wizards” stay clinical when the rest of the market is emotional.

Master Your Trading Mindset with Market Wizards!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.