Markets maintained a cautious but broadly risk-on posture on Thursday as the S&P 500 extended its winning streak to seven consecutive sessions, even as mounting doubts about the durability of the U.S.-Iran ceasefire kept investor confidence fragile.

A dense U.S. morning data slate reinforced stagflationary concerns, with core PCE printing hotter than expected and final Q4 2025 GDP revised sharply lower, weighing on the dollar broadly while gold and equities found support in residual ceasefire optimism and hopes for productive weekend peace talks in Pakistan.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- U.S. API Crude Oil Stock Change for April 3, 2026: 3.72M (10.26M previous)

- Japan Average Cash Earnings for February 2026: 3.3% y/y (2.5% y/y forecast; 3.0% y/y previous)

- Japan Consumer Confidence for March 2026: 33.3 (38.0 forecast; 40.0 previous)

- Germany Balance of Trade for February 2026: 19.8B (19.1B forecast; 21.2B previous)

- Germany Industrial Production for February 2026: -0.3% m/m (0.2% m/m forecast; -0.5% m/m previous)

- Japan Machine Tool Orders for March 2026: 28.1% y/y (16.0% y/y forecast; 24.2% y/y previous)

- U.K. BBA Mortgage Rate for March 2026: 6.6% (6.6% forecast; 6.59% previous)

-

U.S. Core PCE Price Index for February 2026: 0.4% m/m (0.2% m/m forecast; 0.4% m/m previous)

- U.S. Personal Income for February 2026: -0.1% m/m (0.4% m/m forecast; 0.4% m/m previous)

- U.S. Personal Spending for February 2026: 0.5% m/m (0.6% m/m forecast; 0.4% m/m previous)

- U.S. GDP Growth Rate Final for December 31, 2025: 0.5% q/q (0.7% q/q forecast; 4.4% q/q previous)

- U.S. Initial Jobless Claims for April 4, 2026: 219.0k (215.0k forecast; 202.0k previous)

- President Trump warned of renewed U.S. military strikes against Iran if ceasefire negotiations fail, and vowed the Strait of Hormuz must stay open; Israel’s Netanyahu agreed to direct talks with Lebanon on disarming Hezbollah

- The Strait of Hormuz remains effectively closed to commercial oil and gas tankers, with only four vessels transiting post-ceasefire and none carrying oil or gas.

Promotion: Use TradeZella’s AI Powered trade journal to deep-dive into your execution and see exactly how you performed during today’s trading session.

Click here to get the TradeZella Edge and use code PIPS20 to save 20% on your first purchase!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

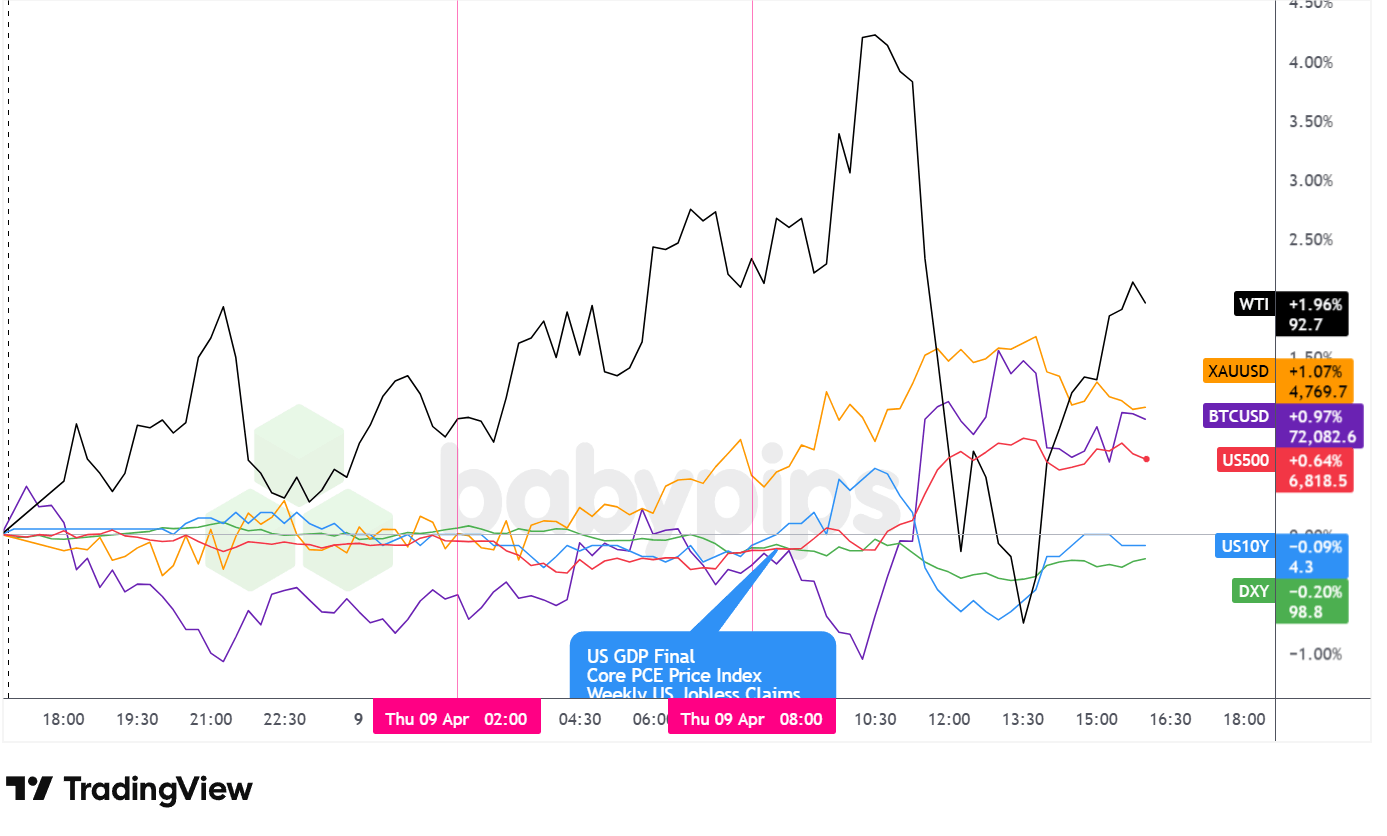

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Thursday’s session delivered a study in competing forces. Ceasefire optimism provided a floor for risk assets broadly, but persistent geopolitical uncertainty and an increasingly stagflationary U.S. data backdrop kept price action volatile, most vividly in oil markets where a dramatic intraday reversal underscored just how sensitive energy prices remain to any news concerning the Strait of Hormuz.

WTI crude oil was the session’s most volatile asset. Prices climbed steadily through the Asian and London sessions, reaching a session high near $95.10 around 10:30 a.m. ET, before reversing abruptly and plunging to a session low near $89.84, a peak-to-trough swing of roughly $5.25. Prices then recovered through the afternoon to close near $92.7, up approximately 1.96% on the day. The whipsaw appeared to reflect the tug-of-war between residual ceasefire optimism and the stubborn reality that the Strait of Hormuz remained effectively closed, with Iran’s leadership continuing to contest the terms of the deal throughout the session.

Gold traded with a sustained bullish bias throughout the day, recovering from an early dip to lows near $4,699-$4,705 in the overnight Asian session and climbing steadily through the London and early U.S. hours to peak near $4,801 around midday. Prices pulled back modestly into the close, settling near $4,769.7, up approximately 1.07% on the day. The metal’s strength appeared consistent with ongoing geopolitical uncertainty and the stagflationary macro backdrop, though no specific catalyst for the midday peak and subsequent pullback was immediately apparent.

The S&P 500 extended its winning streak to seven consecutive sessions, the longest run since October. The index traded softly through Asian and early London hours, dipping into the 6,752-6,764 area, before the 8:30 a.m. ET data releases appeared to spark a sharp rally that drove the index to a session high near 6,835 around midday. Equities held most of those gains into the close, settling near 6,818.5, up approximately 0.64% on the day. The advance came despite the stagflationary data signals, suggesting market focus remained primarily on ceasefire durability and the prospect of meaningful progress in weekend peace talks.

Bitcoin declined from near $71,800 just after the prior close to session lows around $70,468-$70,522 during Asian hours before trading choppy through the London session. U.S. morning session risk-on vibes pushed BTC higher, with prices touching near $72,561 before settling back to close near $72,082.6, up approximately 0.97% on the day.

U.S. 10-year Treasury yields traded in a relatively tight range of approximately 4.264-4.320, with a notable spike higher at the 8:30 a.m. ET data release before reversing sharply to session lows near 4.264. Yields recovered partially into the close, settling near 4.3, down approximately 0.09% from the prior close. The initial spike likely reflected the hotter-than-expected core PCE reading, while the subsequent reversal toward the session’s lows appeared to reflect the weaker growth and income signals embedded in the broader data package.

Promoted: Seven Sessions. One Direction. Are You Scaling?

The S&P 500 just posted its longest winning streak since October. If you’ve been on the right side of this ceasefire-driven risk rally and your journal shows it, your edge is already documented. The only thing missing is the capital to match it. Tradeify’s Lightning accounts offer instant funding with no evaluation phase — so you can trade the next catalyst, Friday’s CPI, at the size your results deserve.

Get Instant Funding with Tradeify!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

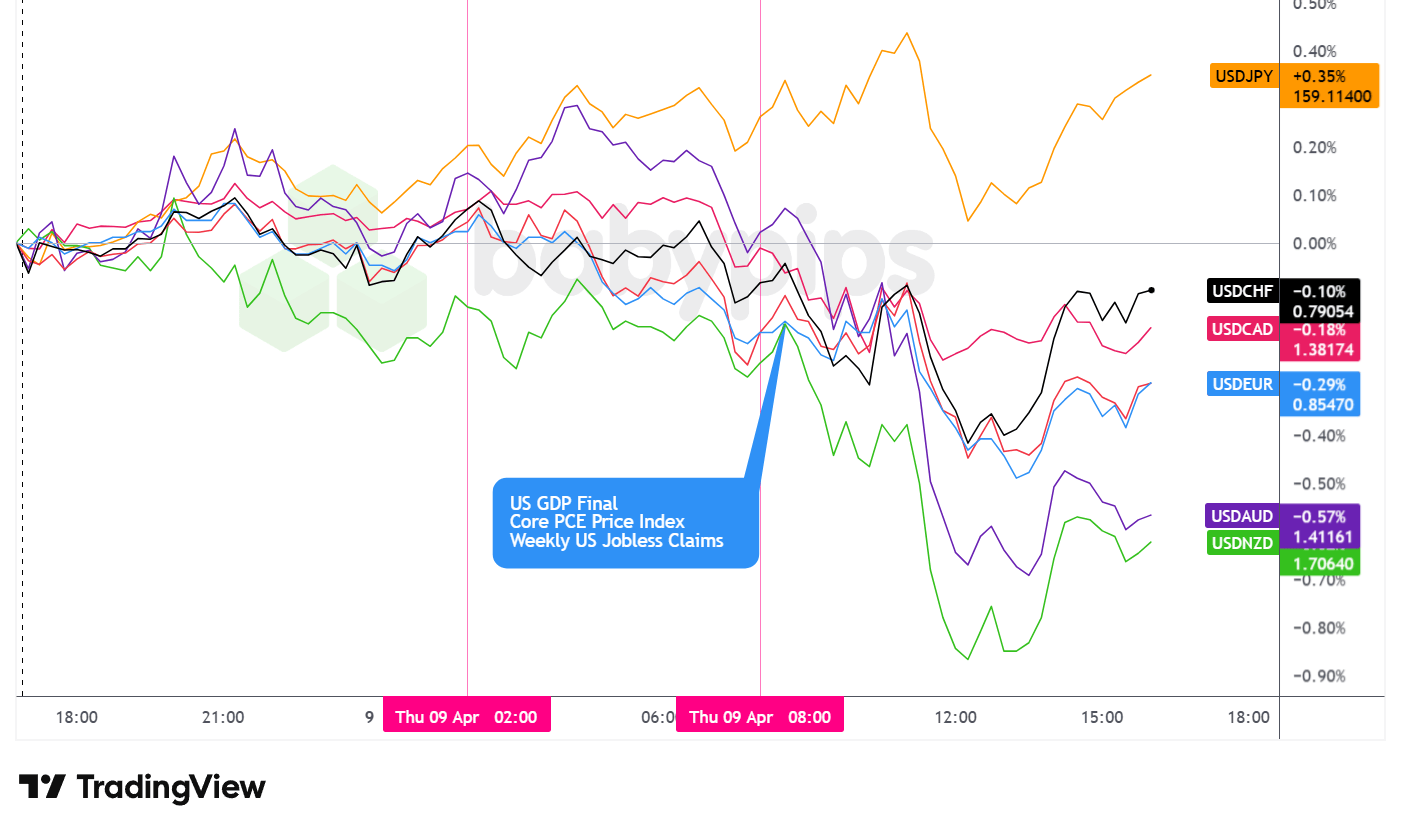

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar closed Thursday as one of the worst-performing major currencies, posting losses against all tracked majors with the sole exception of the Japanese yen.

During the Asian session, the U.S. dollar traded choppy and sideways, arguably with a slight bullish bias. The overnight backdrop was characterized by cautious FX positioning as market participants weighed the fragile and increasingly contested ceasefire situation. BOJ Governor Ueda’s reiteration that Japanese financial conditions remain accommodative weighed on yen sentiment through Asian hours, likely providing modest support to USD/JPY and contributing to the dollar’s slight positive lean during the session.

During the London session, the U.S. dollar continued to trade mixed, but arguably with an increasing bearish bias heading into the U.S. session. European data flows reinforced the cautious backdrop: German industrial production for February contracted 0.3% month-on-month, missing the consensus expectation for a 0.2% gain, while Japan’s consumer confidence index for March plunged to 33.3 from 40.0 in February and well below the 38.0 forecast, reflecting the toll of the ongoing U.S.-Iran conflict on household sentiment. The dollar’s gradual weakening through London hours suggested positioning ahead of the dense U.S. data slate may have been the dominant driver of FX flows during the European session.

After the U.S. session opened, the U.S. dollar saw bearish pressure lasting until roughly 12 p.m. Eastern Time, where it stabilized and rebounded slightly heading into the end of the day.

The 8:30 a.m. ET data cluster delivered a stagflationary verdict for February: the core PCE price index came in at 0.4% month-on-month, double the 0.2% consensus forecast, while the final Q4 2025 GDP growth rate was revised down to a 0.5% annualized pace from the initial 0.7% estimate and sharply below the 4.4% rate posted in Q3 2025.

Personal income fell 0.1% month-on-month, a stark miss against the 0.4% gain expected, while real consumer spending for Q4 2025 was revised down to 1.9% from a 2.0% preliminary reading. Initial jobless claims for the week ending April 4 came in at 219k, slightly above the 215k forecast and above the prior reading of 202k.

The combination of sticky inflation, weakening growth, declining personal income, and softening labor conditions appeared to stoke stagflationary concerns, with traders seemingly pricing in a more constrained Federal Reserve, as any potential rate support for the economy risks further fanning the already elevated inflation driven by war-related energy costs.

Upcoming Potential Catalysts on the Economic Calendar

- New Zealand Business NZ PMI for March 2026 at 10:30 pm GMT

- Japan PPI for March 2026 at 11:50 pm GMT

- Japan Bank Lending for March 2026 at 11:50 pm GMT

- Australia Building Permits Final for February 2026 at 1:30 am GMT

- China Inflation updates for March 2026 at 1:30 am GMT

- Germany Inflation Rate Updates Final for March 2026 at 6:00 am GMT

- Swiss Consumer Confidence for March 2026 at 7:00 am GMT

- Euro area ECB Guindos Speech at 11:00 am GMT

- Canada Employment Situation Update for March 2026 at 12:30 pm GMT

- U.S. CPI for March 2026 at 12:30 pm GMT

- U.S. Factory Orders for February 2026 at 2:00 pm GMT

- University of Michigan Consumer Sentiment Index for April 2026 at 2:00 pm GMT

- U.S. Factory Orders for February 2026 at 2:00 pm GMT

Friday’s calendar is dominated by the U.S. Consumer Price Index report for March at 12:30 pm GMT (8:30 a.m. ET), arguably the most consequential data release of the week. Economists expect a sharp 0.9% month-on-month increase in headline CPI, which would mark the steepest single-month advance since 2022, driven primarily by the war-related surge in energy prices that pushed gasoline prices up by more than a dollar per gallon. Thursday’s hotter-than-expected core PCE reading for February suggests underlying inflation pressures were already elevated before the full pass-through of war-related energy costs shows up in the March CPI data. A print in line with or above expectations would likely reinforce stagflationary concerns and sharply compress the Federal Reserve’s perceived room to ease policy in support of a slowing economy.

Canada’s employment report for March, also at 12:30 pm GMT, will be closely watched for signals about labor market resilience against the backdrop of elevated global uncertainty, and could drive notable moves in the Canadian dollar.

The University of Michigan consumer sentiment index for April at 2:00 pm GMT will provide a timely gauge of how U.S. households are assessing the economic and geopolitical backdrop, particularly any shifts in near-term inflation expectations following the sharp run-up in energy costs.

Stay frosty out there, forex friends!

Promoted: The Hormuz Whipsaw Was a Textbook Setup. Did You See It Coming?

WTI swung nearly $5.25 from peak to trough today as ceasefire headlines collided with the reality that not a single oil tanker had cleared the Strait. Retail traders chased the spike. Professional FX and commodity desks were already positioned around the narrative. Brent Donnelly’s The Art of Currency Trading (⭐ 4.7★ | 500+ reviews on Amazon) is the field manual for reading exactly this kind of geopolitical price action — from headline to execution. If today’s volatility felt like noise, this book turns it into a signal.

Learn more about “The Art of Currency Trading” at Amazon

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.