Markets navigated a tense and headline-driven Tuesday as the U.S.-Iran conflict entered a potentially decisive phase, with American forces striking targets on Iran’s Kharg Island and President Trump’s self-imposed 8 p.m. ET ceasefire deadline rattling nerves across asset classes. A sharp late-session reversal in risk sentiment, driven by reports of Iran positively reviewing a peace proposal and Pakistan urging a two-week extension, allowed equities to claw back steep intraday losses while crude oil tumbled sharply from session highs.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Australia S&P Global Services PMI Final for March 2026: 46.3 (46.6 forecast; 52.8 previous)

- Japan Household Spending for February 2026: 1.5% m/m (3.0% m/m forecast; -2.5% m/m previous); -1.8% y/y (-0.4% y/y forecast; -1.0% y/y previous)

- Australia Household Spending for February 2026: 0.3% m/m (-0.2% m/m forecast; 0.3% m/m previous); 4.6% y/y (4.2% y/y forecast; 4.6% y/y previous)

- Australia ANZ-Indeed Job Ads for March 2026: -3.1% m/m (0.1% m/m forecast; 3.2% m/m previous)

- Japan Leading Economic Index Prel for February 2026: 112.4 (112.5 forecast; 112.1 previous)

- Euro area S&P Global Services PMI Final for March 2026: 50.2 (50.1 forecast; 51.9 previous)

- U.K. New Car Sales for March 2026: 6.6% y/y (1.5% y/y forecast; 7.2% y/y previous)

- U.K. S&P Global Services PMI Final for March 2026: 50.5 (51.2 forecast; 53.9 previous)

- U.S. ADP Employment Change Weekly for March 21, 2026: 26.0k (10.0k previous)

- U.S. Durable Goods Orders for February 2026: -1.4% m/m (-0.3% m/m forecast; -1.4% m/m previous)

- Canada Ivey PMI s.a for March 2026: 49.7 (51.0 forecast; 56.6 previous)

- New Zealand Global Dairy Trade Price Index for April 7, 2026: -3.4% (0.1% previous)

- U.S. Consumer Inflation Expectations for March 2026: 3.4% (3.7% forecast; 3.0% previous)

- U.S. Consumer Credit Change for February 2026: 9.48B (9.0B forecast; 8.05B previous)

- Wallstreet Journal reports that Iran’s Khorramabad airport was targeted by US-Israeli attack on Tuesday

- On Tuesday, the U.S. attacked Iran’s Kharg Island and U.S. President Donald Trump reiterated his threat to unleash a massive new bombing campaign

Promotion: Use TradeZella’s AI Powered trade journal to deep-dive into your execution and see exactly how you performed during today’s trading session.

Click here to get the TradeZella Edge and use code PIPS20 to save 20% on your first purchase!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

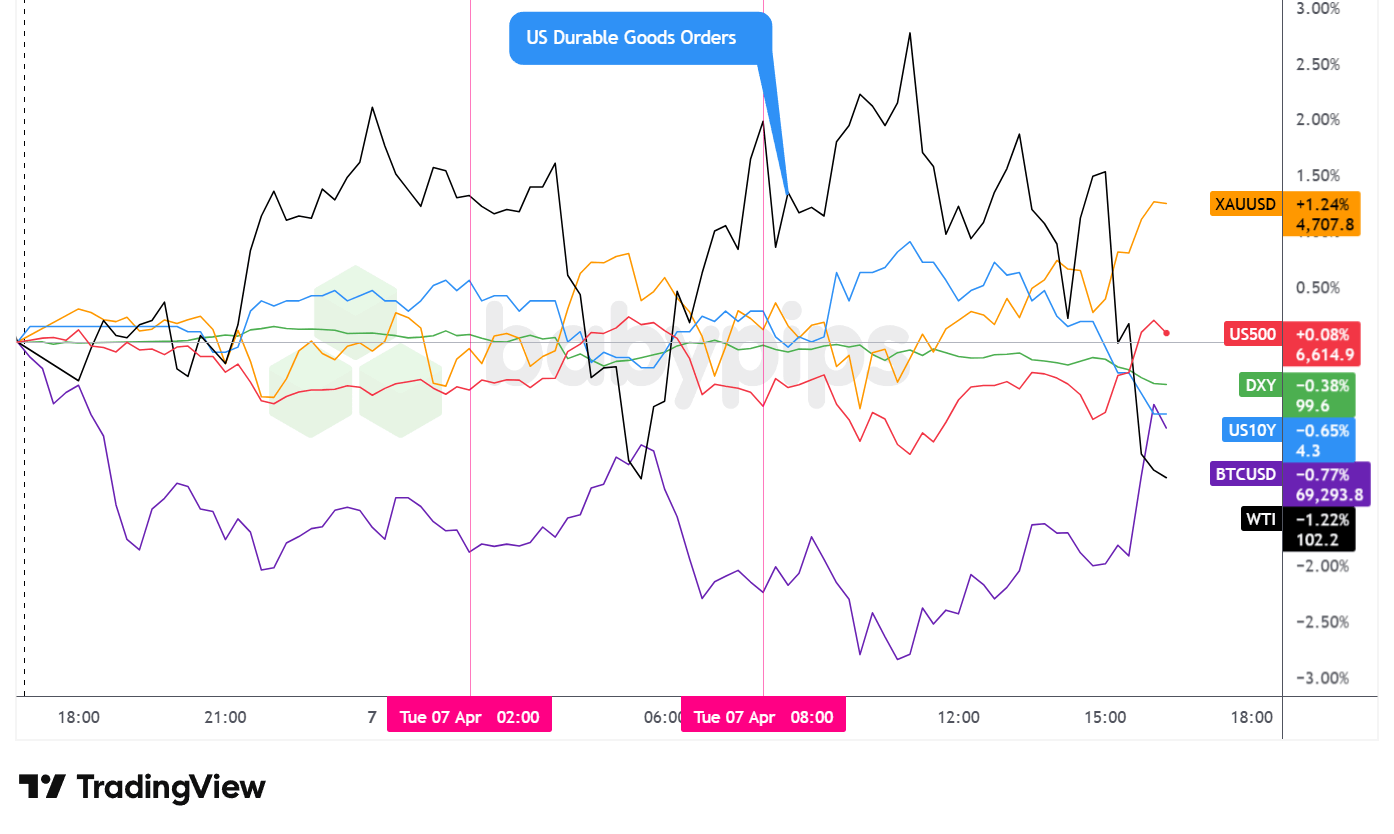

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Tuesday’s session was dominated almost entirely by geopolitical headline risk, with the U.S.-Iran conflict and President Trump’s 8 p.m. ET ceasefire deadline driving sharp, sentiment-driven swings across all major asset classes. Economic data took a secondary role, though a notably weak U.S. durable goods print contributed to the bearish undertone for risk and the dollar during the U.S. session.

Gold was the standout performer in a session tailor-made for safe-haven demand, advancing approximately 1.06% to settle near $4,708.50. The precious metal traded choppy and sideways through Asia and London, before catching a bid in U.S. trading. This late day move was likely supported by the conflict backdrop, rising near-term inflation expectations, and a softening dollar. Gold pushed to new session highs in the final hours of trading as uncertainty surrounding Trump’s deadline reached its peak.

WTI crude oil experienced the session’s most dramatic price action, whipsawing across a wide range before closing sharply lower. Oil had been trading in elevated volatility territory through most of the session, with prices eventually surging to intraday highs above $106 per barrel as the Trump deadline approached and reports of missile strikes on Saudi Arabia’s Jubail industrial hub added to supply disruption fears. The reversal came swiftly in the late U.S. afternoon as Pakistan proposed a two-week ceasefire extension and Reuters reported that Iran was positively reviewing the proposal. WTI ultimately settled near $101.08, a decline of approximately 2.31% on the session.

The S&P 500 endured a volatile journey before managing a modest gain on the day. Equities was under pressure early on, and sold off notably in early U.S. trading, with the index testing lows around the 6,534 area before diplomatic headlines triggered a swift recovery. The index closed near 6,624, up approximately 0.22%, with the late bounce appearing directly correlated with the ceasefire optimism headlines. Soft durable goods orders and cautious Fed commentary from Goolsbee and Williams likely contributed to the intraday weakness.

The 10-year U.S. Treasury yield declined approximately 0.60% to close near 4.31%, with the move likely reflecting a combination of flight-to-safety flows given the conflict environment and the softer economic data tone from the durable goods miss. The NY Fed’s consumer inflation expectations survey for March did rise to 3.4% from 3.0% previously, though it came in below the 3.7% forecast, suggesting the inflation expectations picture was less alarming than feared on the margin.

Bitcoin spent the day in the red, closing near $69,000 at the bell. With no notable crypto catalysts to point to, it looks like Bitcoin traded with broad risk sentiment flows, which were mostly net negative due to elevated geopolitical tensions and uncertainty ahead of the U.S. deadline for a deal with Iran.

Promoted: Capitalize on News Catalysts Without Risking Your Own Funds.

Iran rejected ceasefire talks. Trump threatened strikes by Tuesday. WTI whipsawed from $101–$106 and back — all in a single session.

On a small personal account, navigating that kind of volatility means trading position sizes too small to matter.Alpha Capital Group changes the math. By providing access to simulated funded accounts from $5K to $200K, starting at $50, you can execute high-conviction setups with the professional position sizing they deserve. Join 250K+ traders in 180+ countries today!

Learn more about Alpha Capital Group!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

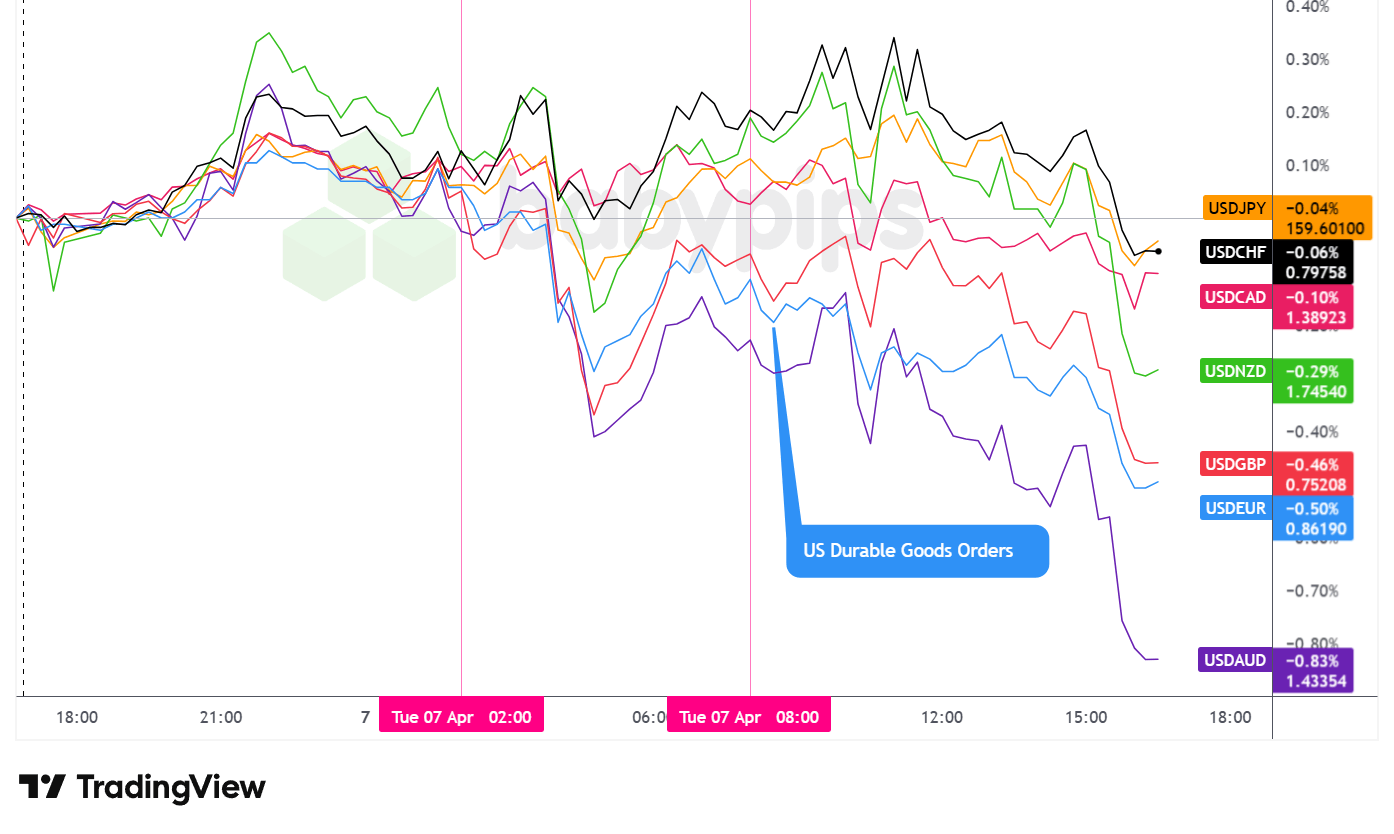

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar closed Tuesday as the worst-performing major currency on the day, with losses broadening through the U.S. session and the greenback finishing in the red against all seven majors tracked on the overlay chart.

During the Asian session, the dollar traded with a gradual bullish lean, slowly appreciating against the major currencies as geopolitical risk headlines intensified and traders likely positioned defensively ahead of the day’s uncertain catalyst load. However, the dollar’s advance capped out mid-session and began pulling back heading into the London open, suggesting the initial bid lacked the conviction needed to sustain gains.

After the London session opened, the U.S. dollar fell sharply against the major currencies, likely driven by a combination of European PMI data signaling further economic softness and the broader sense that escalating conflict risks were beginning to weigh on global growth expectations. The dollar quickly found a bottom and rebounded against the major currencies, stabilizing ahead of the U.S. session open as markets paused for direction.

During the Tuesday U.S. session, the U.S. dollar traded choppy and net lower against the major currencies. The February durable goods orders release, which came in at -1.4% month-over-month against a -0.3% forecast, appeared to correlate with an acceleration in dollar selling shortly after the 8:00 a.m. ET data drop, as annotated on the overlay chart. Cautious commentary from Fed’s Goolsbee, who described himself as “cautious slash nervous” about the economic impact of elevated oil prices and slowing business hiring, added to the dovish undertone for U.S. monetary policy. The late-session ceasefire optimism that boosted risk assets appeared to further weigh on the dollar as capital rotated into commodity-linked and risk-sensitive currencies.

Upcoming Potential Catalysts on the Economic Calendar

- U.S. API Crude Oil Stock Change for April 3, 2026 at 8:30 pm GMT

- U.S. Fed Jefferson Speech at 9:50 pm GMT

- Japan Current Account for February 2026 at 11:50 pm GMT

- New Zealand RBNZ Interest Rate Decision for April 8, 2026 at 2:00 am GMT

- Japan Eco Watchers Survey Outlook for March 2026 at 5:00 am GMT

- Germany Factory Orders for February 2026 at 6:00 am GMT

- U.K. Halifax House Price Index for March 2026 at 6:00 am GMT

- France Balance of Trade for February 2026 at 6:45 am GMT

- Swiss Unemployment Rate for March 2026 at 7:00 am GMT

- Euro area PPI for February 2026 at 9:00 am GMT

- Euro area Retail Sales for February 2026 at 9:00 am GMT

- U.S. MBA 30-Year Mortgage Rate for April 3, 2026 at 11:00 am GMT

- U.S. EIA Crude Oil Stocks Change for April 3, 2026 at 2:30 pm GMT

- U.S. Fed Daly Speech at 5:05 pm GMT

- U.S. FOMC Minutes at 6:00 pm GMT

Wednesday’s calendar carries significant event risk on multiple fronts. The RBNZ interest rate decision at 2:00 am GMT is the overnight highlight, arriving against a backdrop of elevated commodity price volatility and a challenging global growth outlook driven by the ongoing Strait of Hormuz disruptions. Markets will be watching closely for any guidance on the rate path given the inflationary pressures from elevated oil prices.

The FOMC minutes release at 6:00 pm GMT will likely draw considerable market attention, particularly given Tuesday’s comments from Fed officials Goolsbee and Williams flagging concern about the economic implications of the oil shock. Any language pointing to a more cautious or data-dependent stance, especially in light of rising energy prices, could influence rate cut expectations and trigger volatility in rates and the dollar. Fed speakers Daly and Jefferson are also scheduled, offering additional opportunities for market-moving commentary.

On the geopolitical front, the resolution or further escalation of the U.S.-Iran situation following Tuesday’s 8 p.m. ET deadline will likely continue to dominate oil price action and broader risk sentiment heading into Wednesday’s session. Any breakthrough in ceasefire talks could add further selling pressure to crude, while a breakdown in negotiations could rapidly reverse Tuesday’s late-session calm.

Stay frosty out there, forex friends!

Promotion: Today’s Session Was a Stress Test for Your Trading Psychology. Did You Pass?

Today’s session handed traders a masterclass in decision-making under pressure.

The dollar collapsed on data. Oil whipsawed $5 intraday. Safe-haven flows pushed gold to fresh highs — then ceasefire headlines flipped the script in the final hour.

If you were positioned before any of those moves, you faced the choice most traders fumble: hold, flip, or freeze?

In Positive Trading Psychology, Brett Steenbarger argues that surviving sessions like today isn’t about eliminating emotional responses — it’s about channeling your character strengths to stay clinical when everyone else is chasing the next headline.

Learn more about “Positive Trading Psychology: Turning personal strengths into trading strengths” on Amazon!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.