Escalating Middle East tensions defined Monday’s session, with Iran formally rejecting a proposed ceasefire and President Trump threatening to destroy Iranian infrastructure ahead of a Tuesday deadline, keeping oil prices volatile and broader risk sentiment fragile. The U.S. dollar closed the day as arguably the weakest major currency, pressured primarily by a sharp selloff at the London open correlating with fresh Strait of Hormuz headline risk, while a mixed ISM Services report offered conflicting signals on the health of the U.S. economy.

Bitcoin stood out as the session’s strongest performer, surging above $70,000 as a wave of short liquidations amplified an intraday squeeze fueled by shifting ceasefire sentiment.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Tehran had received Pakistan’s mediation proposal; Iran would not accept deadlines or pressure to make a decision; Tehran would not reopen the Strait of Hormuz in exchange for a temporary ceasefire

- Canada S&P Global Services PMI for March 2026: 47.2 (48.0 forecast; 46.5 previous)

- ISM U.S. Services PMI for March 2026: 54.0 (54.0 forecast; 56.1 previous)

- ISM Services Employment for March 2026: 45.2 (51.7 forecast; 51.8 previous)

- ISM Services Prices for March 2026: 70.7 (70.0 forecast; 63.0 previous)

- President Trump, at a White House news conference on Monday, insisted that freedom of navigation through the Strait of Hormuz be part of any deal and threatened to destroy Iranian infrastructure, including bridges and power plants, by Tuesday evening if terms were not met.

Promotion: Use TradeZella’s AI Powered trade journal to deep-dive into your execution and see exactly how you performed during today’s trading session.

Click here to get the TradeZella Edge and use code PIPS20 to save 20% on your first purchase!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

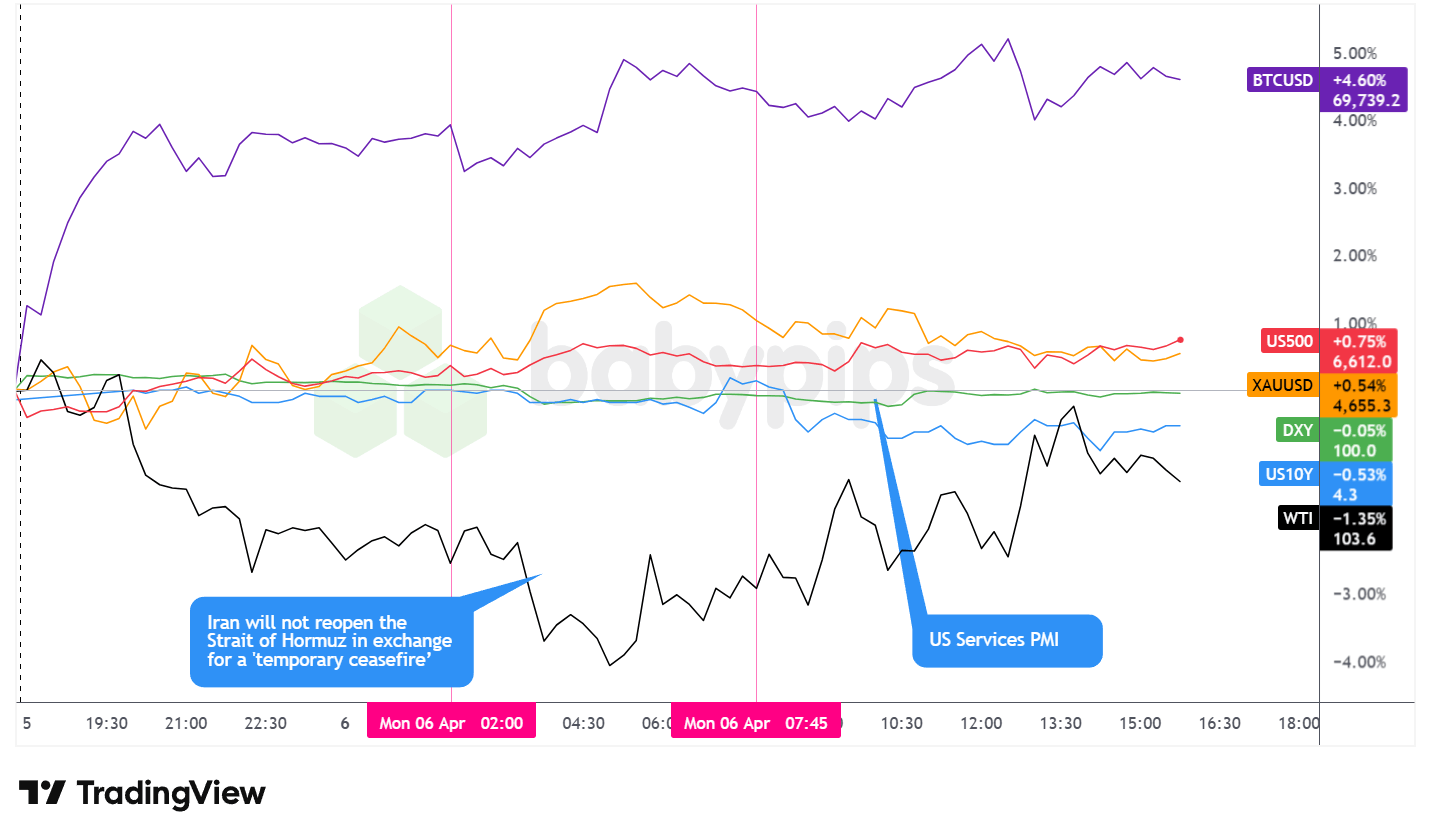

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Monday’s session reflected the ongoing tension between episodic ceasefire optimism and escalating military rhetoric, with asset classes responding to headline flow rather than anchoring to traditional macro drivers.

The S&P 500 posted a modest gain of approximately 0.75%, closing near 6,608. Equities climbed steadily from the overnight session through the New York open, with Iran-related headline volatility appearing to generate a buy-the-dip response rather than a sustained risk-off flight. The ISM Services PMI release at 10:00 AM ET triggered a brief dip, likely reflecting the sharp employment subindex miss, which contracted to 45.2 versus the 51.7 forecast and marked its steepest decline since 2023. Equities absorbed the data and held their gains into the close, possibly supported by the still-expansionary headline activity reading and the prevailing market view that Fed officials retain room to stay patient.

Bitcoin was the session’s standout performer, rallying approximately 4.60% on the broad market overlay to trade near $69,739 at the time of the chart capture. The cryptocurrency briefly surpassed $70,300 intraday before paring some of the advance. According to Bloomberg reporting, over $145 million in short positions were liquidated within the session as traders who had accumulated heavy bearish positioning into the weekend were forced to cover amid shifting ceasefire headlines. Analysts noted thin liquidity conditions as an amplifying factor.

Gold traded with notable intraday volatility, rallying sharply to near $4,706 during the early London hours before pulling back steadily through the U.S. session as the initial safe-haven bid faded. Gold closed at approximately +0.54% near $4,655.3.

WTI crude oil traded in a wide intraday range consistent with the Hormuz risk narrative. The contract dropped sharply toward the $100.50 area during the London session before recovering through U.S. morning hours, then fading again into the close as Trump’s press conference rhetoric renewed fears of prolonged strait disruption. Late-session reports of drone strikes on Iraqi oilfields likely added further volatility to directional positioning.

U.S. 10-year Treasury yields traded mostly sideways during the Asia and London session, but then appeared to drift off intraday highs through the U.S. afternoon, possibly correlated with the weak ISM employment subindex and broader uncertainty about the economic outlook under prolonged geopolitical stress.

Promoted: Capitalize on News Catalysts Without Risking Your Own Funds.

Iran rejected ceasefire talks. Trump threatened strikes by Tuesday. WTI whipsawed from $100.50 to $105 and back — all in a single session.

On a small personal account, navigating that kind of volatility means trading position sizes too small to matter.Alpha Capital Group changes the math. By providing access to simulated funded accounts from $5K to $200K, starting at $50, you can execute high-conviction setups with the professional position sizing they deserve. Join 250K+ traders in 180+ countries today!

Learn more about Alpha Capital Group!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

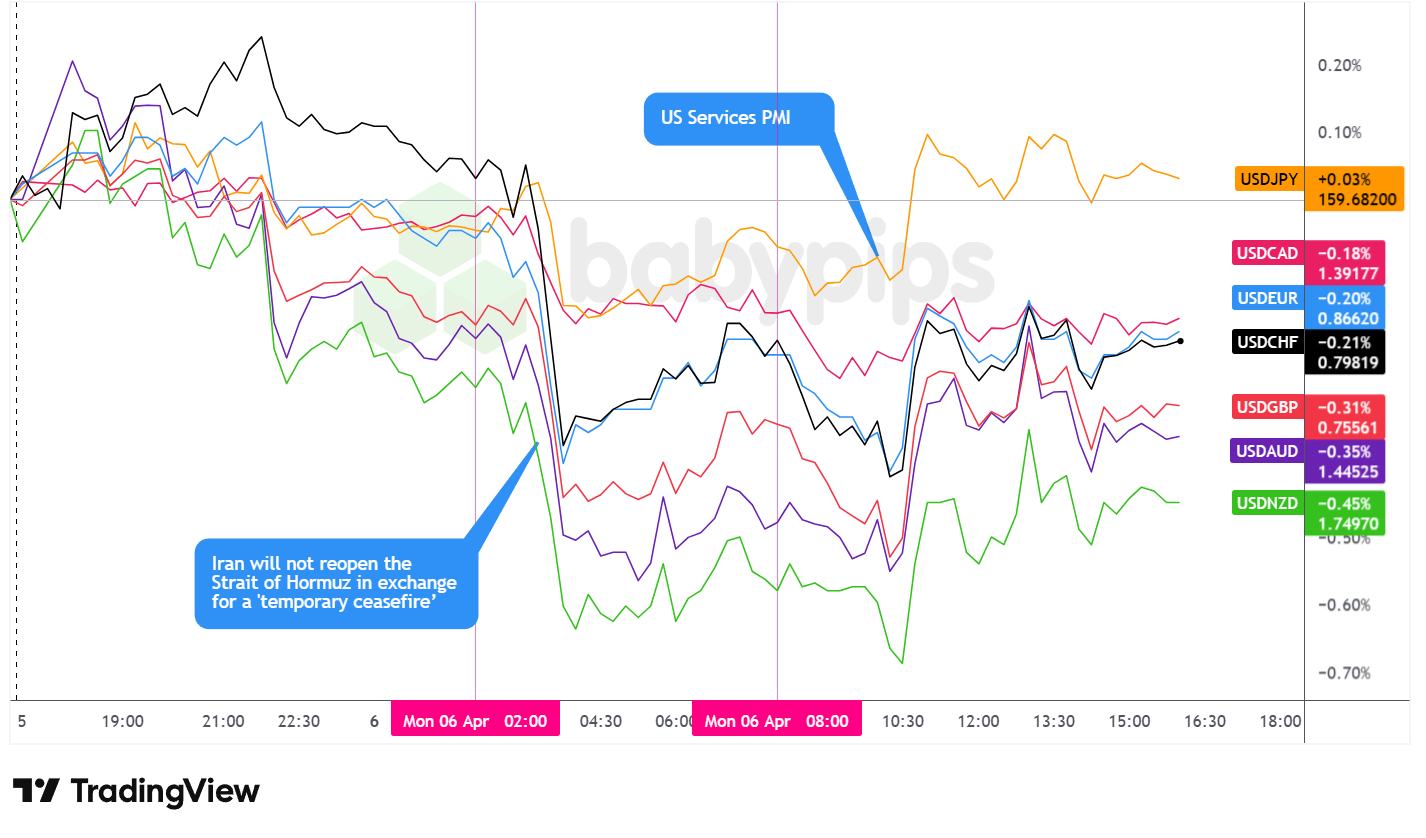

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar traded with a broadly bearish bias on Monday, navigating geopolitical headline risk and a domestic data release that delivered conflicting signals. The greenback closed the day as the second weakest major currency on the session, posting net losses against all tracked pairs with the exception of the Japanese yen.

During the Asian session, the dollar rebounded slightly against the major currencies following the Monday open before pulling lower through mid-morning trading, establishing a net negative bias heading into the London session. No single clear catalyst drove the partial early recovery, and the subsequent retreat suggested that any initial defensiveness proved short-lived as geopolitical developments continued to accumulate.

Shortly after the London session opened, the dollar fell sharply against the major currencies, likely correlated with the Senior Iranian Official statements confirming that Tehran would not reopen the Strait of Hormuz in exchange for a temporary ceasefire. The DXY dipped toward the 99.76-99.79 area in the early European hours. However, the move quickly stabilized, with the dollar finding a floor heading into the U.S. trading session, possibly as traders assessed that the Hormuz standoff had already been partially priced and the immediate shock was absorbed relatively rapidly.

After the U.S. session opened, the dollar initially pulled back slightly before rebounding through the morning hours. The ISM Services PMI data at 10:00 AM ET delivered a mixed picture: the headline print met expectations at 54.0, but the employment subindex contracted sharply to 45.2 (versus 51.7 forecast), its steepest decline since 2023. Meanwhile, the prices index accelerated to 70.7 and new orders beat at 60.6. The stagflationary texture of the report likely limited the dollar’s recovery potential even as it prevented an outright resumption of the London-session selloff. The dollar stabilized and traded choppy through the remainder of the U.S. session without recouping its earlier losses in any meaningful way.

Upcoming Potential Catalysts on the Economic Calendar

- Australia S&P Global Services PMI Final for March 2026 at 11:00 pm GMT

- Japan Household Spending for February 2026 at 11:30 pm GMT

- Japan Average Cash Earnings for February 2026 at 11:30 pm GMT

- Australia TD-MI Inflation Gauge for March 2026 at 1:00 am GMT

- Australia Household Spending for February 2026 at 1:30 am GMT

- Australia ANZ-Indeed Job Ads for March 2026 at 1:30 am GMT

- Japan Leading Economic Index Prel for February 2026 at 5:00 am GMT

- Euro area S&P Global Services PMI Final for March 2026 at 8:00 am GMT

- U.K. S&P Global Services PMI Final for March 2026 at 8:30 am GMT

- U.S. ADP Employment Change Weekly for March 21, 2026 at 12:15 pm GMT

- U.S. Durable Goods Orders for February 2026 at 12:30 pm GMT

- New Zealand Global Dairy Trade Price Index for April 7, 2026

- Canada Ivey PMI s.a for March 2026 at 2:00 pm GMT

- U.S. Consumer Inflation Expectations for March 2026 at 3:00 pm GMT

- U.S. Fed Goolsbee Speech at 4:35 pm GMT

- U.S. Consumer Credit Change for February 2026 at 7:00 pm GMT

Tuesday’s calendar carries significant volatility potential across multiple sessions. Japan’s household spending and average cash earnings data at 11:30 pm GMT will be monitored for signs of domestic consumption resilience and wage momentum. A cluster of Australian releases spanning 11:00 pm through 1:30 am GMT could influence AUD positioning following Monday’s notable outperformance against the greenback. The final Services PMI readings for the euro area (8:00 am GMT) and U.K. (8:30 am GMT) will draw attention if they diverge from flash estimates.

The primary U.S. catalysts arrive early in the session, with ADP Employment Change at 12:15 pm GMT and Durable Goods Orders at 12:30 pm GMT. Both carry heightened market relevance as traders attempt to read through the mixed ISM Services employment signals from Monday. U.S. Consumer Inflation Expectations at 3:00 pm GMT and Fed’s Goolsbee speech at 4:35 pm GMT could add further clarity on the policy outlook, especially with services inflation running hot.

Overhanging the entire session is Trump’s Tuesday 8:00 PM ET deadline for Iran, which carries the potential to drive outsized moves across oil, safe-haven assets, and risk sentiment if escalation or a diplomatic breakthrough develops.

Stay frosty out there, forex friends!

Promotion: Today’s Session Was a Stress Test for Your Trading Psychology. Did You Pass?

Iran rejected a ceasefire. Trump threatened strikes. Oil whipsawed 4% intraday. Bitcoin short-squeezed above $70K.

If you were positioned before those headlines broke, you faced the choice most traders fumble: hold, flip, or freeze?

In Positive Trading Psychology, Brett Steenbarger argues that surviving sessions like today isn’t about eliminating emotional responses — it’s about channeling your character strengths to stay clinical when everyone else is chasing the next headline.

Learn more about “Positive Trading Psychology: Turning personal strengths into trading strengths” on Amazon!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.