Markets absorbed the aftershocks of President Trump’s Wednesday evening address on Iran, which fell short of the de-escalation signal investors had positioned for and sent oil prices surging more than 10% while equities whipsawed between sharp early losses and a late-session recovery. The U.S. dollar emerged as the session’s strongest major currency, while gold declined sharply and Bitcoin extended its recent pullback.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- In his primetime speech, President Trump’s refusal to provide a definitive end date for the conflict and his vow to “hit them extremely hard” triggered a sharp market reaction, causing global stocks to tumble as initial hopes for a quick de-escalation evaporated, and oil prices surged.

- Australia Balance of Trade for February 2026: 5.69B (1.5B forecast; 2.63B previous)

- Swiss Inflation Rate for March 2026: 0.2% m/m (0.4% m/m forecast; 0.6% m/m previous); 0.3% y/y (0.5% y/y forecast; 0.1% y/y previous)

- ECB’s Simkus said it is too early to determine what action will be needed at the April meeting.

- U.S. Challenger Job Cuts for March 2026: 60.62k (90.0k forecast; 48.31k previous)

- Canada Balance of Trade for February 2026: -5.74B (-1.8B forecast; -3.65B previous)

- U.S. Goods Trade Balance for February 2026: -83.5B (-84.0B forecast; -80.8B previous)

- U.S. Initial Jobless Claims for March 28, 2026: 202.0k (213.0k forecast; 210.0k previous)

- U.S. Balance of Trade for February 2026: -57.3B (-60.0B forecast; -54.5B previous)

- Iran is drafting a protocol with Oman to monitor traffic through the Strait of Hormuz

Promotion: Use TradeZella’s AI Powered trade journal to deep-dive into your execution and see exactly how you performed during today’s trading session.

Click here to get the TradeZella Edge and use code PIPS20 to save 20% on your first purchase!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

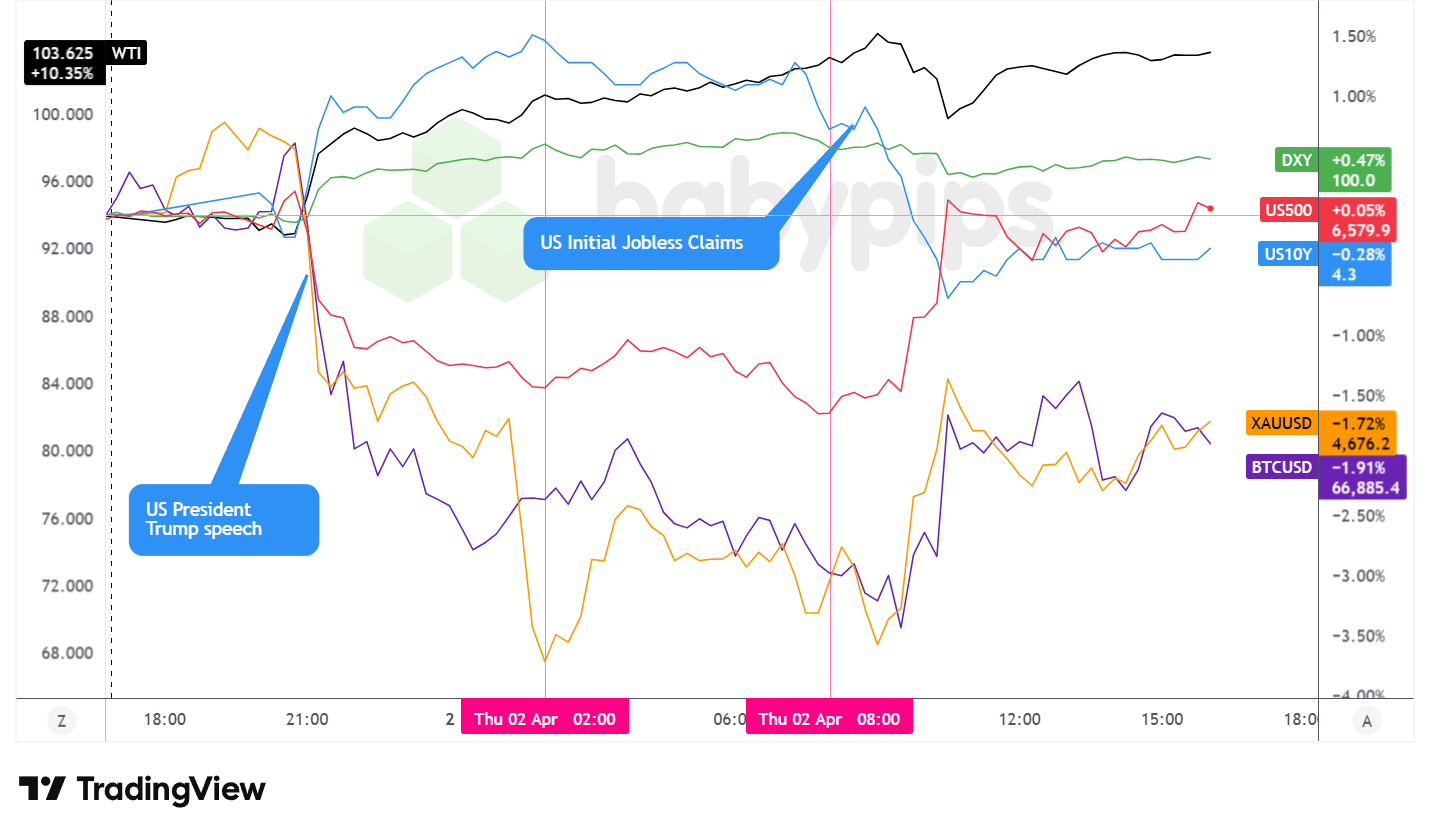

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Thursday’s session opened under pressure as investors digested Wednesday night’s speech by President Trump, which reiterated a 2-3 week timeline for operations in Iran while warning of potential strikes on electricity and oil infrastructure if a deal is not reached. Markets had positioned for a softer tone following two consecutive days of risk-on momentum, and the hawkish framing quickly reset that positioning.

WTI crude oil surged more than 10% on the session, reaching an intraday high near $105 and settling around $103.60, its highest close in roughly four years. The move reflected a continued reassessment of Strait of Hormuz supply risk following Trump’s speech, with oil firmly in the driver’s seat of broader risk appetite throughout the day. The magnitude of the gain came despite an intraday pullback of several dollars per barrel following reports midday that Iran was in talks with Oman over a traffic monitoring protocol for the strait.

The S&P 500 closed just above flat at approximately 6,583, up a marginal 0.05% after falling as much as roughly 1.5% earlier in the session. The intraday recovery coincided with the Hormuz protocol headline, suggesting equity traders opted to look past the embedded oil premium in favor of any reopening signal, however tentative. Tesla shares weighed on the index after the company reported one of its weakest sales quarters in recent memory, while shares of Blue Owl Capital and top asset managers also declined.

Gold fell approximately 1.72% to trade near $4,676, reversing gains from earlier in the week. The decline appeared to reflect a combination of rising oil-driven inflation expectations pressuring real assets and broad portfolio deleveraging. The precious metal tested intraday lows near $4,556 before partially recovering into the close.

Bitcoin declined roughly 1.91% to trade near $66,885, extending its recent weakness alongside broader risk-off sentiment. The cryptocurrency sold off sharply in the early Asian session following Trump’s speech before finding tentative stabilization above the $66,000 area, though no meaningful recovery materialized through the rest of the day.

The 10-year U.S. Treasury yield closed around 4.31%, down approximately 0.28% on the day. Yields had climbed to an intraday high near 4.39% during the Asia-London session before reversing sharply lower after the U.S. Jobless Claims data release, with the move possibly reflecting a flight-to-safety bid in Treasuries as equities came under pressure during the worst of the session’s losses.

Promoted: Capitalize on News Catalysts Without Risking Your Own Funds.

Today, oil popped in reaction to Trump’s latest threats of attack. On a small personal account, riding that kind of move means trading tiny position sizes that barely move the needle.

Alpha Capital Group changes the math. By providing access to simulated funded accounts from $5K to $200K, starting at $50, you can execute high-conviction setups with the professional position sizing they deserve. Join 250K+ traders in 180+ countries today!

Learn more about Alpha Capital Group!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

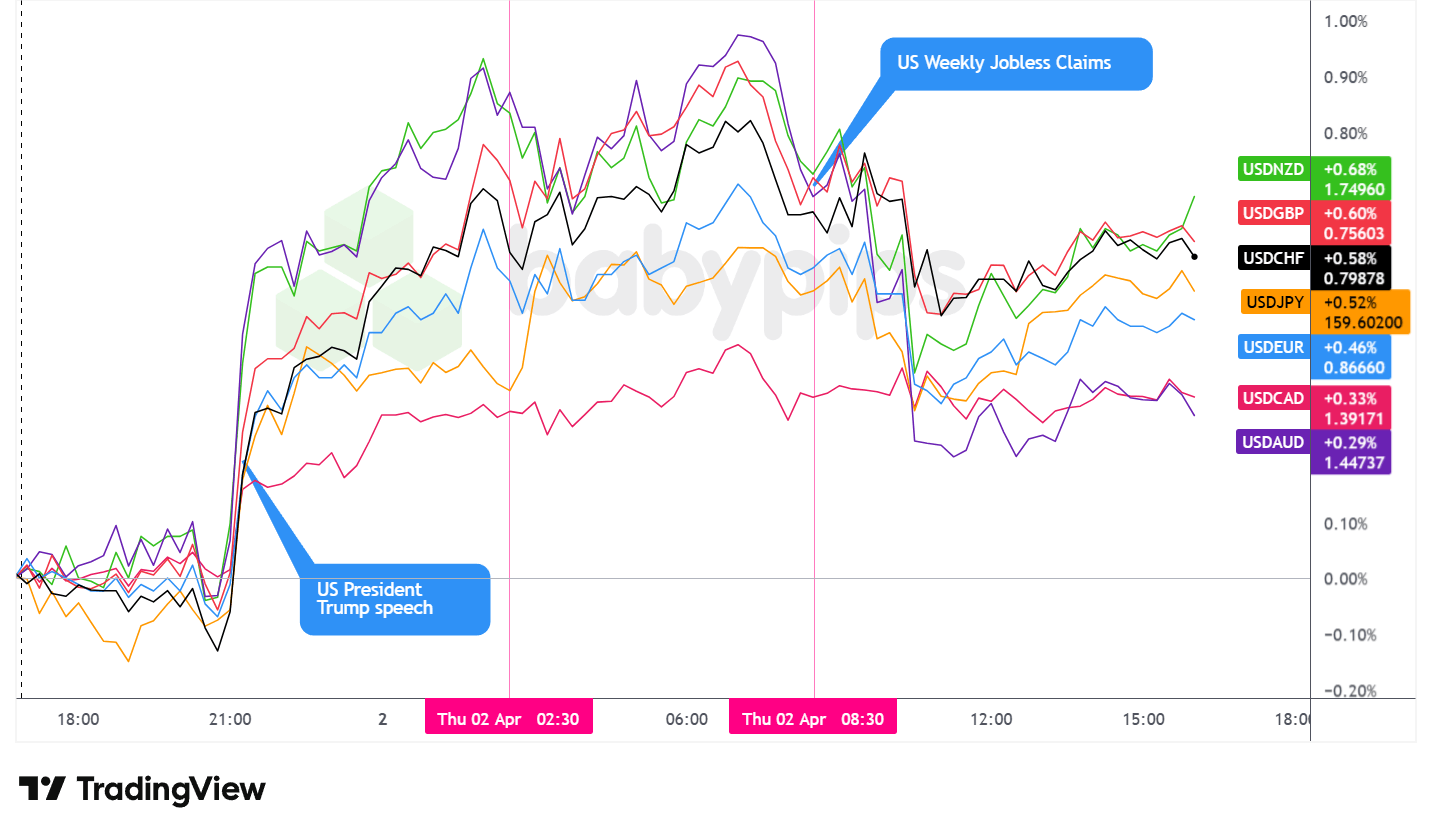

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar posted broad gains across all major currency pairs on Thursday, closing as the best performing major currency on a daily basis. The session’s dominant driver was President Trump’s Wednesday evening address on the Iran conflict, which triggered a sharp, sustained move higher in the greenback that set the tone for the entire trading day.

During the Asian session, the dollar initially traded with low volatility and little directional conviction in the early hours. That changed quickly when the Trump speech triggered a sharp spike higher across all USD pairs, with the move sharp enough to be clearly visible across the overlay chart above. The dollar held those gains and sustained them through the remainder of the Asian session heading into the London open. The initial reaction reflected a classic safe-haven bid, consistent with the broader repricing in oil and risk assets that followed the speech.

During the London session, the dollar traded with a slightly choppier character. It dipped modestly early in European hours before rebounding, and then dipped a second time heading toward the U.S. open. Switzerland’s March CPI came in soft across the board, printing at 0.3% year-over-year against the 0.5% expected and a previous read of 0.1%, reinforcing dovish expectations for the Swiss National Bank and providing a headwind for the franc. The ECB’s Simkus added a note of uncertainty for the euro by signaling it was too early to determine whether April would bring additional easing. Australia’s February trade surplus came in at AUD 5.69B, more than triple the 1.5B forecast, driven in part by strong gold exports, though the outperformance was paired with a notable decline in imports, raising questions about the strength of domestic demand. The AUD response was muted on the session as the overall risk-off tone and USD strength dominated.

Canada’s February trade balance disappointed sharply, widening to -5.74B against the -1.8B forecast as imports surged well beyond expectations. Despite the negative headline, the Canadian dollar held relatively firm compared to other majors against the USD, likely supported in part by the sharp rally in crude oil prices, given the currency’s strong historical correlation with energy markets.

During the U.S. session, the dollar came under pressure as the session progressed. Weekly Initial Jobless Claims came in well below expectations at 202k versus the 213k forecast and a prior reading of 210k, pointing to continued resilience in the labor market. This data initially appeared to correlate with a brief reversal in several USD pairs on the overlay, with the dollar softening shortly after the release. The broader U.S. trade deficit for February also beat expectations at -57.3B versus the -60.0B forecast, with exports surprising to the upside. Despite the favorable data, the dollar continued to weaken during the U.S. session, bottoming out just after the London close before recovering slightly and grinding higher through the remainder of the afternoon.

Upcoming Potential Catalysts on the Economic Calendar

- Japan S&P Global Services PMI Final for March 2026 at 12:30 am GMT

- China RatingDog Services PMI for March 2026 at 1:45 am GMT

- France Industrial Production for February 2026 at 6:45 am GMT

-

U.S. Nonfarm Payrolls for March 2026 at 12:30 pm GMT

- U.S. Unemployment Rate for March 2026 at 12:30 pm GMT

- U.S. Average Hourly Earnings for March 2026 at 12:30 pm GMT

- U.S. S&P Global Services PMI Final for March 2026 at 1:45 pm GMT

Friday’s calendar is dominated by the March Nonfarm Payrolls release at 8:30 a.m. ET, against a forecast of approximately +57k following February’s steep -92k contraction. The report arrives on Good Friday, meaning U.S. equity and bond markets will be closed for the session, though futures markets will remain active. Any meaningful deviation from expectations, particularly to the upside, could prompt a pricing adjustment in rate expectations and a notable reaction in the dollar and Treasury futures when cash markets reopen Monday.

The ISM Services PMI for March follows at 10:00 a.m. ET and will draw attention in the context of the energy shock, as services-sector confidence and input costs could offer early clues about whether the oil price surge is beginning to filter through to the broader U.S. economy. Markets will also be monitoring any weekend developments in the Iran conflict, particularly around the Strait of Hormuz, as any progress or setbacks on that front could significantly shape risk sentiment at Monday’s open.

Stay frosty out there, forex friends!

Promotion: Today’s Session Was an Opportunity to Practice Emotional Discipline. Were You Ready for It?

Thursday price action was ripe with opportunity as oil rallied while bitcoin and gold fell following Trump’s speech.

If you were positioned before today’s headlines and data broke, you faced the choice most traders fumble: hold, flip, or freeze?

In Positive Trading Psychology, renowned psychologist Brett Steenbarger argues that surviving sessions like today isn’t about eliminating emotional responses — it’s about channeling your character strengths to stay clinical when everyone else is reacting to the next headline. When a war-risk premium can reverse in a single news cycle, your psychology isn’t a soft edge. It’s your hardest one.

Learn more about “Positive Trading Psychology: Turning personal strengths into trading strengths” on Amazon!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.