Ceasefire speculation dominated Tuesday’s global session, with signals from both Washington and Tehran that the US-Iran conflict may be taking steps towards a resolution, triggering a sharp risk-on rotation across equities, gold, and the broader financial complex. The S&P 500 posted its strongest single-session gain since May, oil reversed aggressively from earlier highs, and the US dollar ended the day as the worst-performing major currency as risk appetite broadly improved on diplomatic headlines.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Trump open to ending Iran war without reopening Strait of Hormuz

- Japan Unemployment Rate for February 2026: 2.6% (2.7% forecast; 2.7% previous)

- Japan Tokyo CPI for March 2026: 1.4% y/y (1.7% y/y forecast; 1.6% y/y previous)

- Japan Industrial Production Prel for February 2026: -2.1% m/m (-2.0% m/m forecast; 4.3% m/m previous); 0.3% y/y (1.0% y/y forecast; 0.7% y/y previous)

- Japan Retail Sales for February 2026: -2.0% m/m (-0.9% m/m forecast; 4.1% m/m previous); -0.2% y/y (1.5% y/y forecast; 1.8% y/y previous)

- New Zealand ANZ Business Confidence for March 2026: 32.5 (57.0 forecast; 59.2 previous)

- RBA Meeting Minutes showed a narrowly split Board that ultimately opted for a 25bp hike to 4.10%, judging that financial conditions need to be more restrictive to address persistent above‑target inflation and upside risks from higher oil prices and the Middle East conflict.

- China NBS Manufacturing PMI for March 2026: 50.4 (49.8 forecast; 49.0 previous)

- China NBS General PMI for March 2026: 50.5 (50.2 forecast; 49.5 previous)

- Japan Housing Starts for February 2026: -4.9% y/y (1.0% y/y forecast; -0.4% y/y previous)

- Germany Import Prices for February 2026: 0.3% m/m (0.5% m/m forecast; 1.1% m/m previous); -2.3% y/y (-2.1% y/y forecast; -2.3% y/y previous)

- Germany Retail Sales for February 2026: -0.6% m/m (0.5% m/m forecast; -0.9% m/m previous); 0.7% y/y (1.1% y/y forecast; 1.2% y/y previous)

- U.K. Nationwide Housing Prices for March 2026: 0.9% m/m (0.6% m/m forecast; 0.3% m/m previous); 2.2% y/y (1.5% y/y forecast; 1.0% y/y previous)

- U.K. GDP Growth Rate Final for Q4 2025: 0.1% q/q (0.1% q/q forecast; 0.1% q/q previous); 1.0% y/y (1.0% y/y forecast; 1.3% y/y previous)

-

Germany Unemployment Change for March 2026: 0.0k (5.0k forecast; 1.0k previous)

- Germany Unemployment Rate for March 2026: 6.3% (6.3% forecast; 6.3% previous)

- Euro area CPI Growth Rate Flash for March 2026: 1.2% m/m (1.4% m/m forecast; 0.6% m/m previous); 2.5% y/y (2.7% y/y forecast; 1.9% y/y previous)

- Canada GDP Prel for February 2026: 0.2% m/m (0.1% m/m forecast; 0.0% m/m previous)

- U.S. S&P/Case-Shiller Home Price for January 2026: -0.1% m/m (-0.2% m/m forecast; -0.1% m/m previous); 1.2% y/y (1.3% y/y forecast; 1.4% y/y previous)

- U.S. Chicago PMI for March 2026: 52.8 (54.0 forecast; 57.7 previous)

- U.S. JOLTs Job Openings for February 2026: 6.88M (6.7M forecast; 6.95M previous)

- CB U.S. Consumer Confidence for March 2026: 91.8 (86.0 forecast; 91.2 previous)

- On Tuesday, Iran’s Foreign Minister Abbas Araghchi confirms that messages have been exchanged with the US, but insists Tehran is not in negotiations with Washington

Promotion: Use TradeZella’s AI Powered trade journal to deep-dive into your execution and see exactly how you performed during today’s trading session.

Click here to get the TradeZella Edge and use code PIPS20 to save 20% on your first purchase!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

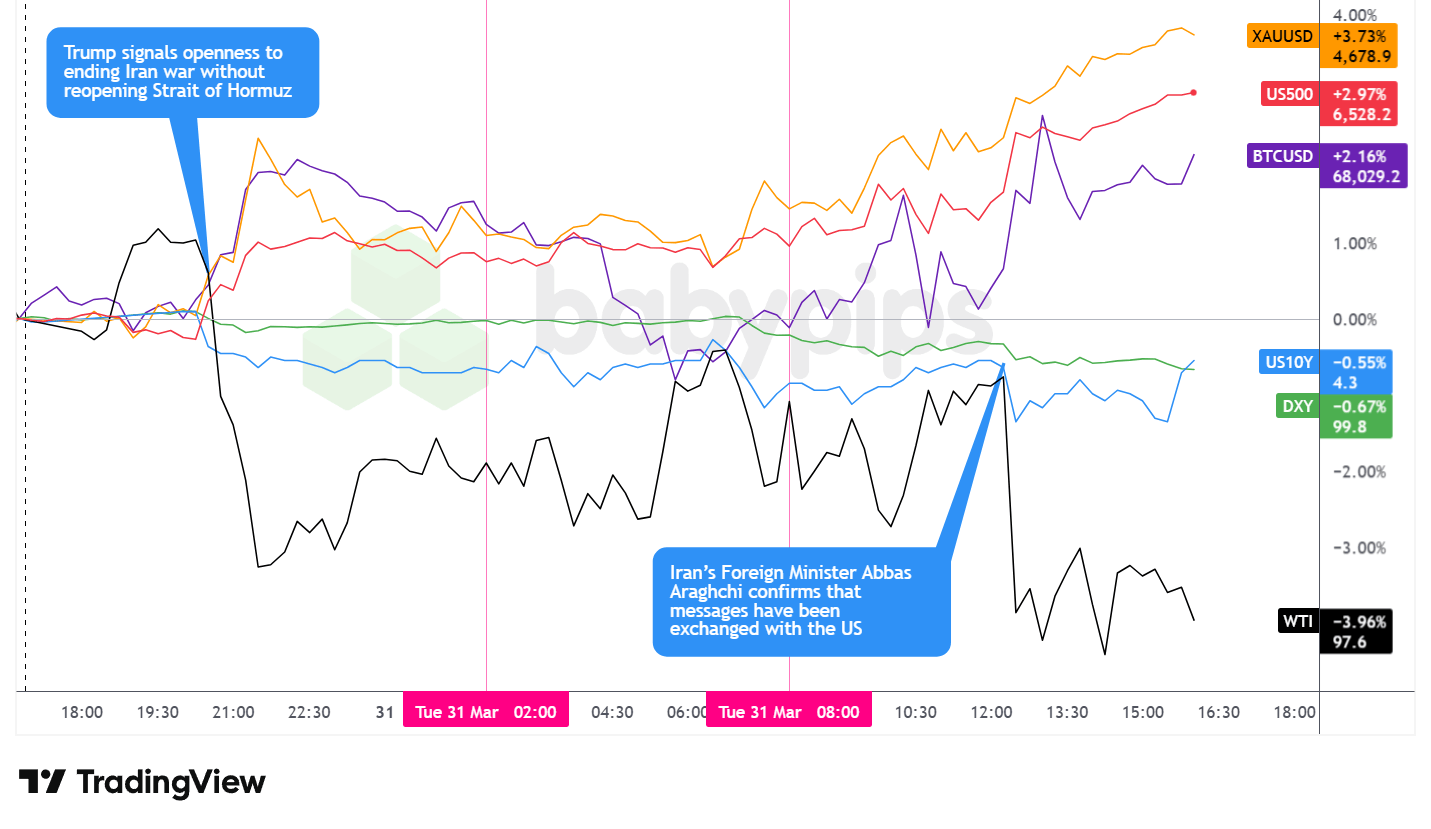

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Tuesday’s broad market session was defined almost entirely by geopolitical sentiment tied to the US-Iran conflict, as signals from both Washington and Tehran that a resolution may be approaching triggered a sharp risk-on rotation and one of the most consequential sessions in recent weeks. Equities surged, oil reversed dramatically lower, gold continued its record run, and Treasury yields drifted lower across the session.

The S&P 500 surged 2.99% to close at 6,529, its largest single-session gain since May. Futures had already been building during Asian hours following the WSJ report that President Trump was open to ending the war without requiring the Strait of Hormuz to reopen, and the index maintained a constructive tone through both the Asian and London sessions before a further acceleration into the US session drove it to intraday highs near 6,541. Airlines and travel-related sectors led gains, while energy producers lagged, broadly consistent with the easing war-premium narrative.

Gold gained 3.73% to close near $4,677, extending its record-setting run despite the more optimistic geopolitical backdrop. The precious metal had traded with sharp two-way volatility during the Asian session, popping higher early, then briefly pulling back before recovering alongside equities. Rather than retreating on improved risk sentiment, gold appeared to continue benefiting from US dollar Weakness and not its typical role as a geopolitical and inflation hedge, climbing steadily through the US session alongside equities.

WTI crude oil declined 3.96% to settle near $97.60, the session’s weakest performer among major assets tracked. Oil had initially extended gains after the Asian session open on escalating Middle East developments, including reports of a tanker strike in Dubai’s port and missile interceptions in Saudi Arabia, with prices briefly touching the $103 area on those escalation headlines. The sharp reversal lower appeared to correlate with the WSJ report that Trump was open to ending the conflict without the Strait of Hormuz reopening condition, which eased the most acute near-term fears around a prolonged supply disruption. Oil remained under sustained selling pressure into the US close.

Bitcoin gained 1.91% to trade near $68,010, participating in the broader risk-on sentiment but trailing equities and gold in percentage-gain terms. The cryptocurrency moved like a rollercoaster, first higher then lower during the Asian session before recovering through the London hours and extending gains into the US session, with no apparent direct crypto-specific catalyst, suggesting the move likely reflected the broader improvement in risk appetite.

The 10-year Treasury yield declined approximately 0.55% to settle near 4.30%, with the bond market bid building steadily through the session. Yields had already been drifting lower during Asian hours before the softer-than-expected Eurozone core CPI reading (2.3% y/y versus 2.6% forecast) added brief support during the London session. Yields remained choppy through the US afternoon as markets absorbed a mix of domestic data, including a better-than-expected Consumer Confidence print of 91.8 (versus 86.0 forecast) and JOLTs job openings that came in above forecast at 6.88M but declined from the prior month’s 6.95M, together suggesting gradual rather than sharp deterioration in labor market conditions.

Promoted: Capitalize on News Catalysts Without Risking Your Own Funds.

Today, oil dropped like a rock on prospects for military de-escalation. On a small personal account, riding that kind of move means trading tiny position sizes that barely move the needle.

Alpha Capital Group changes the math. By providing access to simulated funded accounts from $5K to $200K, starting at $50, you can execute high-conviction setups with the professional position sizing they deserve. Join 250K+ traders in 180+ countries today!

Learn more about Alpha Capital Group!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

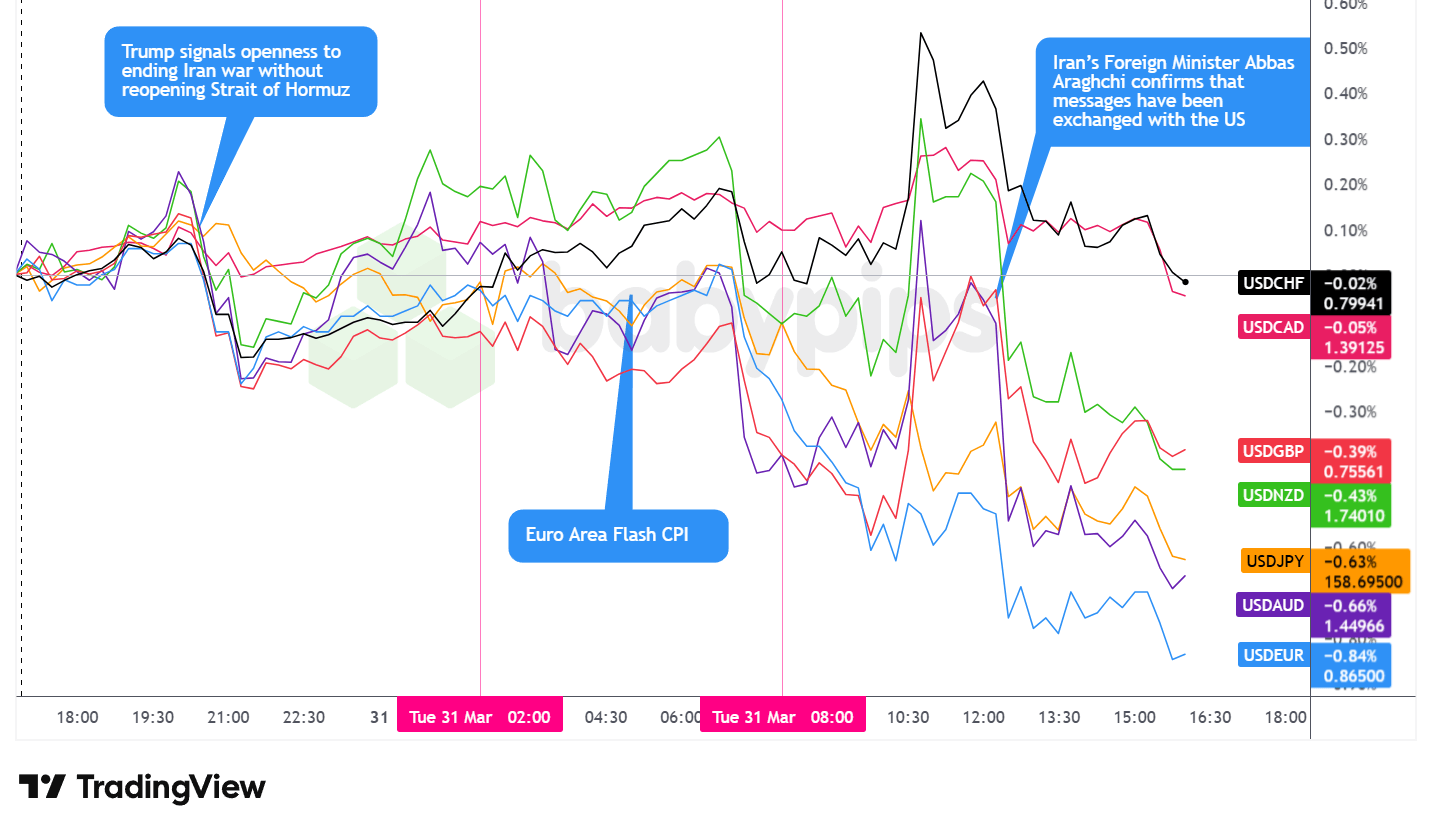

Overlay of USD vs. Majors – Chart Faster With TradingView

The US dollar closed Tuesday as the worst-performing major currency on a daily basis, pressured throughout the session by improving risk sentiment tied to ceasefire speculation and signs of diplomatic engagement between Washington and Tehran.

During the Asian session, the dollar traded choppy, opening slightly positive before pulling back quickly in a move that appeared to correlate with the early circulation of the WSJ report that President Trump was open to ending the Iran conflict without requiring the Strait of Hormuz to reopen. The initial decline was followed by a modest rebound, with the greenback recovering some ground heading into the London open, though the overall tone remained tentative and the session produced no sustained directional commitment.

The London session brought choppy and mostly sideways price action for the dollar, with no clear directional push for much of the European morning. The Eurozone Flash CPI print for March showed headline inflation accelerating to 2.5% y/y (from 1.9% prior), driven primarily by war-related energy prices, while core inflation surprised to the downside at 2.3% y/y (versus 2.6% forecast and 2.4% prior), suggesting the underlying inflationary backdrop outside of energy remained comparatively contained. The data appeared to produce some brief market reaction around the release, with the overlay chart showing a short-lived response before settling back. Bearish pressure on the dollar built more notably just ahead of the US session open, with most pairs tilting lower as the European morning concluded.

The US session brought elevated volatility for the dollar. The greenback initially pulled back before spiking sharply higher just ahead of the London close, possibly reflecting a short-term technical repositioning or a brief safe-haven bid on residual Middle East uncertainty, before reversing decisively to the downside through the remainder of the session. Iran’s Foreign Minister Araghchi confirming that messages had been exchanged with the US appeared to reinforce ceasefire optimism and likely contributed to the dollar’s afternoon selloff, as risk assets maintained their gains and the greenback remained under pressure into the close.

Upcoming Potential Catalysts on the Economic Calendar

- U.S. API Crude Oil Stock Change for March 27, 2026 at 8:30 pm GMT

- New Zealand Building Permits for February 2026 at 9:45 pm GMT

- Australia S&P Global Manufacturing PMI Final for March 2026 at 10:00 pm GMT

- Japan Tankan Large Manufacturers Index for March 31, 2026 at 11:50 pm GMT

- Australia Building Permits Prel for February 2026 at 12:30 am GMT

- Japan S&P Global Manufacturing PMI Final for March 2026 at 12:30 am GMT

- China RatingDog Manufacturing PMI for March 2026 at 1:45 am GMT

- Australia Commodity Prices for March 2026 at 5:30 am GMT

- Swiss Retail Sales for February 2026 at 6:30 am GMT

- Swiss procure.ch Manufacturing PMI for March 2026 at 7:30 am GMT

- Germany S&P Global Manufacturing PMI Final for March 2026 at 7:55 am GMT

- Euro area S&P Global Manufacturing PMI Final for March 2026 at 8:00 am GMT

- U.K. S&P Global Manufacturing PMI Final for March 2026 at 8:30 am GMT

- Euro area Unemployment Rate for February 2026 at 9:00 am GMT

- U.S. MBA Mortgage Applications for March 27, 2026 at 11:00 am GMT

- U.S. MBA 30-Year Mortgage Rate for March 27, 2026 at 11:00 am GMT

- U.S. ADP National Employment Report for March 2026 at 12:15 pm GMT

- U.S. Retail Sales for February 2026 at 12:30 pm GMT

- U.S. Fed Barr Speech at 1:13 pm GMT

- Canada S&P Global Manufacturing PMI for March 2026 at 1:30 pm GMT

- U.S. S&P Global Manufacturing PMI Final for March 2026 at 1:45 pm GMT

- U.S. ISM Manufacturing PMI for March 2026 at 2:00 pm GMT

- EIA Crude Oil Stocks Change for March 27, 2026 at 2:30 pm GMT

- Canada BoC Summary of Deliberations at 5:30 pm GMT

Wednesday’s calendar is loaded with high-impact data across multiple regions.

In the upcoming Asia session, the Japan Tankan Large Manufacturers Index at 11:50 pm GMT and the China RatingDog Manufacturing PMI at 1:45 am GMT will attract attention for any further signals on Asian industrial momentum, following Tuesday’s upside surprise in China’s official PMI data.

Across Europe, final S&P Global Manufacturing PMIs for Germany, the Eurozone, and the UK headline the morning session, alongside the Eurozone Unemployment Rate at 9:00 am GMT.

The US slate is what really stands out, with the ADP National Employment Report at 12:15 pm GMT offering an early read on private-sector hiring for March, followed by U.S. Retail Sales at 12:30 pm GMT for a pulse on consumer spending amid elevated energy prices. The ISM Manufacturing PMI at 2:00 pm GMT will be a key gauge of industrial activity, and the EIA Crude Oil Stocks report at 2:30 pm GMT may generate further oil-market volatility given the heightened sensitivity to supply dynamics.

Stay frosty out there, forex friends!

Promotion: Today’s Session Was an Opportunity to Practice Emotional Discipline. Were You Ready for It?

Tuesday’s session flipped the script in real time. Oil surged past $103 on escalation headlines — tanker strikes, missile interceptions, Strait of Hormuz fears — then reversed nearly 4% in hours on a single WSJ report. Equities ripped 3% higher. The dollar collapsed. Gold kept climbing through it all.

If you were positioned before those headlines broke, you faced the choice most traders fumble: hold, flip, or freeze?

In Positive Trading Psychology, renowned psychologist Brett Steenbarger argues that surviving sessions like today isn’t about eliminating emotional responses — it’s about channeling your character strengths to stay clinical when everyone else is reacting to the next headline. When a war-risk premium can reverse in a single news cycle, your psychology isn’t a soft edge. It’s your hardest one.

Learn more about “Positive Trading Psychology: Turning personal strengths into trading strengths” on Amazon!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.