Last week, Prime Minister Narendra Modi asked 1.4 billion Indians to do something that, on the surface, sounds almost reasonable: stop buying gold for a year.

Speaking at a BJP rally in Hyderabad, he said: “For a year, be it any function, we shouldn’t buy gold jewelry.”

Skip the wedding jewelry. Skip the festival coins. Give the country a break.

Within 72 hours, his government backed the appeal with a policy move that had (gold?) teeth… hiking the gold import duty from 6% to 15%.

The rupee, meanwhile, hit a record low of 96.97 against the dollar on May 20.

The request is rooted in a genuine economic emergency.

But if you understand India’s relationship with gold, you’d understand why many Indians are likely to keep buying anyway, and why they may not be wrong to do so.

India and Gold: More Than Just Jewelry

Gold is not just jewelry in India. It is savings, insurance, and inheritance all in one.

Families buy it for weddings, Diwali (the Hindu festival of lights), and Akshaya Tritiya (an auspicious Hindu day for buying gold).

Rural households use it as collateral for agricultural loans.

For generations without reliable access to banks or financial markets, a gold bangle was the most dependable store of wealth available.

Indian households have accumulated an estimated 25,000 to 28,000 tonnes of gold over centuries, more than the combined sovereign reserves of the United States, Germany, Italy, and France.

The metal is woven into the economy at every level, from street-corner jewelers to temple vaults to the Reserve Bank of India’s (RBI) own balance sheet.

Asking Indians to stop buying gold is not a simple lifestyle request. It cuts against one of the deepest financial instincts in the country.

Why Modi Is Asking

The appeal isn’t arbitrary. India is caught between two massive import bills it can’t easily control, and gold is the one the government thinks it can actually do something about.

Gold Is India’s Second-Biggest Import

India imports nearly all of the gold it consumes. Every gram purchased is effectively money leaving the country.

Gold imports hit a record $71.98 billion in FY26, up 24% year-on-year, making it the second-largest item on India’s import bill after oil.

The prolonged U.S.-Iran conflict has pushed oil prices sharply higher. Since India imports most of its energy, the bigger oil bill increases demand for dollars and puts downward pressure on the rupee.

The Rupee Is Under Serious Pressure

The combined pressure has widened India’s current account deficit to 1.3% of GDP in Q3 FY26.

Forex reserves have fallen by roughly $37.8 billion since the conflict began, from a record $728 billion in late February to around $690 billion by early May.

USD/INR is down roughly 7-8% year-to-date, making the rupee Asia’s worst-performing major currency.

The Reserve Bank of India (RBI) is reportedly selling around $1 billion per day to slow the slide, and still losing ground.

The RBI is reportedly selling around $1 billion per day to slow the rupee’s slide, and not everyone is familiar with how central bank currency intervention actually works. Premium members can read our lesson:

📖 Currency Intervention: When Central Banks Enter the Market

Reading this helps you understand how to spot intervention coming, what tools central banks use to defend a currency, and how to manage risk when a central bank is actively fighting the market.

And if you’re not a Premium subscriber yet, now’s a good time to sign up.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just what USD/INR is doing on the chart, but the central bank mechanics and intervention tactics driving the move.

The Cost of India’s Gold Habit

The GTRI think tank, which backed Modi’s appeal, put it plainly: “Rising bullion imports are hurting India’s foreign exchange reserves and trade balance.”

Union Minister Ashwini Vaishnaw reinforced the message at the CII Annual Business Summit, framing gold restraint as a matter of national economic security.

Even a 10% reduction in gold imports could save roughly $7.2 billion in forex, meaningful when every dollar counts.

👍 The Case for Listening to Modi

There are legitimate reasons to take Modi’s appeal seriously. Here’s the strongest case for it.

It’s a Bad Time to Buy

Gold prices are at record highs. At over Rs. 1,56,000 per 10 grams domestically, this is arguably the worst time to be a new buyer.

The duty hike makes it worse. You are now paying roughly 9 percentage points more in tax than you were three weeks ago.

Your Purchase Has a National Cost

The national impact is real. India is the world’s second-largest gold importer.

When Indians buy gold in large amounts, India has to spend dollars to import it. That can put pressure on the rupee and make imported essentials, from oil to food, more expensive for everyone.

So the problem is not just individual choice…what makes sense for one household can hurt the country when everyone does it all at once.

Paper Alternatives Are Available

Alternatives exist. Gold ETFs and gold mutual funds give you economic exposure to gold prices without triggering new physical imports.

They are cleaner, more liquid, and, since the July 2024 budget changes, taxed at the same 12.5% long-term capital gains rate as physical gold.

It’s Only for One Year

The government’s ask is for one year, not forever. A temporary pause during a genuine balance-of-payments stress event is a different kind of request than structural reform.

👎 The Case for Ignoring Him

History is not on the government’s side here. Indians have seen this movie before, and gold was the one that didn’t let them down.

The Rupee Has a Long Track Record of Losing

Every time the Indian government has asked its citizens to trust paper over gold, the people who ignored that advice came out ahead.

The rupee has lost roughly 81% of its value against the dollar since 1991.

Gold has roughly 6x’d in rupee terms over the past decade alone.

This chart above shows a gram of gold (XAU to INR) is currently trading at around ₹14,000.

Four years ago, it was below ₹4,000!

Demonetization Left a Scar

Demonetization in 2016 is the sharpest example, when Modi voided 86% of India’s currency overnight. Indians who rushed to convert cash into gold were vindicated.

The policy, by the RBI’s own later accounting, failed at its stated goal while successfully teaching a generation that government promises about money have limits.

That lesson has only been reinforced since.

The government has quietly shut down both of its own paper-gold alternatives.

Sovereign Gold Bonds, once pitched as the responsible modern substitute for physical gold, were discontinued in early 2024 after gold prices rose so dramatically that the redemption liability became a fiscal burden.

The Gold Monetization Scheme was partially wound down in 2025.

A government that voided its own currency, then quietly shut down its own gold alternatives, is now asking citizens to stop buying gold.

It’s not hard to understand why many will ignore the request.

Should Indians Stop Buying Gold?

Both sides of this debate have merit, and the right answer depends on whether you’re thinking like a policymaker or a household.

It Depends Who You’re Optimizing For

The honest answer is: it depends on whether you’re optimizing for India or for yourself, and history suggests those two things are genuinely in tension right now.

For the country, reduced gold imports would help narrow the deficit, ease pressure on the rupee, and free up foreign exchange for things that actually generate economic output.

The logic is sound.

For the individual Indian household, the case for gold hasn’t weakened.

A falling rupee, elevated inflation, discontinued paper alternatives, and a government track record of currency interventions all point toward the same conclusion Indians have been drawing for decades: gold holds its value when paper doesn’t.

Modi’s appeal is well-intentioned, and the underlying macro stress is real.

But asking Indian families to forgo gold is essentially asking them to trust the rupee more than they trust gold, a bet that the last 60 years of monetary history doesn’t support.

Which brings us to the rupee itself, and what all of this means if you’re trading it.

What This Means for Forex Traders

Whether or not Indians comply, the macro pressure driving this story is very much alive in the currency markets.

And if the rupee keeps falling, the people who kept buying gold will have been right again.

USD/INR: One-Way Traffic

According to analysts, USD/INR has become a one-way trend.

- DBS now forecasts 95-100 for the rest of 2026.

- Barclays raised its year-end target to 96.80.

- MUFG sees 97.50+ as possible.

- Ambit Capital goes further, projecting 100-101.5 by end-FY27.

The main variable is crude oil: every $10/bbl on Brent adds roughly $14-15 billion to India’s annual import bill.

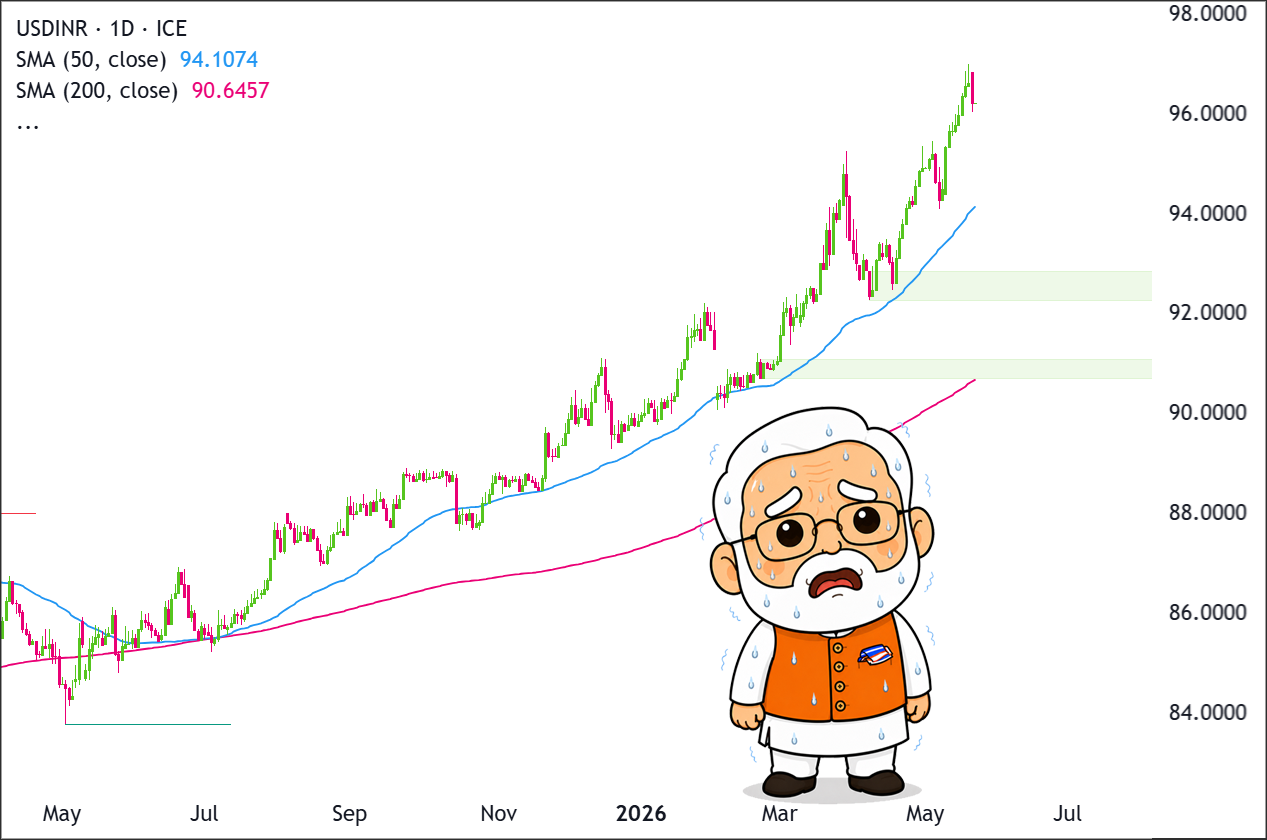

Current Price Action

USD/INR remains in a clear daily uptrend, with price holding above the rising 50-day SMA at 94.1074 and the 200-day SMA at 90.6457.

The broader structure is still bullish as long as price holds above the recent higher-low support area near 94.00–94.10.

- Immediate resistance is the recent high zone around 96.80–97.00, while the next visible upside extension area sits near 98.00.

- Deeper support is visible around 92.20–92.80, followed by the major support zone around 90.65–91.00.

Recent candles show strong upside momentum after buyers defended the pullback area near 94.00–94.10 and pushed the price into fresh highs near 96.80–97.00.

The latest candle shows some hesitation near the high, so buyers now need a daily close above 97.00 to confirm continuation.

Sellers would need to force price back below 94.00 to suggest the breakout leg is losing strength and that a deeper pullback toward 92.20–92.80 is opening.

The RBI Is Running Low on Ammunition

The RBI is fighting the slide but visibly losing ground.

It also announced a $5 billion swap auction for May 26, a tool that puts rupees into the system without permanently drawing down its foreign exchange reserves.

In other words, the central bank is trying to manage the slide while holding something back for later.

Standard Chartered now expects RBI rate hikes of 50 basis points starting in June, which could provide some temporary support.

Watch the June MPC Meeting

Watch the June 3-5 MPC meeting as the first major inflection point for the USD/INR direction.

A rate hike would make rupee assets more attractive to hold, slowing the currency’s slide.

A separate but complementary move would be a government bond scheme to attract dollar deposits from Indians living abroad.

It has done this before, raising $26 billion in 2013 by offering overseas Indians attractive rates to park dollars in Indian banks.

That kind of direct dollar inflow could give the rupee a meaningful boost.

A rate hold without new measures likely means another leg lower.