Last month, Mervyn King and the rest of his Bank of England (BOE) economists slapped the markets with another round of quantitative easing measures.

After waiting nearly two years to see if the economy would improve, the BOE announced that it would be implementing a 75 billion GBP asset purchase program. In addition, the central bank decided to keep rates steady at 0.50% in order to boost liquidity and lending.

The reasons for injecting more stimulus were simple: the slow pace of the global economy and the uncertainty surrounding the European debt crisis that had been choking the flow of credit in the markets.

The latest round of asset purchases will take about four months to complete, so chances are we will not be seeing any changes to the interest rate or additional QE measures until March next year at the earliest.

The BOE will most likely want to assess the effects of the additional asset purchases over this period before deciding upon any further moves.

So instead of waiting on changes in interest rates and the BOE’s quantitative easing program, let’s focus on the accompanying statement. Given the U.K.’s weak fundamentals, I think that it is highly likely that the BOE will maintain a very bearish economic outlook.

For instance, a weighted composite index for the U.K.’s purchasing managers’ indices for manufacturing, construction, and services fell to its lowest level in 28 months in October. It stood at 50.8, which is dangerously close to the 50.0 level, the dividing line between expansion and contraction.

Then, there’s the GDP report for the third quarter of this year. Preliminary estimates showed that the country probably grew 0.5% in the third quarter, beating the 0.4% forecast.

Sounds good, right? But here’s a little-known fact: the second-quarter GDP was revised down to 0.1% from 0.2%. This means that upside surprise was actually canceled out by the downward revision!The disappointing growth figures are being made worse by the stubbornly high inflation rate. The CPI for September was at 5.2%, 0.3% higher than forecast. According to the data, the sharp uptick in prices was the result of rising utility prices (e.g., electricity).

Normally, this isn’t a bad thing, but when GDP growth is slow, it could lead to a nasty case of stagflation (that’s stagnation and inflation in one)!

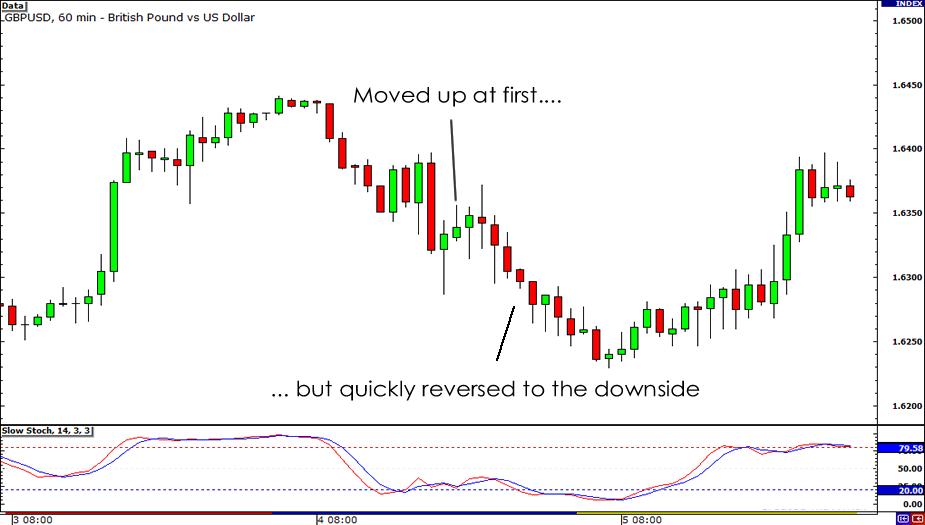

So, all these being said, how will Cable move following the announcement? To make educated guesses, let’s take a look at the most recent reactions of Cable when the central bank DID NOT do anything.

August 4, 2011

September 8, 2011

On both occasions, the release candle was green, meaning the price went up. However, after a few hours, the initial move was quickly faded and the price reversed to the downside.

To me, this indicates the U.K.’s disappointing fundamental background is weighing heavily on GBPUSD. For the upcoming release, any trade with a short bias seems to be a good idea. Be careful of the initial spike though!